Reading: Lesson 2 - The Value of an Asset

1. The Value of an Asset

- Our basic explanation of assets reveals that there are two ways in which you can earn money from holding an asset: (1) You may receive some kind of payment that we call a flow benefit—a dividend payment from a stock, a coupon payment from a bond, a rental check from an apartment, and so on. (2) The price of the asset may increase, in which case you get a capital gain. You might guess that the price of an asset should be linked in some way to the payments you get from the asset, and you would be right. In this section, we explain how to determine the price of an asset. To do so, we use two tools: discounted present value and expected value.

2. The Value of an Orange Tree

Imagine that you own a very simple asset: an orange tree. The orange tree pays a “dividend” in the form of fruit that you can sell. What is the value to you of owning such a tree? You can think of this value as representing the most you would be willing to pay for the orange tree—that is, your valuation of the tree. As we proceed, we will link this value to the price of the orange tree.

We begin by supposing your orange tree is very simple indeed. Next year, it will yield a crop of precisely one orange. That orange can be sold next year for $1. Then the tree will die. We suppose that you know all these things with certainty.

The value to you of the orange tree today depends on the value of having $1 next year. A dollar next year is not worth the same as a dollar this year. If you have a dollar this year, you can put it in the bank and earn interest on it. The technique of discounted present value tells us that you must divide next year’s dollar by the nominal interest factor to find its value today:

Here and for the rest of this chapter we use the nominal interest factor rather than the nominal interest rate to make the equations easier to read. The interest factor is 1 plus the interest rate, so whenever the interest rate is positive, the interest factor is greater than 1. We use the nominal interest factor because the flow benefit we are discounting has not been corrected for inflation. If this flow were already corrected for inflation, then we would instead discount by the real interest factor.

To see why this formula makes sense, begin with the special case of a nominal interest rate that is zero. Then using this formula, the discounted present value of a dollar next year is exactly $1. You would be willing to pay at most $1 today for the right to receive $1 next year. Similarly, if you put $1 in a bank paying zero interest today, you would have exactly $1 in the bank tomorrow. When the nominal interest rate is zero, $1 today and $1 next year are equally valuable. As another example, suppose the nominal interest rate is 10 percent. Using the formula, the discounted present value is = $0.909. If you put $0.909 in a bank account paying a 10 percent annual rate of interest (an interest factor of 1.1), then you would have $1 in the bank at the end of the year.

3. A Tree that Lives for Many Years

Our orange tree was a very special tree in many ways. Now we make our tree more closely resemble real assets in the economy. Suppose first that the tree lives for several years, yielding its flow benefit of fruit for many years to come. Finding the value of the tree now seems much harder, but there are some tricks that help us determine the answer. Orange trees—like stocks, bonds, and other assets—can be bought and sold. So suppose that next year, you harvest the crop of one orange, sell it, and then also sell the tree. Using this strategy, the value of the tree is as follows:

The first term is the same as before: it is the discounted present value to you of the crop next year ($1.00 in our example). The second term is the price that you can sell the tree for next year. After all, if the tree lives for 10 years, then next year it will still have 9 crops remaining and will still be a valuable asset.

This expression tells us something very important. The value of an asset depends on

- the value of the flow benefit (here, the crop of oranges) that you obtain while owning the asset,

- the price of the asset in the market when you sell it.

The insight that the value of the tree equals the value of the crop plus next year’s price greatly simplifies the analysis. If you know the price next year, then you know the value of the tree to you this year. Of course, we do not yet know how the price next year is determined; we come back to that question later.

We can now give a more precise definition of the return on an asset: it is the amount you obtain, in percentage terms, from holding the asset for a year. The return has two components: a flow of money (such as a dividend in the case of a stock) and the price of the asset.

In this simple case, the return on the asset is equal to the nominal interest rate. If we wanted the real return, we would use the real interest factor (1 + the real interest rate) instead.

4. A Tree with a Random Crop

- So far we have assumed that you know the orange crop with certainty. This is a good starting point but is not realistic if we want to use our story to understand the value of actual assets. We do not know for sure the future dividends that will be paid by a company whose stock we might own. Nor do we know the future price of a stock or a bond.

Looking back at the tree that lives for one year only, imagine you do not know how many oranges it will yield. Start by assuming that you can buy a tree that lasts for one period and whose crop is not known with certainty. The value of the tree depends on the following.

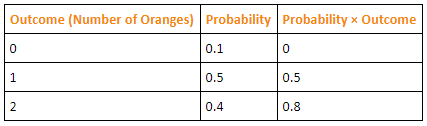

- The expected value of the crop. You must list all the possible outcomes and the probability of each outcome. For example, the Table below "Expected Crop from an Orange Tree" shows the case of a tree where there are three possible outcomes: 0, 1, or 2 oranges. The probability of 0 oranges is 10 percent—that is, 1 in 10 times on average, the tree yields no fruit. The probability of 1 orange is 50 percent: half the time, on average, the tree yields 1 fruit. And the probability of 2 oranges is 40 percent. The expected crop is obtained by adding together the numbers in the final column: 1.3 oranges.

- A risk premium is an addition to the return on an asset that is demanded by investors to compensate for the riskiness of the asset. This adjustment reflects the riskiness of the crop and how risk-averse the owner of the tree is. If the owner is risk-neutral, there is no need for a risk premium. Obviously enough, if the crop is known with certainty, there is also no need for a risk premium.

The easiest way to see how the risk premium works is to recognize that someone who is risk-averse will demand a higher return to hold a risky asset. Earlier, we said that the return on an asset without risk equals the nominal interest rate. From this we can see that there is a relationship between risk and return. If the crop is not risky, then the risk premium is zero, so the return equals the nominal interest rate. As the crop becomes riskier, the risk premium increases, causing an increase in the return per dollar invested.

We can see how the risk premium affects the value of the tree by rearranging the equation:

For a given expected crop, the higher is the risk premium, the lower is the value of the tree.

5. The Value of a Bond

- Suppose that you want to value a bond that lasts only one year. You will receive a payment from the borrower next year and then—because the bond has reached its maturity date—there will be no further payments. Naturally enough, the bond is worthless once it matures, so its price next year will be zero. This bond is like the first orange tree we considered: it delivers a crop next year and then dies. For example, if the coupon on the bond called for a payment of $100 next year and the nominal interest rate was zero, then the value of the bond today would be $100. But if the nominal interest rate was 10 percent, then the value of the bond today would be = $90.91.

If the bond has several years until maturity,

This expression for the value of a bond is very powerful. It shows that a bond is more valuable this year if

- the coupon payment next year is higher,

- the bond will sell for a higher price next year, or

- interest rates are lower

We explained earlier that bonds are subject to inflation risk. There are two ways of seeing this in our example. Imagine that inflation increases by 10 percentage points.

This inflation means that the coupon payment next year will be worth less in real terms—that is, in terms of the amount of goods and services that it will buy. Also, from the Fisher equation, we know that increases in the inflation rate translate into changes in the nominal interest rate. If inflation increases by 10 percentage points and the real rate of interest is unchanged, then the nominal rate increases by 10 percentage points. So the discounted present value of the bond decreases. Inflation risk might cause a bondholder to include a risk premium when valuing the bond.

6. The Value of a Stock

- Now let us use our general equation to evaluate the dividend flow from stock ownership. Imagine you are holding a share of a stock this year. You can hold it for a year, receive the dividend payment if there is one, and then sell the stock. For now we treat both the dividend and the price next year as if they are known for sure. What is the value of a share under that plan? The flow benefit in this case is the dividend paid on the stock. Because the dividend is received next year, we have to discount it back to the current year using the nominal interest factor. The other part of the value of the share comes from the fact that it can be sold next year. Again, that share price must be discounted to put it in today’s terms. If the share does not pay a dividend next year, then its value is even simpler: the value of the share this year equals its price next year discounted by the nominal interest factor.

The return to owning the share comes in two forms: the dividend and the gain from selling the share next year. To calculate the return per dollar invested, we divide the dividend and future price by the value of a share this year:

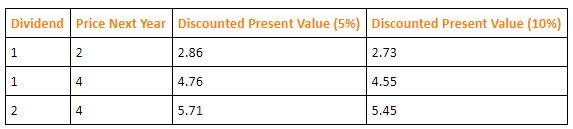

The Table below "Discounted Present Value of Dividends in Dollars" shows an example where we calculate the value of a stock using two different interest rates: 5 percent and 10 percent.

最后修改: 2018年08月14日 星期二 10:13