Reading: Lesson 3 - Determining inventory cost II

Weighted-average under perpetual inventory procedure Under perpetual inventory

procedure, firms compute a new weighted-average unit cost after each purchase by dividing total cost

of goods available for sale by total units available for sale. The unit cost is a moving weighted-average

because it changes after each purchase. In Exhibit 59, you can see how to compute the moving

weighted-average using perpetual inventory procedure. The new weighted-average unit cost computed

after each purchase is the unit cost for inventory items sold until a new purchase is made. The unit cost

of the 20 units in ending inventory is USD 8.929 for a total inventory cost of USD 178.58. Cost of goods

sold under this procedure is USD 690 minus the USD 178.58, or USD 511.42.

Advantages and disadvantages of specific identification Companies that use the specific

identification method of inventory costing state their cost of goods sold and ending inventory at the

actual cost of specific units sold and on hand. Some accountants argue that this method provides the

most precise matching of costs and revenues and is, therefore, the most theoretically sound method.

This statement is true for some one-of-a-kind items, such as autos or real estate. For these items, use of

any other method would seem illogical.

One disadvantage of the specific identification method is that it permits the manipulation of

income. For example, assume that a company bought three identical units of a given product at

different prices. One unit cost USD 2,000, the second cost USD 2,100, and the third cost USD 2,200.

The company sold one unit for USD 2,800. The units are alike, so the customer does not care which of

the identical units the company ships. However, the gross margin on the sale could be either USD 800,

USD 700, or USD 600, depending on which unit the company ships.

Advantages and disadvantages of FIFO The FIFO method has four major advantages: (1) it is

easy to apply, (2) the assumed flow of costs corresponds with the normal physical flow of goods, (3) no

manipulation of income is possible, and (4) the balance sheet amount for inventory is likely to

approximate the current market value. All the advantages of FIFO occur because when a company sells

goods, the first costs it removes from inventory are the oldest unit costs. A company cannot manipulate

income by choosing which unit to ship because the cost of a unit sold is not determined by a serial

number. Instead, the cost attached to the unit sold is always the oldest cost. Under FIFO, purchases at

the end of the period have no effect on cost of goods sold or net income.

The disadvantages of FIFO include (1) the recognition of paper profits and (2) a heavier tax burden

if used for tax purposes in periods of inflation. We discuss these disadvantages later as advantages of

LIFO.

Advantages and disadvantages of LIFO The advantages of the LIFO method are based on the

fact that prices have risen almost constantly for decades. LIFO supporters claim this upward trend in

prices leads to inventory, or paper, profits if the FIFO method is used. Inventory, or paper, profits

are equal to the current replacement cost of a unit of inventory at the time of sale minus the unit's

historical cost.

For example, assume a company has three units of a product on hand, each purchased at a different

cost: USD 12, USD 15, and USD 20 (the most recent cost). The sales price of the unit normally rises

because the unit's replacement cost is rising. Assume that the company sells one unit for USD 30. FIFO

gross margin would be USD 18 (USD 30 – USD 12), while LIFO would show a gross margin of USD 10

(USD 30 – USD 20). LIFO supporters would say that the extra USD 8 gross margin shown under FIFO represents inventory (paper) profit; it is merely the additional amount that the company must spend

over cost of goods sold to purchase another unit of inventory (USD 8 + USD 12 = USD 20). Thus, the

profit is not real; it exists only on paper. The company cannot distribute the USD 8 to owners, but must

retain it to continue handling that particular product. LIFO shows the actual profits that the company

can distribute to the owners while still replenishing inventory.

During periods of inflation, LIFO shows the largest cost of goods sold of any of the costing methods

because the newest costs charged to cost of goods sold are also the highest costs. The larger the cost of

goods sold, the smaller the net income.

Those who favor LIFO argue that its use leads to a better matching of costs and revenues than the

other methods. When a company uses LIFO, the income statement reports both sales revenue and cost

of goods sold in current dollars. The resulting gross margin is a better indicator of management's

ability to generate income than gross margin computed using FIFO, which may include substantial

inventory (paper) profits.

Supporters of FIFO argue that LIFO (1) matches the cost of goods not sold against revenues, (2)

grossly understates inventory, and (3) permits income manipulation.

The first criticism—that LIFO matches the cost of goods not sold against revenues—is an extension

of the debate over whether the assumed flow of costs should agree with the physical flow of goods.

LIFO supporters contend that it makes more sense to match current costs against current revenues

than to worry about matching costs for the physical flow of goods.

The second criticism—that LIFO grossly understates inventory—is valid. A company may report

LIFO inventory at a fraction of its current replacement cost, especially if the historical costs are from

several decades ago. LIFO supporters contend that the increased usefulness of the income statement

more than offsets the negative effect of this undervaluation of inventory on the balance sheet.

The third criticism—that LIFO permits income manipulation—is also valid. Income manipulation is

possible under LIFO. For example, assume that management wishes to reduce income. The company

could purchase an abnormal amount of goods at current high prices near the end of the current period,

with the purpose of selling the goods in the next period. Under LIFO, these higher costs are charged to

cost of goods sold in the current period, resulting in a substantial decline in reported net income. To

obtain higher income, management could delay making the normal amount of purchases until the next

period and thus include some of the older, lower costs in cost of goods sold.

Tax benefit of LIFO The LIFO method results in the lowest taxable income, and thus the lowest

income taxes, when prices are rising. The Internal Revenue Service allows companies to use LIFO for

tax purposes only if they use LIFO for financial reporting purposes. Companies may also report an alternative inventory amount in the notes to their financial statements for comparison purposes.

Because of high inflation during the 1970s, many companies switched from FIFO to LIFO for tax

advantages.

Advantages and disadvantages of weighted-average When a company uses the weightedaverage

method and prices are rising, its cost of goods sold is less than that obtained under LIFO, but

more than that obtained under FIFO. Inventory is not as badly understated as under LIFO, but it is not

as up-to-date as under FIFO. Weighted-average costing takes a middle-of-the-road approach. A

company can manipulate income under the weighted-average costing method by buying or failing to

buy goods near year-end. However, the averaging process reduces the effects of buying or not buying.

The four inventory costing methods, specific identification, FIFO, LIFO, and weighted-average,

involve assumptions about how costs flow through a business. In some instances, assumed cost flows

may correspond with the actual physical flow of goods. For example, fresh meats and dairy products

must flow in a FIFO manner to avoid spoilage losses. In contrast, firms use coal stacked in a pile in a

LIFO manner because the newest units purchased are unloaded on top of the pile and sold first.

Gasoline held in a tank is a good example of an inventory that has an average physical flow. As the tank

is refilled, the new gasoline mixes with the old. Thus, any amount used is a blend of the old gas with the

new.

Although physical flows are sometimes cited as support for an inventory method, accountants now

recognize that an inventory method's assumed cost flows need not necessarily correspond with the

actual physical flow of the goods. In fact, good reasons exist for simply ignoring physical flows and

choosing an inventory method based on other criteria.

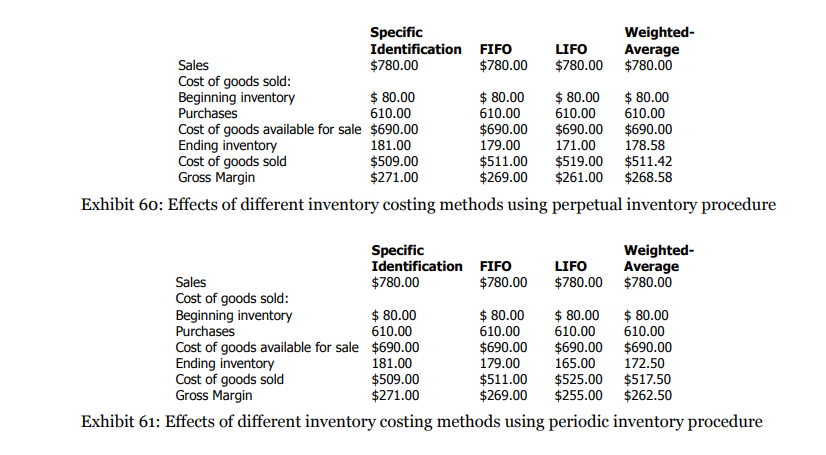

In Exhibit 60 and Exhibit 61, we use data from Exhibit 49 to show the cost of goods sold, inventory

cost, and gross margin for each of the four basic costing methods using perpetual and periodic

inventory procedures. The differences for the four methods occur because the company paid different

prices for goods purchased. No differences would occur if purchase prices were constant. Since a

company's purchase prices are seldom constant, inventory costing method affects cost of goods sold,

inventory cost, gross margin, and net income. Therefore, companies must disclose on their financial

statements which inventory costing methods were used.

Which is the correct method? All four methods of inventory costing are acceptable; no single

method is the only correct method. Different methods are attractive under different conditions.

If a company wants to match sales revenue with current cost of goods sold, it would use LIFO. If a

company seeks to reduce its income taxes in a period of rising prices, it would also use LIFO. On the other hand, LIFO often charges against revenues the cost of goods not actually sold. Also, LIFO may

allow the company to manipulate net income by changing the timing of additional purchases.

The FIFO and specific identification methods result in a more precise matching of historical cost

with revenue. However, FIFO can give rise to paper profits, while specific identification can give rise to

income manipulation. The weighted-average method also allows manipulation of income. Only under

FIFO is the manipulation of net income not possible.

Generally, companies use the inventory method that best fits their individual circumstances.

However, this freedom of choice does not include changing inventory methods every year or so,

especially if the goal is to report higher income. Continuous switching of methods violates the

accounting principle of consistency, which requires using the same accounting methods from period to

period in preparing financial statements. Consistency of methods in preparing financial statements

enables financial statement users to compare statements of a company from period to period and

determine trends.

Now we illustrate in more detail the journal entries made when using perpetual inventory

procedure. Data from Exhibit 56 serves as the basis for some of the entries.

You would debit the Merchandise Inventory account to record the increases in the asset due to

purchase costs and transportation-in costs. You would credit Merchandise Inventory to record the

decreases in the asset brought about by purchase returns and allowances, purchase discounts, and cost

of goods sold to customers. The balance in the account is the cost of the inventory that should be on

hand at any date. This entry records the purchase of 10 units on March 2 in Exhibit 56:

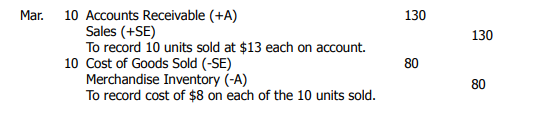

You would also record the 10 units sold on the perpetual inventory record in Exhibit 56. Perpetual

inventory procedure requires two journal entries for each sale. One entry is at selling price—a debit to

Accounts Receivable (or Cash) and a credit to Sales. The other entry is at cost—a debit to Cost of Goods

Sold and a credit to Merchandise Inventory. Assuming that the 10 units sold on March 10 in Exhibit 56

had a retail price of USD 13 each, you would record the following entries:

When a company sells merchandise to customers, it transfers the cost of the merchandise from an

asset account (Merchandise Inventory) to an expense account (Cost of Goods Sold). The company

makes this transfer because the sale reduces the asset, and the cost of the goods sold is one of the

expenses of making the sale. Thus, the Cost of Goods Sold account accumulates the cost of all the

merchandise that the company sells during a period.

A sales return also requires two entries, one at selling price and one at cost. Assume that a customer

returned merchandise that cost USD 20 and originally sold for USD 32. The entry to reduce the

accounts receivable and to record the sales return of USD 32 is:

The entry that increases the Merchandise Inventory account and decreases the Cost of Goods Sold

account by USD 20 is as follows:

Sales returns affect both revenues and cost of goods sold because the goods charged to cost of goods

sold are actually returned to the seller. In contrast, sales allowances granted to customers affect only

revenues because the customers do not have to return goods. Thus, if the company had granted a sales

allowance of USD 32 on March 17, only the first entry would be required.

The balance of the Merchandise Inventory account is the cost of the inventory that should be on

hand. This fact is a major reason some companies choose to use perpetual inventory procedure. The

cost of inventory that should be on hand is readily available. A physical inventory determines the

accuracy of the account balance. Management may investigate any major discrepancies between the

balance in the account and the cost based on the physical count. It thereby achieves greater control

over inventory. When a shortage is discovered, an adjusting entry is required. Assuming a USD 15

shortage (at cost) is discovered, the entry is:

Assume that the Cost of Goods Sold account had a balance of USD 200,000 by year-end when it is

closed to Income Summary. There are no other purchase-related accounts to be closed. The entry to

close the Cost of Goods Sold account is:

Последнее изменение: вторник, 28 мая 2019, 12:12