Reading: Lesson 2 - Determining inventory cost I

To place the proper valuation on inventory, a business must answer the question: Which costs

should be included in inventory cost? Then, when the business purchases identical goods at different costs, it must answer the question: Which cost should be assigned to the items sold? In this section,

you learn how accountants answer these questions.

The costs included in inventory depend on two variables: quantity and price. To arrive at a current

inventory figure, companies must begin with an accurate physical count of inventory items. They

multiply the quantity of inventory by the unit cost to compute the cost of ending inventory. This section

discusses the taking of a physical inventory and the methods of costing the physical inventory under

both perpetual and periodic inventory procedures. The remainder of the chapter discusses departures

from the cost basis of inventory measurement.

To take a physical inventory, a company must count, weigh,

measure, or estimate the physical quantities of the goods on hand. For example, a clothing store may

count its suits; a hardware store may weigh bolts, washers, and nails; a gasoline company may measure

gasoline in storage tanks; and a lumberyard may estimate quantities of lumber, coal, or other bulky

materials. Throughout the taking of a physical inventory, the goal should be accuracy.

Taking a physical inventory may disrupt the normal operations of a business. Thus, the count

should be administered as quickly and as efficiently as possible. The actual taking of the inventory is

not an accounting function; however, accountants often plan and coordinate the count. Proper forms

are required to record accurate counts and determine totals. Identification names or symbols must be

chosen, and those persons who count, weigh, or measure the inventory items must know these

symbols.

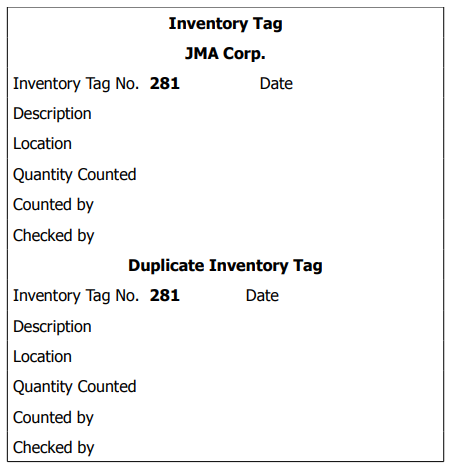

Exhibit 47: Inventory tag

Taking a physical inventory often involves using inventory tags, such as that in Exhibit 47. These

tags are consecutively numbered for control purposes. A tag usually consists of a stub and a detachable

duplicate section. The duplicate section facilitates checking discrepancies. The format of the tags can

vary. However, the tag usually provides space for (1) a detailed description and identification of

inventory items by product, class, and model; (2) location of items; (3) quantity of items on hand; and

(4) initials of the counters and checkers.

The descriptive information and count may be entered on one copy of the tag by one team of

counters. Another team of counters may record its count on the duplicate copy of the tag.

Discrepancies between counts of the same items by different teams are reconciled by supervisors, and

the correct counts are assembled on intermediate inventory sheets. Only when the inventory counts are

completed and checked does management send the final sheets to the accounting department for

pricing and extensions (quantity X price). The tabulated result is the dollar amount of the physical

inventory. Later in the chapter we explain the different methods accountants use to cost inventory.

Usually, inventory cost includes all the necessary outlays to obtain the goods, get the goods ready to

sell, and have the goods in the desired location for sale to customers. Thus, inventory cost includes:

- Seller's invoice price less any purchase discount.

- Cost of the buyer's insurance to cover the goods while in transit.

- Transportation charges when borne by the buyer.

- Handling costs, such as the cost of pressing clothes wrinkled during shipment.

In theory, the cost of each unit of inventory should include its net invoice price plus its share of

other costs incurred in shipment. The 1986 Tax Reform Act requires companies to assign these costs to

inventory for tax purposes. For accounting purposes, these cost assignments are recommended but not

required.

Practical difficulties arise in allocating some of these costs to inventory items. Assume, for example,

that the freight bill on a shipment of clothes does not separate out the cost of shipping one shirt. Also,

assume that the company wants to include the freight cost as part of the inventory cost of the shirt.

Then, the freight cost would have to be allocated to each unit because it cannot be measured directly.

In practice, allocations of freight, insurance, and handling costs to the individual units of inventory

purchased are often not worth the additional cost. Consequently, in the past many companies have not

assigned the costs of freight, insurance, and handling to inventory. Instead, they have expensed these

costs as incurred. When companies omit these costs from both beginning and ending inventories, they minimize the effect of expensing these costs on net income. The required allocation for tax purposes

has probably resulted in many companies using the same inventory amounts in their financial

statements.

Even if a company derives a cost for each unit in inventory, the inventory valuation problem is not

solved. Management must consider two other aspects of the problem:

- If goods were purchased at varying unit costs, how should the cost of goods available for sale be allocated between the units sold and those that remain in inventory? For example, assume Hi-Fi Buys, Inc., purchased two identical DVD players for resale. One cost USD 250 and the other, USD 200. If one was sold during the period, should Hi-Fi Buys assign it a cost of USD 250, USD 200, or an average cost of USD 225?

- Does the fact that current replacement costs are less than the costs of some units in inventory

have any bearing on the amount at which inventory should be carried? Using the same

example, if Hi-Fi Buys can currently buy all DVD players for USD 200, is it reasonable to carry

some units in inventory at USD 250 rather than USD 200?

We answer these questions in the next section.

Generally companies should account for inventories at historical cost; that is, the cost at which the

items were purchased. However, this rule does not indicate how to assign costs to ending inventory and

to cost of goods sold when the goods have been purchased at different unit costs. For example, suppose

a retailer has three shirts on hand. One costs USD 20; another, USD 22; and a third, USD 24. If the

retailer sells two shirts for USD 30 each, what is the cost of the two shirts sold?

Accountants developed these four inventory costing methods to solve costing problems: (1) specific

identification; (2) first-in, first-out (FIFO); (3) last-in, first-out (LIFO); and (4) weighted-average.

Before explaining the inventory costing methods, we briefly introduce perpetual inventory procedure

and compare periodic and perpetual inventory procedures.

Under periodic inventory

procedure, firms debit the Purchases account when goods are acquired; they use other accounts, such

as Purchase Discounts, Purchase Returns and Allowances, and Transportation-In, for purchase-related

transactions. Companies determine cost of goods sold only at the end of the period as the difference

between cost of goods available for sale and ending inventory. They keep no records of the cost of items

as they are sold, and have no information on possible inventory shortages. They assume any goods not

in ending inventory have been sold.

The availability of inventory management software packages is causing more and more businesses

to change from periodic to perpetual inventory procedure. Under perpetual inventory procedure,

companies have no Purchases and purchase-related accounts. Instead, they make all entries involving

merchandise purchased for sale to customers directly in the Merchandise Inventory account. Thus,

they debit or credit Merchandise Inventory in place of debiting or crediting Purchases, Purchase

Discounts, Purchase Returns and Allowances, and Transportation-In. At the time of each sale, firms

make two entries: the first debits Accounts Receivable or Cash and credits Sales at the retail selling

price. The second debits Cost of Goods Sold and credits Merchandise Inventory at cost. Therefore, at

the end of the period the Merchandise Inventory account shows the cost of the inventory that should be

on hand. Comparison of this amount with the cost obtained by taking and pricing a physical inventory

may reveal inventory shortages. Thus, perpetual inventory procedure is an important element in

providing internal control over goods in inventory.

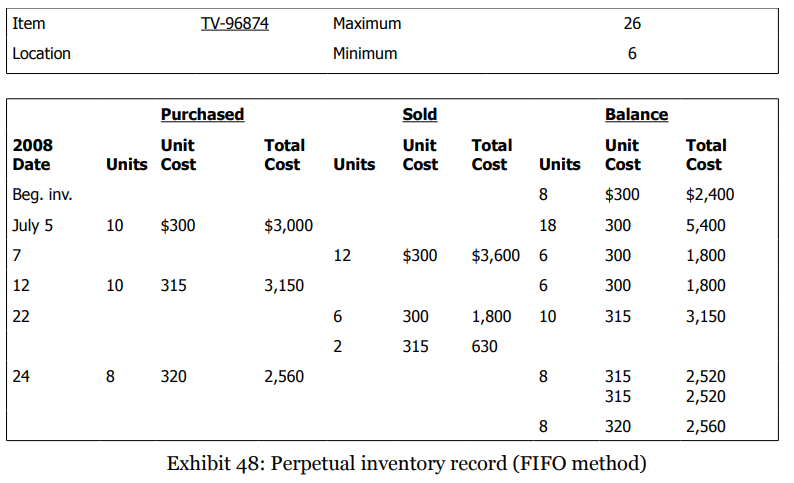

Perpetual inventory records Even though companies could apply perpetual inventory

procedure manually, tracking units and dollars in and out of inventory is much easier using a

computer. Both manual and computer processing maintain a record for each item in inventory. Look at

Exhibit 48, an inventory record for Entertainment World, a firm that sells many different brands of

television sets. This inventory record shows the information on one particular brand and model of

television set carried in inventory. Other information on the record includes (1) the maximum and minimum number of units the company wishes to stock at any time, (2) when and how many units

were acquired and at what cost, and (3) when and how many units were sold and what cost was

assigned to cost of goods sold. The number of units on hand and their cost are readily available also.

Entertainment World assumes that the first units acquired are the first units sold. This assumption is

the first-in, first-out (FIFO) method of inventory costing; we will discuss it later.

The following comparison reveals several differences between accounting for inventories under

periodic and perpetual procedures. We explain these differences by using data from Exhibit 48 and

making additional assumptions. Later, we discuss other journal entries under perpetual inventory

procedure.

Assuming the merchandise sold on July 7 was priced at USD 4,800, these entries record the sale:

Several other transactions not included in Exhibit 48 could occur:

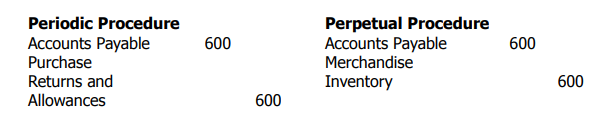

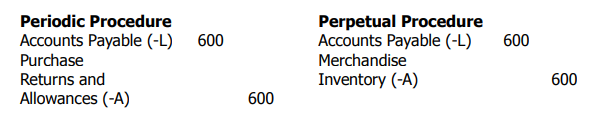

- Assume that two of the units purchased on July 5 were returned to the supplier because they were defective. The entries would be:

- Assume that the supplier instead granted an allowance of USD 600 to the company because

of the defective merchandise. The entries would be:

- Assume that the company incurred and paid freight charges of USD 100 on the purchase of

July 5. The entries would be:

In these entries, notice that under perpetual inventory procedure the Merchandise Inventory

account records purchases, purchase returns and allowances, purchase discounts, and transportationin.

Also, when goods are sold, the seller debits (increases) Cost of Goods Sold and credits or reduces

Merchandise Inventory.

At the end of the accounting period, under perpetual inventory procedure, the only merchandis erelated

expense account to be closed is Cost of Goods Sold. The Purchases, Purchase Returns and

Allowances, Purchase Discounts, and Transportation-In accounts do not even exist.

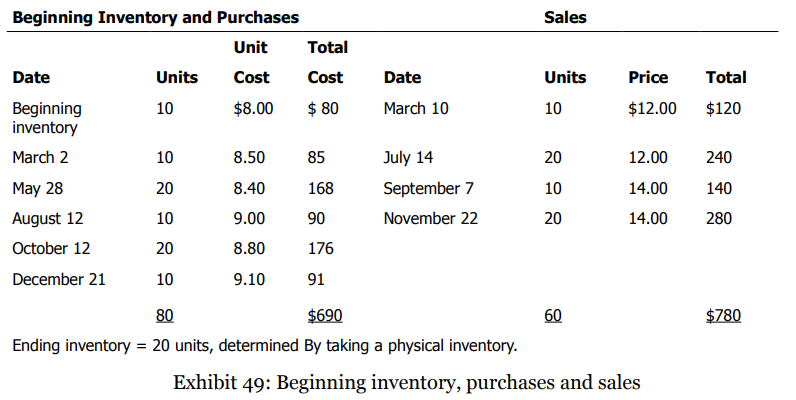

Using the data for purchases, sales, and beginning inventory in Exhibit 49, next we explain the four

inventory costing methods. Except for the specific identification method, we first present all of the

methods using periodic inventory procedure and then present all of the methods using perpetual

inventory procedure. Total goods available for sale consist of 80 units with a total cost of USD 690. A

physical inventory determined that 20 units are on hand at the end of the period. Sales revenue for the 60 units sold was USD 780. The questions to be answered are: What is the cost of the 20 units in

inventory? What is the cost of the 60 units sold?

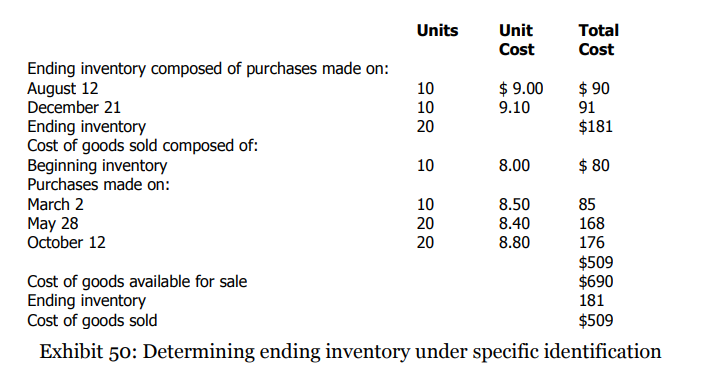

Specific identification The specific identification method of inventory costing attaches the

actual cost to an identifiable unit of product. Firms find this method easy to apply when purchasing

and selling large inventory items such as autos. Under the specific identification method, the firm must

identify each unit in inventory, unless it is unique, with a serial number or identification tag.

To illustrate, assume that the company in Exhibit 49 can identify the 20 units on hand at year-end

as 10 units from the August 12 purchase and 10 units from the December 21 purchase. The company

computes the ending inventory as shown in Exhibit 50; it subtracts the USD 181 ending inventory cost

from the USD 690 cost of goods available for sale to obtain the USD 509 cost of goods sold. Note that

you can also determine the cost of goods sold for the year by recording the cost of each unit sold. The

USD 509 cost of goods sold is an expense on the income statement, and the USD 181 ending inventory

is a current asset on the balance sheet.

The specific identification costing method attaches cost to an identifiable unit of inventory. The

method does not involve any assumptions about the flow of the costs as in the other inventory costing

methods. Conceptually, the method matches the cost to the physical flow of the inventory and

eliminates the emphasis on the timing of the cost determination. Therefore, periodic and perpetual

inventory procedures produce the same results for the specific identification method.

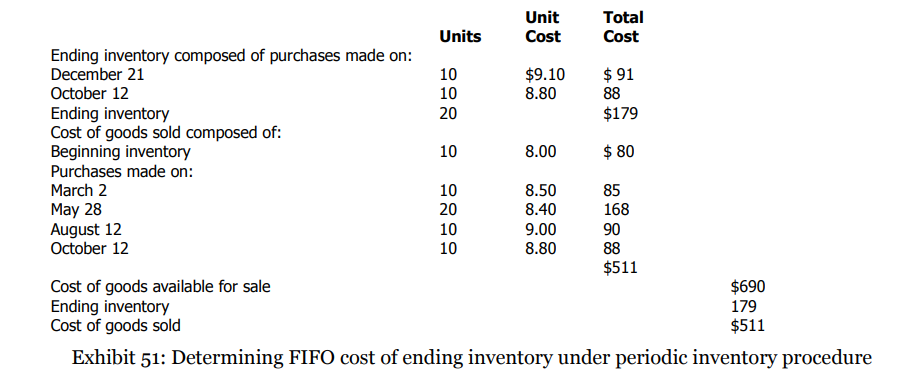

FIFO (first-in, first-out) under periodic inventory procedure The FIFO (first-in, firstout)

method of inventory costing assumes that the costs of the first goods purchased are those charged to cost of goods sold when the company actually sells goods. This method assumes the first goods

purchased are the first goods sold. In some companies, the first units in (bought) must be the first units

out (sold) to avoid large losses from spoilage. Such items as fresh dairy products, fruits, and vegetables

should be sold on a FIFO basis. In these cases, an assumed first-in, first-out flow corresponds with the

actual physical flow of goods.

Because a company using FIFO assumes the older units are sold first and the newer units are still

on hand, the ending inventory consists of the most recent purchases. When using periodic inventory

procedure, to determine the cost of the ending inventory at the end of the period under FIFO, you

would begin by listing the cost of the most recent purchase. If the ending inventory contains more units

than acquired in the most recent purchase, it also includes units from the next-to-the-latest purchase

at the unit cost incurred, and so on. You would list these units from the latest purchases until that

number agrees with the units in the ending inventory.

In Exhibit 51, you can see how to determine the cost of ending inventory under FIFO using periodic

inventory procedure. The company assumes that the 20 units in inventory consist of 10 units

purchased December 21 and 10 units purchased October 12. The total cost of ending inventory is USD

179, and the cost of goods sold is USD 511.

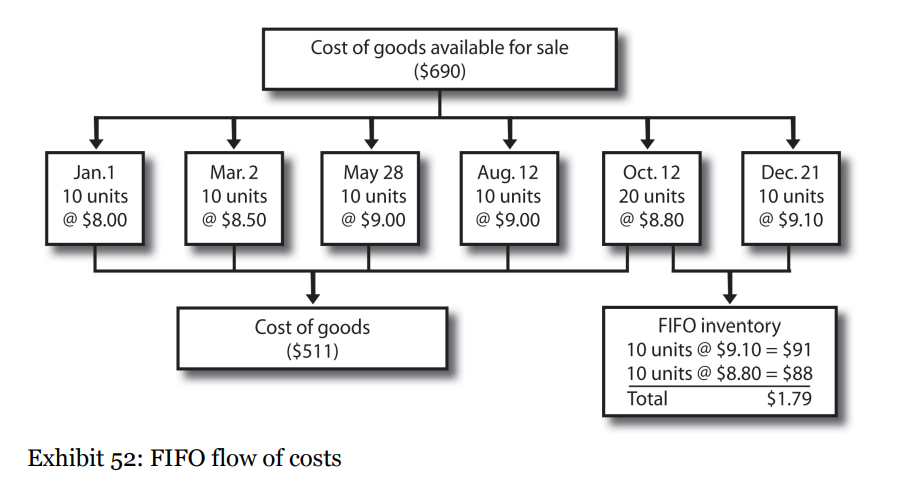

We show the relationship between the cost of goods sold and the cost of ending inventory under

FIFO using periodic inventory procedure in Exhibit 52. The 80 units in cost of goods available for sale

consists of the beginning inventory and all of the purchases during the period. Under FIFO, the ending

inventory of 20 units consists of the most recent purchases—10 units of the December 21 purchase and

10 units of the October 12 purchase—costing USD 179. We assume the beginning inventory and other

earlier purchases have been sold during the period, representing the cost of goods sold of USD 511.

LIFO (last-in, first-out) under periodic inventory procedure The LIFO (last-in, firstout)

method of inventory costing assumes that the costs of the most recent purchases are the first

costs charged to cost of goods sold when the company actually sells the goods.

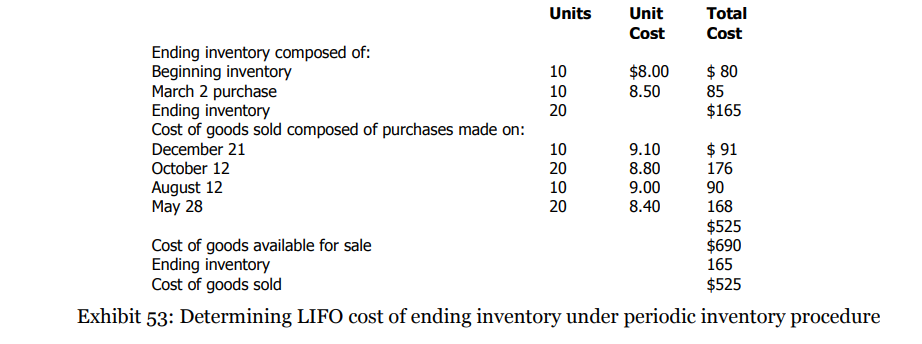

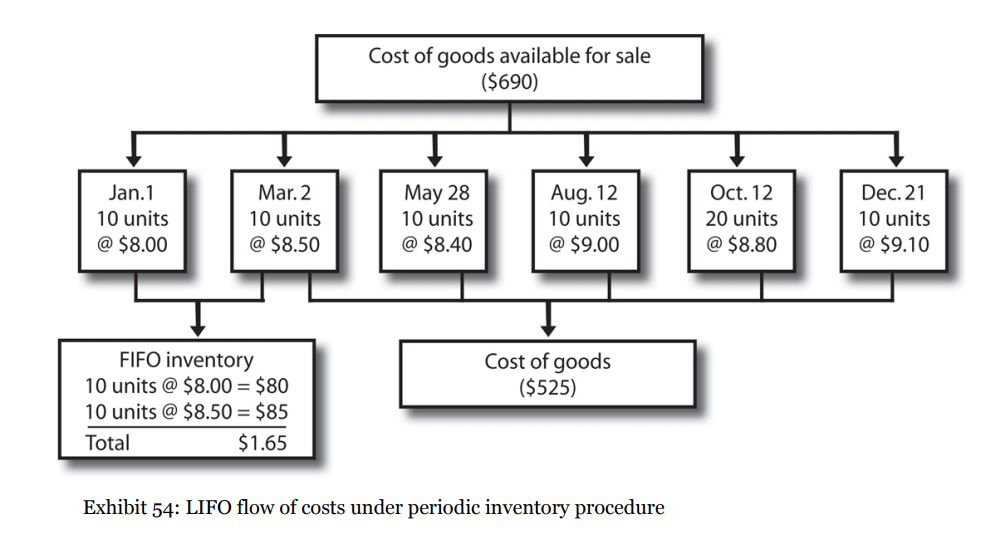

In Exhibit 53, we show the use of LIFO under periodic inventory procedure. Since the company

charges the latest costs to cost of goods sold under periodic inventory procedure, the ending inventory

always consists of the oldest costs. Therefore, when determining the cost of inventory under periodic inventory procedure, the company lists the oldest units and their costs. The first units listed are those

in beginning inventory, then the first purchase, and so on, until the number listed agrees with the units

in ending inventory. Thus, ending inventory in Exhibit 53 consists of the 10 units from beginning

inventory and the 10 units purchased on March 2. The total cost of these 20 units, USD 165, is the

ending inventory cost; the cost of goods sold is USD 525. Exhibit 54 is a graphic representation of the

LIFO flow of costs under periodic inventory procedure.

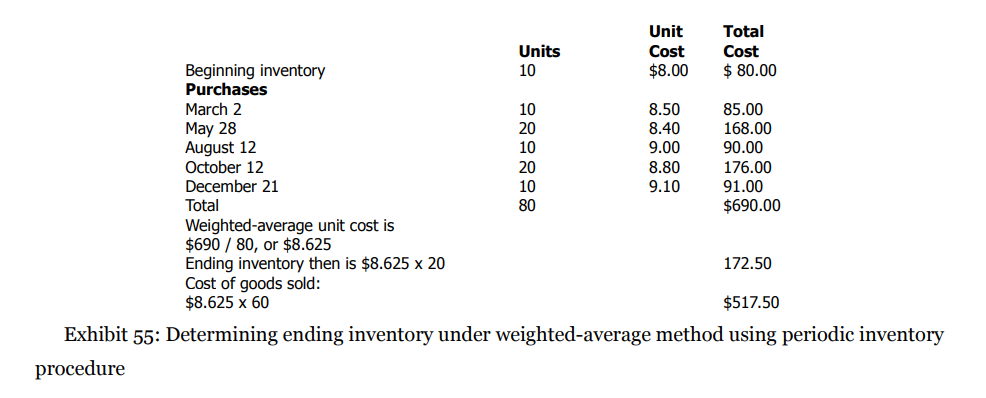

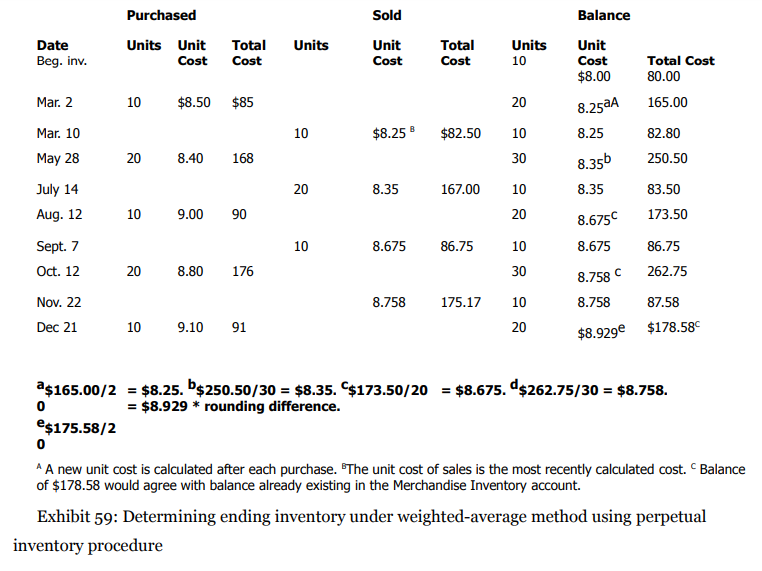

Weighted-average under periodic inventory procedure The weighted-average method

of inventory costing is a means of costing ending inventory using a weighted-average unit cost.

Companies most often use the weighted-average method to determine a cost for units that are basically

the same, such as identical games in a toy store or identical electrical tools in a hardware store. Since

the units are alike, firms can assign the same unit cost to them.

Under periodic inventory procedure, a company determines the average cost at the end of the

accounting period by dividing the total units purchased plus those in beginning inventory into total

cost of goods available for sale. The ending inventory is carried at this per unit cost. To see how a

company uses the weighted-average method to determine inventory costs using periodic inventory

procedure, look at Exhibit 55. Note that we compute weighted-average cost per unit by dividing the

cost of units available for sale, USD 690, by the total number of units available for sale, 80. Thus, the

weighted-average cost per unit is USD 8.625, meaning that each unit sold or remaining in inventory is

valued at USD 8.625.

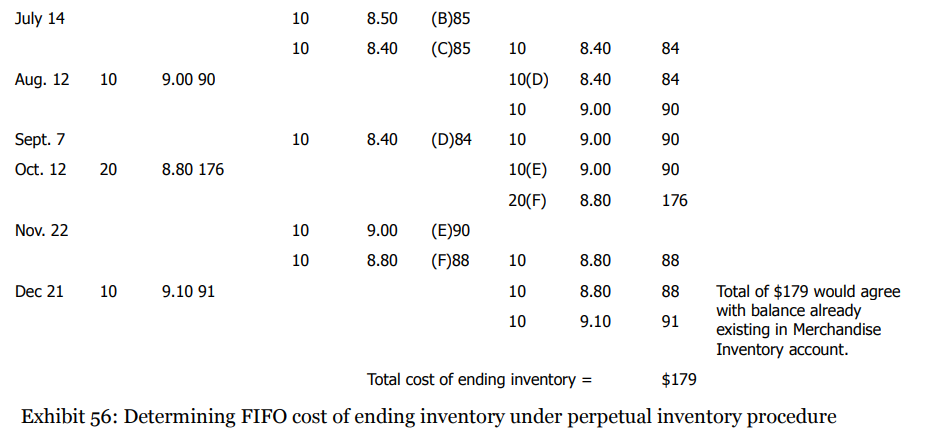

FIFO under perpetual inventory procedure Under perpetual inventory procedure, the ending

balance in the Merchandise Inventory account reflects the most recent purchases as a result of making

the required entries during the period. Also, the firm has already recorded the cost of goods sold in the

Cost of Goods Sold account. Exhibit 56 shows how to determine the cost of ending inventory under

FIFO using perpetual inventory procedure. This illustration uses the same format as the earlier

perpetual inventory record in Exhibit 48. The company keeps a record of the balance in the inventory

account as it makes purchases and sells items from inventory.

Notice in Exhibit 56 that each time a sale occurs, the company assumes the items sold are the oldest

on hand. Thus, after each transaction, it can readily determine the balance in the Merchandise

Inventory account from the perpetual inventory record. The balance after the December 21 purchase

represents the 20 units from the most recent purchases. The total cost of ending inventory is USD 179,

which the company reports as a current asset on the balance sheet. During the accounting period, as

sales occurred the firm would have debited a total of USD 511 to Cost of Goods Sold. Adding this USD

511 to the ending inventory of USD 179 accounts for the USD 690 cost of goods available for sale.

Under FIFO, using either perpetual or periodic inventory procedures results in the same total amounts

for ending inventory and for cost of goods sold.

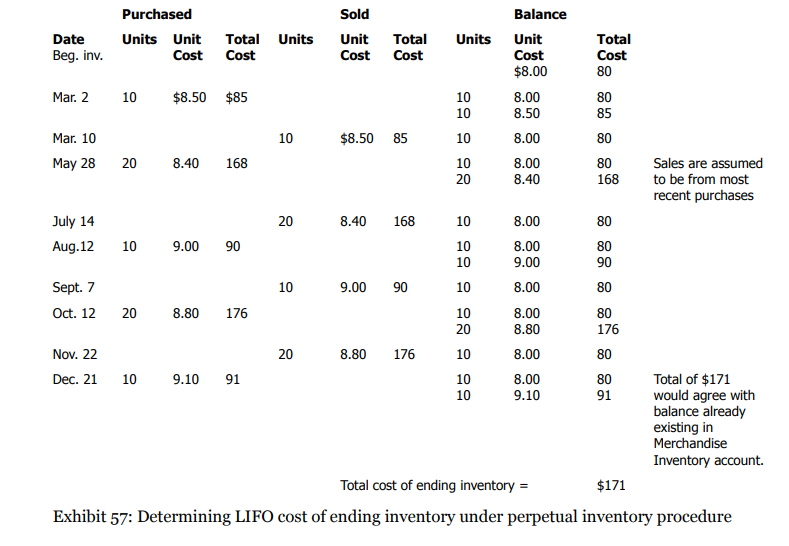

LIFO under perpetual inventory procedure Look at Exhibit 57 to see the LIFO method using

perpetual inventory procedure. Under this procedure, the inventory composition and balance are

updated with each purchase and sale. Notice in Exhibit 57 that each time a sale occurs, the items sold

are assumed to be the most recent ones acquired. Despite numerous purchases and sales during the year, the ending inventory still includes the 10 units from beginning inventory in our example. The

remainder of the ending inventory consists of the last purchase because no sale occurred after the

December 21 purchase. The total cost of the 20 units in ending inventory is USD 171; the cost of goods

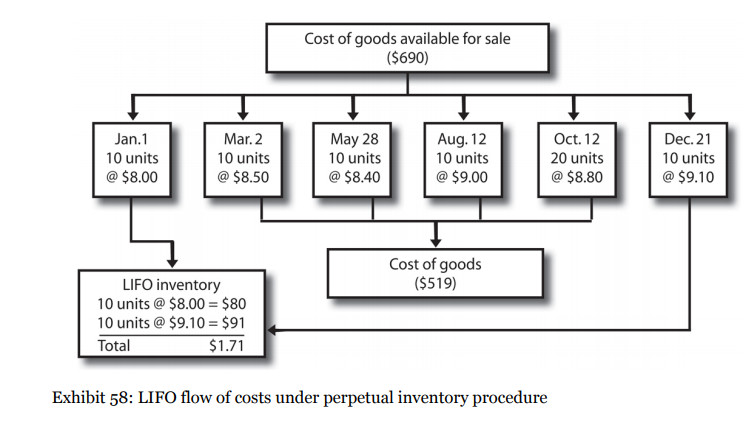

sold is USD 519. Exhibit 58 shows graphically the LIFO flow of costs under perpetual inventory

procedure.

Applying LIFO on a perpetual basis during the accounting period, as shown in Exhibit 57, results in

different ending inventory and cost of goods sold figures than applying LIFO only at year-end using

periodic inventory procedure. (Compare Exhibit 57 and Exhibit 53 to verify that ending inventory and

cost of goods sold are different under the two procedures.) For this reason, if LIFO is applied on a

perpetual basis during the period, special adjustments are sometimes necessary at year-end to take full

advantage of using LIFO for tax purposes. Complicated applications of LIFO perpetual inventory

procedures that require such adjustments are beyond the scope of this text.

Look at Exhibit 58 and Exhibit 54, the flow of inventory costs under LIFO using both the perpetual

and periodic inventory procedures. Note that ending inventory and cost of goods sold are different

under the two procedures

Última modificación: martes, 28 de mayo de 2019, 12:12