Reading: Lesson 4 - The Business Transactions

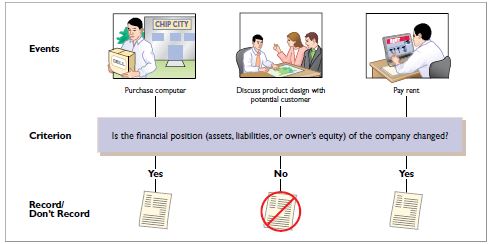

The business transactions represent economic events that take place during the course of the day to day business operations. These events must be able to be reliably recorded. Businesses conduct many activities that do not represent business transactions. The transactions are analyzed to determine if the events affect the components of the accounting equation.

The following transactions illustrate the business transaction analysis:

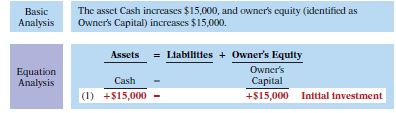

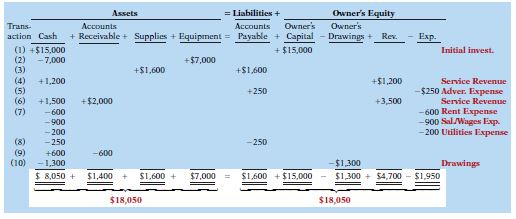

Transaction (1) INVESTMENT BY OWNER: Owner invests $15,000 cash into the business.

Note that the Cash received from the business is not recorded as revenue. The accounting equation remains intake, assets = liabilities + owner's equity.

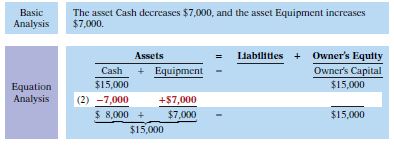

Transaction (2) PURCHASE OF EQUIPMENT FOR CASH: Computer equipment purchased for $7,000 cash.

The asset and owner's equity remains at $15,000.

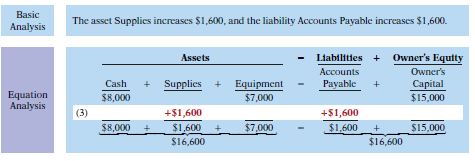

Transaction (3). PURCHASE OF SUPPLIES ON CREDIT. Supplies purchased on credit for $1,600.

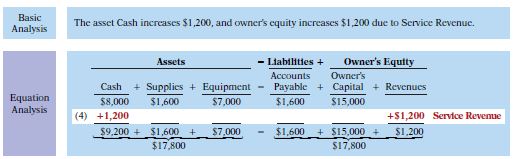

Transaction (4). SERVICES PERFORMED FOR CASH. Received $1,200 cash for services performed.

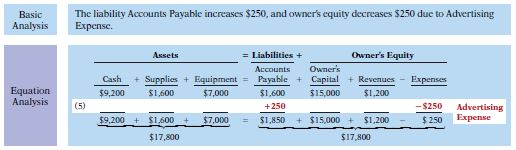

Transaction (5). PURCHASE OF ADVERTISING ON CREDIT. A bill for advertising is received in the amount $250.

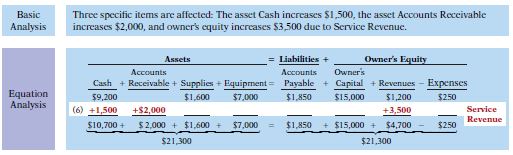

Transaction (6) SERVICES PERFORMED FOR CASH AND CREDIT Company performed $3,500 worth of services Customer pays $1,500 in cash and the remainder is billed at $2,000 on account.

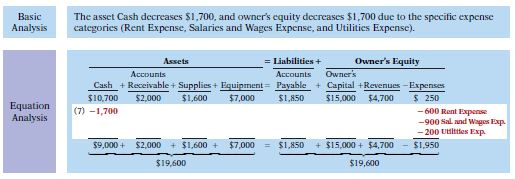

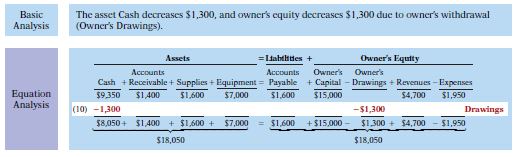

Transaction (7). PAYMENT OF EXPENSES The following expenses were paid with cash, $600 office rent, $900 salaries and wages of employees, $200 utilities.

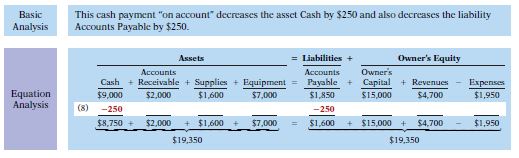

Transaction (8). PAYMENT OF ACCOUNTS PAYABLE Owner pays $250 in cash for a bill from transaction (5).

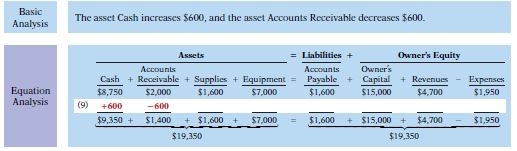

Transaction (9). RECEIPT OF CASH ON ACCOUNT. Received $600 in cash from customers who were billed for services.

Below is the summary of all ten transactions. Please note that during the recording of these transactions, both sides of the equation remained in balance. The equation must always remain in balance.

When evaluating a business transaction, they are analyzed for their effect on the three components of the basic accounting equation and the specific items within each component.

Последнее изменение: вторник, 28 мая 2019, 12:04