Reading: Lesson 2 - The accounting cycle summarized

In Unit 2, you learned that when an event is a measurable business transaction, you need

adequate proof of this transaction. Then, you analyze the transaction's effects on the accounting

equation, Assets = Liabilities + Stockholders' equity. In Chapters 2 and 3, you performed other steps in

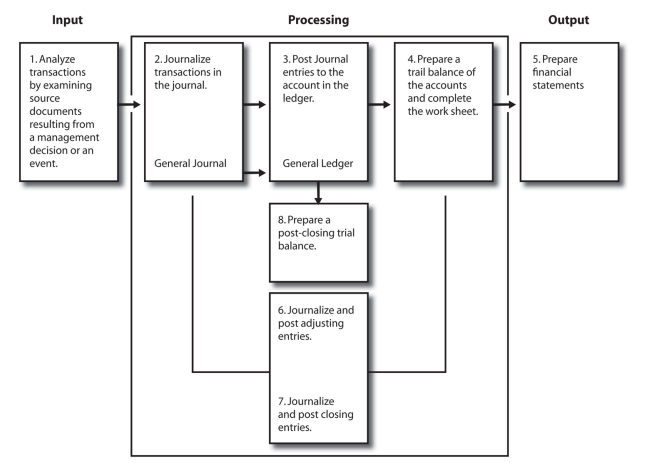

the accounting cycle. Unit 3 presented the eight steps in the accounting cycle as a preview of the

content of Chapters 2 through 4. As a review, study the diagram of the eight steps in the accounting

cycle in Exhibit 19. Remember that the first three steps occur during the accounting period and the last

five occur at the end. The next section explains how to use the work sheet to facilitate the completion of

the accounting cycle.

The work sheet

The work sheet is a columnar sheet of paper or a computer spreadsheet on which accountants

summarize information needed to make the adjusting and closing entries and to prepare the financial

statements. Usually, they save these work sheets to document the end-of-period entries. A work sheet

is only an accounting tool and not part of the formal accounting records. Therefore, work sheets may

vary in format; some are prepared in pencil so that errors can be corrected easily. Other work sheets

are prepared on personal computers with spreadsheet software. Accountants prepare work sheets each

time financial statements are needed—monthly, quarterly, or at the end of the accounting year.

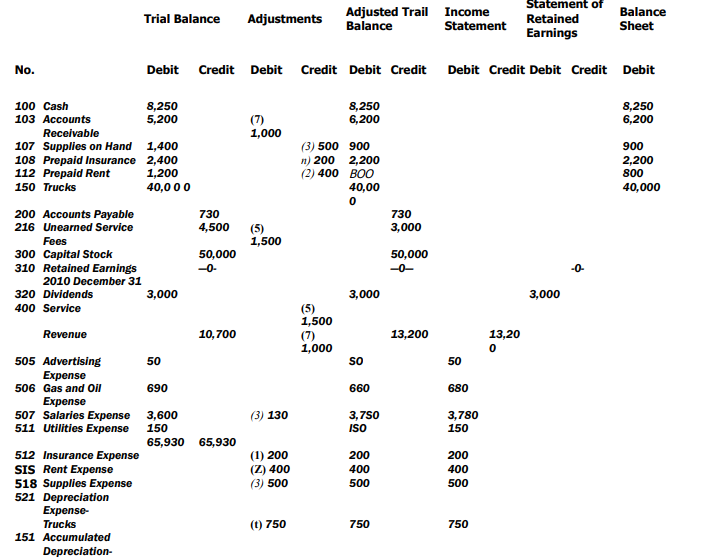

This unit illustrates a 12-column work sheet that includes sets of columns for an unadjusted trial

balance, adjustments, adjusted trial balance, income statement, statement of retained earnings, and

balance sheet. Each set has a debit and a credit column. (See Exhibit 20.)

Accountants use these initial steps in preparing the work sheet. The following sections describe the

detailed steps for completing the work sheet.

- Enter the titles and balances of ledger accounts in the Trial Balance columns.

- Enter adjustments in the Adjustments columns. Enter adjusted account balances in the Adjusted Trial Balance columns.

- Extend adjusted balances of revenue and expense accounts from the Adjusted Trial Balance columns to the Income Statement columns.

- Extend any balances in the Retained Earnings and Dividends accounts to the Statement of Retained Earnings columns.

- Extend adjusted balances of asset, liability, and capital stock accounts from the Adjusted

Trial Balance columns to the Balance Sheet columns.

Instead of preparing a separate trial balance as we did in Chapter 2, accountants use the Trial

Balance columns on a work sheet. Look at Exhibit 20 and note that the numbers and titles of the ledger

accounts of MicroTrain Company are on the left portion of the work sheet. Usually, only those accounts

with balances as of the end of the accounting period are listed. (Some accountants do list the entire

chart of accounts, even those with zero balances.) Assume you are MicroTrain's accountant. You list

the Retained Earnings account in the trial balance even though it has a zero balance to (1) show its

relative position among the accounts and (2) indicate that December 2010 is the first month of

operations for this company. Next, you enter the balances of the ledger accounts in the Trial Balance

columns. The accounts are in the order in which they appear in the general ledger: assets, liabilities,

stockholders' equity, dividends, revenues, and expenses. Then, total the columns. If the debit and

credit column totals are not equal, an error exists that must be corrected before you proceed with the

work sheet.

As you learned in Unit 4, adjustments bring the accounts to their proper balances before

accountants prepare the income statement, statement of retained earnings, and balance sheet. You

enter these adjustments in the Adjustments columns of the work sheet. Also, you cross-reference the

debits and credits of the entries by placing a key number or letter to the left of the amounts. This key

number facilitates the actual journalizing of the adjusting entries later because you do not have to

rethink the adjustments to record them. For example, the number (1) identifies the adjustment

debiting Insurance Expense and crediting Prepaid Insurance. Note in the Account Titles column that the Insurance Expense account title is below the trial balance totals because the Insurance Expense

account did not have a balance before the adjustment and, therefore, did not appear in the trial

balance.

Work sheet preparers often provide brief explanations at the bottom for the keyed entries as in

Exhibit 20. Although these explanations are optional, they provide valuable information for those who

review the work sheet later.

The adjustments (which were discussed and illustrated in Unit 4) for MicroTrain Company are:

Exhibit 19: Steps in the accounting cycle

- Entry (1) records the expiration of USD 200 of prepaid insurance in December.

- Entry (2) records the expiration of USD 400 of prepaid rent in December.

- Entry (3) records the using up of USD 500 of supplies during the month.

- Entry (4) records USD 750 depreciation expense on the trucks for the month. MicroTrain

acquired the trucks at the beginning of December.

MicroTrain acquired the trucks at the beginning of December

- Entry (5) records the earning of USD 1,500 of the USD 4,500 in the Unearned Service Fees account.

- Entry (6) records USD 600 of interest earned in December.

- Entry (7) records USD 1,000 of unbilled training services performed in December.

- Entry (8) records the USD 180 accrual of salaries expense at the end of the month.

Often it is difficult to discover all the adjusting entries that should be made. The following steps are

helpful:

- Examine adjusting entries made at the end of the preceding accounting period. The same types of entries often are necessary period after period.

- Examine the account titles in the trial balance. For example, if the company has an account titled Trucks, an entry must be made for depreciation.

- Examine various business documents (such as bills for services received or rendered) to discover other assets, liabilities, revenues, and expenses that have not yet been recorded.

- Ask the manager or other personnel specific questions regarding adjustments that may be

necessary. For example: "Were any services performed during the month that have not yet been

billed?"

(1) To record insurance expenses for December.

(2) To record rent expenses for December.

(3) To record supplies expenses for December.

(4) To record depreciation expenses for December.

(5) To transfer fees for service provided in December from the liability account to the revenue account.

(6) To record one month's interest revenue.

(7) To record unbilled training services performed in December.

(8) To accrue one day's salaries that were earned but are unpaid.

After all the adjusting entries are entered in the Adjustments columns, total the two columns. The

totals of these two columns should be equal when all debits and credits are entered properly.

After MicroTrain's adjustments, compute the adjusted balance of each account and enter these in

the Adjusted Trial Balance columns. For example, Supplies on Hand (Account No. 107) had an

unadjusted balance of USD 1,400. Adjusting entry (3) credited the account for USD 500, leaving a

debit balance of USD 900. This amount is a debit in the Adjusted Trial Balance columns.

Next, extend all accounts having balances to the Adjusted Trial Balance columns. Note carefully

how the rules of debit and credit apply in determining whether an adjustment increases or decreases

the account balance. For example, Salaries Expense (Account No. 507) has a USD 3,600 debit balance

in the Trial Balance columns. A USD 180 debit adjustment increases this account, which has a USD

3,780 debit balance in the Adjusted Trial Balance columns.

Some account balances remain the same because no adjustments have affected them. For example,

the balance in Accounts Payable (Account No. 200) does not change and is simply extended to the

Adjusted Trial Balance columns.

Now, total the Adjusted Trial Balance debit and credit columns. The totals must be equal before

taking the next step in completing the work sheet. When the Trial Balance and Adjustments columns

both balance but the Adjusted Trial Balance columns do not, the most probable cause is a math error or

an error in extension. The Adjusted Trial Balance columns make the next step of sorting the amounts

to the Income Statement, the Statement of Retained Earnings, and the Balance Sheet columns much

easier.

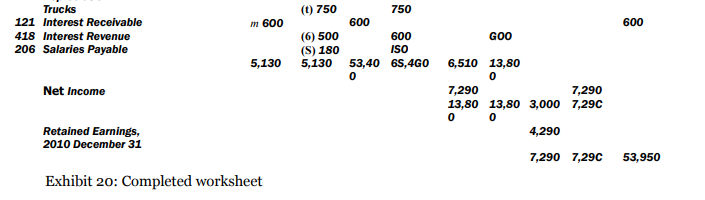

Begin by extending all of MicroTrain's revenue and expense account balances in the Adjusted Trial

Balance columns to the Income Statement columns. Since revenues carry credit balances, extend them

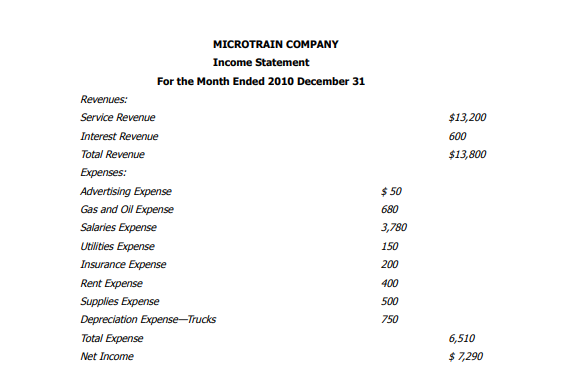

to the credit column. After extending expenses to the debit column, subtotal each column. MicroTrain's

total expenses are USD 6,510 and total revenues are USD 13,800. Thus, net income for the period is USD 7,290 (USD 13,800—USD 6,510). Enter this USD 7,290 income in the debit column to make the

two column totals balance. You would record a net loss in the opposite manner; expenses (debits)

would have been larger than revenues (credits) so a net loss would be entered in the credit column to

make the columns balance.

Next, complete the Statement of Retained Earnings columns. Enter the USD 7,290 net income

amount for December in the credit Statement of Retained Earnings column. Thus, this net income

amount is the balancing figure for the Income Statement columns and is also in the credit Statement of

Retained Earnings column. Net income appears in the Statement of Retained Earnings credit column

because it causes an increase in retained earnings. Add the USD 7,290 net income to the beginning

retained earnings balance of USD 0, and deduct the dividends of USD 3,000. As a result, the ending

balance of the Retained Earnings account is USD 4,290.

Now extend the assets, liabilities, and capital stock accounts in the Adjusted Trial Balance columns

to the Balance Sheet columns. Extend asset amounts as debits and liability and capital stock amounts

as credits.

Note that the ending retained earnings amount determined in the Statement of Retained Earnings

columns appears again as a credit in the Balance Sheet columns. The ending retained earnings amount

is a debit in the Statement of Retained Earnings columns to balance the Statement of Retained

Earnings columns. The ending retained earnings is a credit in the Balance Sheet columns because it

increases stockholders' equity, and increases in stockholders' equity are credits. (Retained earnings

would have a debit ending balance only if cumulative losses and dividends exceed cumulative

earnings.) With the inclusion of the ending retained earnings amount, the Balance Sheet columns

balance.

When the Balance Sheet column totals do not agree on the first attempt, work backward through

the process used in preparing the work sheet. Specifically, take the following steps until you discover

the error:

Exhibit 21: Income statement

- Re-total the two Balance Sheet columns to see if you made an error in addition. If the column

totals do not agree, check to see if you did not extend a balance sheet item or if you made an

incorrect extension from the Adjusted Trial Balance columns.

- Re-total the Statement of Retained Earnings columns and determine whether you entered the correct amount of retained earnings in the appropriate Statement of Retained Earnings and Balance Sheet columns.

- Re-total the Income Statement columns and determine whether you entered the correct amount of net income or net loss for the period in the appropriate Income Statement and Statement of Retained Earnings columns.

Modifié le: mardi 28 mai 2019, 12:10