Reading: Lesson 1 - Accounts receivable

Under the

accrual basis, a merchandising company that extends credit records revenue when it

makes a sale because at this time it has earned and realized the revenue. The company

has earned the revenue because it has completed the seller's part of the sales contract

by delivering the goods. The company has realized the revenue because it has received

the customer's promise to pay in exchange for the goods. This promise to pay by the

customer is an account receivable to the seller. Accounts receivable are amounts that

customers owe a company for goods sold and services rendered on account.

Frequently, these receivables resulting from credit sales of goods and services are

called trade receivables.

When a company sells goods on account, customers do not sign formal, written

promises to pay, but they agree to abide by the company's customary credit terms.

However, customers may sign a sales invoice to acknowledge purchase of goods.

Payment terms for sales on account typically run from 30 to 60 days. Companies

usually do not charge interest on amounts owed, except on some past-due amounts. Because customers do not always keep their promises to pay, companies must

provide for these uncollectible accounts in their records. Companies use two methods

for handling uncollectible accounts. The allowance method provides in advance for

uncollectible accounts. The direct write-off method recognizes bad accounts as an

expense at the point when judged to be uncollectible and is the required method for

federal income tax purposes. However, since the allowance method represents the

accrual basis of accounting and is the accepted method to record uncollectible accounts

for financial accounting purposes, we only discuss and illustrate the allowance method

in this text.

Even though companies carefully screen credit customers, they cannot eliminate all

uncollectible accounts. Companies expect some of their accounts to become

uncollectible, but they do not know which ones. The matching principle requires

deducting expenses incurred in producing revenues from those revenues during the

accounting period. The allowance method of recording uncollectible accounts adheres

to this principle by recognizing the uncollectible accounts expense in advance of

identifying specific accounts as being uncollectible. The required entry has some

similarity to the depreciation entry in Chapter 3 because it debits an expense and

credits an allowance (contra asset). The purpose of the entry is to make the income

statement fairly present the proper expense and the balance sheet fairly present the

asset. Uncollectible accounts expense (also called doubtful accounts expense or

bad debts expense) is an operating expense that a business incurs when it sells on

credit. We classify uncollectible accounts expense as a selling expense because it results

from credit sales. Other accountants might classify it as an administrative expense

because the credit department has an important role in setting credit terms.

To adhere to the matching principle, companies must match the uncollectible

accounts expense against the revenues it generates. Thus, an uncollectible account

arising from a sale made in 2010 is a 2010 expense even though this treatment requires

the use of estimates. Estimates are necessary because the company sometimes cannot

determine until 2008 or later which 2010 customer accounts will become uncollectible. Recording the uncollectible accounts adjustment A company that estimates

uncollectible accounts makes an adjusting entry at the end of each accounting period.

It debits Uncollectible Accounts Expense, thus recording the operating expense in the

proper period. The credit is to an account called Allowance for Uncollectible Accounts.

As a contra account to the Accounts Receivable account, the Allowance for

Uncollectible Accounts (also called Allowance for doubtful accounts or Allowance

for bad debts) reduces accounts receivable to their net realizable value. Net

realizable value is the amount the company expects to collect from accounts

receivable. When the firm makes the uncollectible accounts adjusting entry, it does not

know which specific accounts will become uncollectible. Thus, the company cannot

enter credits in either the Accounts Receivable control account or the customers'

accounts receivable subsidiary ledger accounts. If only one or the other were credited, the Accounts Receivable control account balance would not agree with the total of the

balances in the accounts receivable subsidiary ledger. Without crediting the Accounts

Receivable control account, the allowance account lets the company show that some of

its accounts receivable are probably uncollectible.

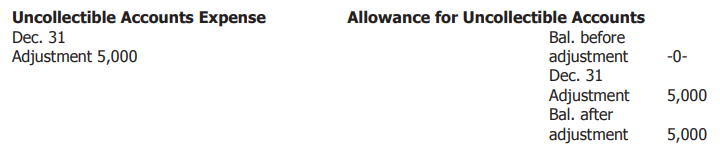

To illustrate the adjusting entry for uncollectible accounts, assume a company has

USD 100,000 of accounts receivable and estimates its uncollectible accounts expense

for a given year at USD 4,000. The required year-end adjusting entry is:

The debit to Uncollectible Accounts Expense brings about a matching of expenses

and revenues on the income statement; uncollectible accounts expense is matched

against the revenues of the accounting period. The credit to Allowance for

Uncollectible Accounts reduces accounts receivable to their net realizable value on the

balance sheet. When the books are closed, the firm closes Uncollectible Accounts

Expense to Income Summary. It reports the allowance on the balance sheet as a

deduction from accounts receivable as follows:

Estimating uncollectible accounts Accountants use two basic methods to

estimate uncollectible accounts for a period. The first method—percentage-of-sales

method—focuses on the income statement and the relationship of uncollectible

accounts to sales. The second method—percentage-of-receivables method—focuses on

the balance sheet and the relationship of the allowance for uncollectible accounts to

accounts receivable.

Percentage-of-sales method The percentage-of-sales method estimates

uncollectible accounts from the credit sales of a given period. In theory, the method is

based on a percentage of prior years' actual uncollectible accounts to prior years' credit

sales. When cash sales are small or make up a fairly constant percentage of total sales,

firms base the calculation on total net sales. Since at least one of these conditions is usually met, companies commonly use total net sales rather than credit sales. The

formula to determine the amount of the entry is:

Amount of journal entry for uncollectible accounts – Net sales (total or credit) x

Percentage estimated as uncollectible

To illustrate, assume that Rankin Company's uncollectible accounts from 2008 sales

were 1.1 percent of total net sales. A similar calculation for 2009 showed an

uncollectible account percentage of 0.9 percent. The average for the two years is 1

percent [(1.1 +0.9)/2]. Rankin does not expect 2010 to differ from the previous two

years. Total net sales for 2010 were USD 500,000; receivables at year-end were USD

100,000; and the Allowance for Uncollectible Accounts had a zero balance. Rankin

would make the following adjusting entry for 2010:

Using T-accounts, Rankin would show:

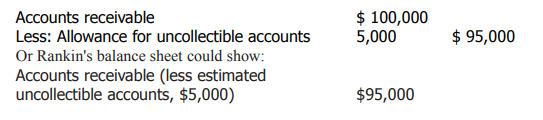

Rankin reports Uncollectible Accounts Expense on the income statement. It reports

the accounts receivable less the allowance among current assets in the balance sheet as

follows:

On the income statement, Rankin would match the uncollectible accounts expense

against sales revenues in the period. We would classify this expense as a selling expense

since it is a normal consequence of selling on credit.

The Allowance for Uncollectible Accounts account usually has either a debit or

credit balance before the year-end adjustment. Under the percentage-of-sales method,

the company ignores any existing balance in the allowance when calculating the amount of the year-end adjustment (except that the allowance account must have a

credit balance after adjustment).

For example, assume Rankin's allowance account had a USD 300 credit balance

before adjustment. The adjusting entry would still be for USD 5,000. However, the

balance sheet would show USD 100,000 accounts receivable less a USD 5,300

allowance for uncollectible accounts, resulting in net receivables of USD 94,700. On

the income statement, Uncollectible Accounts Expense would still be 1 percent of total

net sales, or USD 5,000.

In applying the percentage-of-sales method, companies annually review the

percentage of uncollectible accounts that resulted from the previous year's sales. If the

percentage rate is still valid, the company makes no change. However, if the situation

has changed significantly, the company increases or decreases the percentage rate to

reflect the changed condition. For example, in periods of recession and high

unemployment, a firm may increase the percentage rate to reflect the customers'

decreased ability to pay. However, if the company adopts a more stringent credit

policy, it may have to decrease the percentage rate because the company would expect

fewer uncollectible accounts.

Percentage-of-receivables method The percentage-of-receivables

method estimates uncollectible accounts by determining the desired size of the

Allowance for Uncollectible Accounts. Rankin would multiply the ending balance in

Accounts Receivable by a rate (or rates) based on its uncollectible accounts experience.

In the percentage-of-receivables method, the company may use either an overall rate or

a different rate for each age category of receivables.

To calculate the amount of the entry for uncollectible accounts under the

percentage-of-receivables method using an overall rate, Rankin would use:

Amount of entry for uncollectible accounts – (Accounts receivable ending balance x

percentage estimated as uncollectible) – Existing credit balance in allowance for

uncollectible accounts or existing debit balance in allowance for uncollectible accounts.

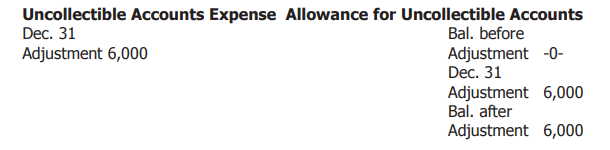

Using the same information as before, Rankin makes an estimate of uncollectible

accounts at the end of 2010. The balance of accounts receivable is USD 100,000, and

the allowance account has no balance. If Rankin estimates that 6 percent of the

receivables will be uncollectible, the adjusting entry would be:

![]()

Using T-accounts, Rankin would show:

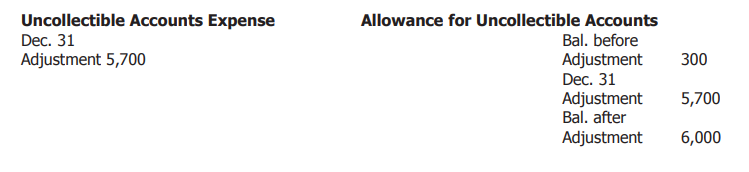

If Rankin had a USD 300 credit balance in the allowance account before

adjustment, the entry would be the same, except that the amount of the entry would be

USD 5,700. The difference in amounts arises because management wants the

allowance account to contain a credit balance equal to 6 percent of the outstanding

receivables when presenting the two accounts on the balance sheet. The calculation of

the necessary adjustment is [(USD 100,000 X 0.06)-USD 300] = USD 5,700. Thus,

under the percentage-of-receivables method, firms consider any existing balance in the

allowance account when adjusting for uncollectible accounts. Using T-accounts,

Rankin would show:

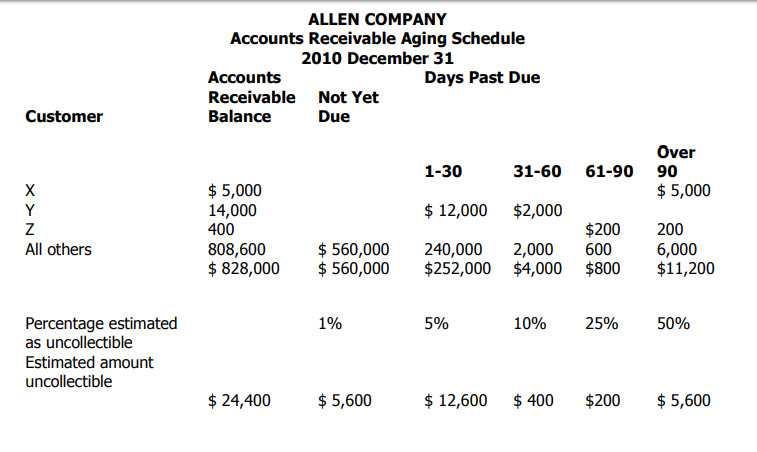

Exhibit 1: Accounts receivable aging schedule

As another example, suppose that Rankin had a USD 300 debit balance in the

allowance account before adjustment. Then, a credit of USD 6,300 would be necessary

to get the balance to the required USD 6,000 credit balance. The calculation of the

necessary adjustment is [(USD 100,000 X 0.06) + USD 300] = USD 6,300. Using Taccounts,

Rankin would show:

No matter what the pre-adjustment allowance account balance is, when using the

percentage-of-receivables method, Rankin adjusts the Allowance for Uncollectible

Accounts so that it has a credit balance of USD 6,000—equal to 6 percent of its USD

100,000 in Accounts Receivable. The desired USD 6,000 ending credit balance in the

Allowance for Uncollectible Accounts serves as a "target" in making the adjustment.

So far, we have used one uncollectibility rate for all accounts receivable, regardless

of their age. However, some companies use a different percentage for each age category

of accounts receivable. When accountants decide to use a different rate for each age

category of receivables, they prepare an aging schedule. An aging schedule classifies

accounts receivable according to how long they have been outstanding and uses a

different uncollectibility percentage rate for each age category. Companies base these

percentages on experience. In Exhibit 1, the aging schedule shows that the older the

receivable, the less likely the company is to collect it.

Classifying accounts receivable according to age often gives the company a better

basis for estimating the total amount of uncollectible accounts. For example, based on

experience, a company can expect only 1 percent of the accounts not yet due (sales

made less than 30 days before the end of the accounting period) to be uncollectible. At

the other extreme, a company can expect 50 percent of all accounts over 90 days past

due to be uncollectible. For each age category, the firm multiplies the accounts

receivable by the percentage estimated as uncollectible to find the estimated amount

uncollectible.

The sum of the estimated amounts for all categories yields the total estimated

amount uncollectible and is the desired credit balance (the target) in the Allowance for

Uncollectible Accounts.

Since the aging schedule approach is an alternative under the percentage-ofreceivables

method, the balance in the allowance account before adjustment affects the

year-end adjusting entry amount recorded for uncollectible accounts. For example, the

schedule in Exhibit 1 shows that USD 24,400 is needed as the ending credit balance in

the allowance account. If the allowance account has a USD 5,000 credit balance before

adjustment, the adjustment would be for USD 19,400.

The information in an aging schedule also is useful to management for other

purposes. Analysis of collection patterns of accounts receivable may suggest the need

for changes in credit policies or for added financing. For example, if the age of many

customer balances has increased to 61-90 days past due, collection efforts may have to

be strengthened. Or, the company may have to find other sources of cash to pay its

debts within the discount period. Preparation of an aging schedule may also help

identify certain accounts that should be written off as uncollectible.

Write-off of receivables As time passes and a firm considers a specific

customer's account to be uncollectible, it writes that account off. It debits the

Allowance for Uncollectible Accounts. The credit is to the Accounts Receivable control

account in the general ledger and to the customer's account in the accounts receivable

subsidiary ledger. For example, assume Smith's USD 750 account has been determined

to be uncollectible. The entry to write off this account is:

The credit balance in Allowance for Uncollectible Accounts before making this entry

represented potential uncollectible accounts not yet specifically identified. Debiting the

allowance account and crediting Accounts Receivable shows that the firm has

identified Smith's account as uncollectible. Notice that the debit in the entry to write

off an account receivable does not involve recording an expense. The company

recognized the uncollectible accounts expense in the same accounting period as the

sale. If Smith's USD 750 uncollectible account were recorded in Uncollectible Accounts

Expense again, it would be counted as an expense twice.

A write-off does not affect the net realizable value of accounts receivable. For

example, suppose that Amos Company has total accounts receivable of USD 50,000

and an allowance of USD 3,000 before the previous entry; the net realizable value of

the accounts receivable is USD 47,000. After posting that entry, accounts receivable

are USD 49,250, and the allowance is USD 2,250; net realizable value is still USD

47,000, as shown here:

You might wonder how the allowance account can develop a debit balance before

adjustment. To explain this, assume that Jenkins Company began business on 2009

January 1, and decided to use the allowance method and make the adjusting entry for

uncollectible accounts only at year-end. Thus, the allowance account would not have

any balance at the beginning of 2009. If the company wrote off any uncollectible

accounts during 2009, it would debit Allowance for Uncollectible Accounts and cause a

debit balance in that account. At the end of 2009, the company would debit

Uncollectible Accounts Expense and credit Allowance for Uncollectible Accounts. This

adjusting entry would cause the allowance account to have a credit balance. During

2010, the company would again begin debiting the allowance account for any write-offs

of uncollectible accounts. Even if the adjustment at the end of 2009 was adequate to

cover all accounts receivable existing at that time that would later become

uncollectible, some accounts receivable from 2010 sales may be written off before the

end of 2010. If so, the allowance account would again develop a debit balance before

the end-of-year 2010 adjustment.

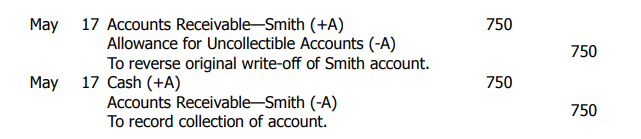

Uncollectible accounts recovered Sometimes companies collect accounts

previously considered to be uncollectible after the accounts have been written off. A

company usually learns that an account has been written off erroneously when it

receives payment. Then the company reverses the original write-off entry and

reinstates the account by debiting Accounts Receivable and crediting Allowance for

Uncollectible Accounts for the amount received. It posts the debit to both the general

ledger account and to the customer's accounts receivable subsidiary ledger account.

The firm also records the amount received as a debit to Cash and a credit to Accounts

Receivable. And it posts the credit to both the general ledger and to the customer's

accounts receivable subsidiary ledger account.

To illustrate, assume that on May 17 a company received a USD 750 check from

Smith in payment of the account previously written off. The two required journal

entries are:

The debit and credit to Accounts Receivable—Smith on the same date is to show in

Smith's subsidiary ledger account that he did eventually pay the amount due. As a

result, the company may decide to sell to him in the future.

When a company collects part of a previously written off account, the usual

procedure is to reinstate only that portion actually collected, unless evidence indicates

the amount will be collected in full. If a company expects full payment, it reinstates the

entire amount of the account.

Because of the problems companies have with uncollectible accounts when they

offer customers credit, many now allow customers to use bank or external credit cards.

This policy relieves the company of the headaches of collecting overdue accounts.

Credit cards are either nonbank (e.g. American Express) or bank (e.g. VISA and

MasterCard) charge cards that customers use to purchase goods and services. For

some businesses, uncollectible account losses and other costs of extending credit are a

burden. By paying a service charge of 2 percent to 6 percent, businesses pass these

costs on to banks and agencies issuing national credit cards. The banks and credit card

agencies then absorb the uncollectible accounts and costs of extending credit and

maintaining records.

Usually, banks and agencies issue credit cards to approved credit applicants for an

annual fee. When a business agrees to honor these credit cards, it also agrees to pay the

percentage fee charged by the bank or credit agency.

When making a credit card sale, the seller checks to see if the customer's card has

been canceled and requests approval if the sale exceeds a prescribed amount, such as

USD 50. This procedure allows the seller to avoid accepting lost, stolen, or canceled cards. Also, this policy protects the credit agency from sales causing customers to

exceed their established credit limits.

The seller's accounting procedures for credit card sales differ depending on whether

the business accepts a nonbank or a bank credit card. To illustrate the entries for the

use of nonbank credit cards (such as American Express), assume that a restaurant

American Express invoices amounting to USD 1,400 at the end of a day. American

Express charges the restaurant a 5 percent service charge. The restaurant uses the

Credit Card Expense account to record the credit card agency's service charge and

makes the following entry:

The restaurant mails the invoices to American Express. Sometime later, the

restaurant receives payment from American Express and makes the following entry:

To illustrate the accounting entries for the use of bank credit cards (such as VISA or

MasterCard), assume that a retailer has made sales of USD 1,000 for which VISA cards

were accepted and the service charge is USD 30 (which is 3 percent of sales). VISA

sales are treated as cash sales because the receipt of cash is certain. The retailer

deposits the credit card sales invoices in its VISA checking account at a bank just as it

deposits checks in its regular checking account. The entry to record this deposit is:

Just as every company must have current assets such as cash and accounts receivable to operate, every company incurs current liabilities in conducting its operations. Corporations (IBM and General Motors), partnerships (CPA firms), and single proprietorships (corner grocery stores) all have one thing in common—they have liabilities. The next section discusses some of the current liabilities companies incur.

最后修改: 2019年05月28日 星期二 12:13