Reading: Lesson 4 - Financial Statements and Their Preparation

After the business transactions have been analyzed and journalized, they are used to construct the four primary financial statements.

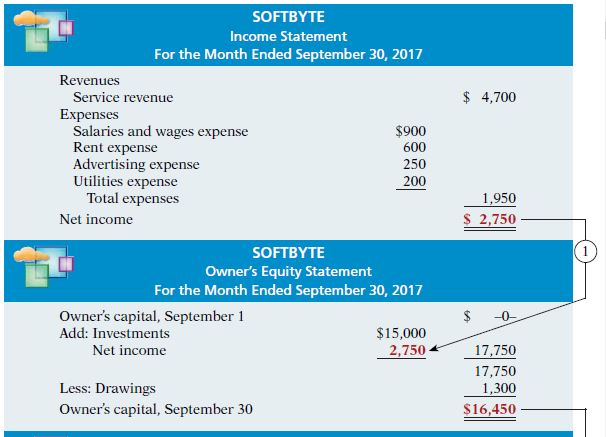

1.) Income Statement. This statement represents the revenues and expenses. The net of the two will either be a net income or net loss. This report is for a specific period of time. The statement lists the Revenues first, then the expenses. If the revenues exceed the expenses then Net Income results. If the expenses exceed the revenues then Net Loss occurs.

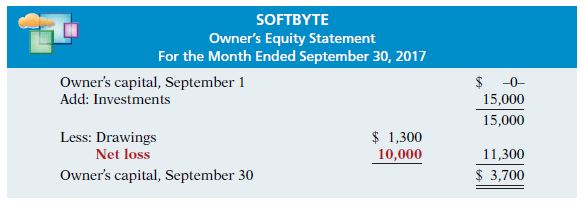

2.) Owner's Equity Statement. This statement shows the changes in the owner's equity for the same specific period of time as the income statement. It shows why the owner's equity was increased or decreased. Net income and Net losses are in different areas of the statement.

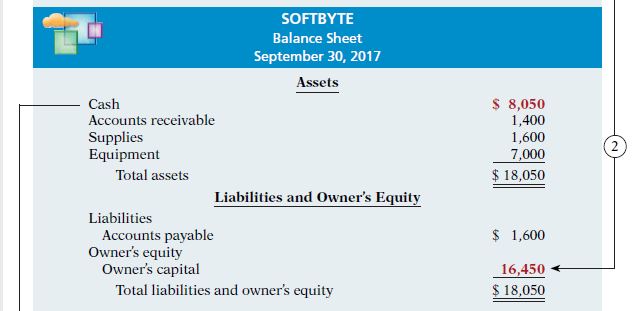

3.) Balance Sheet. It is a snapshot of the company's financial condition. The date on the statement is for a specific date. The balance sheet lists the company's assets, liabilities and owner's equity. The assets are listed first, then the liabilities and finally the owner's equity.

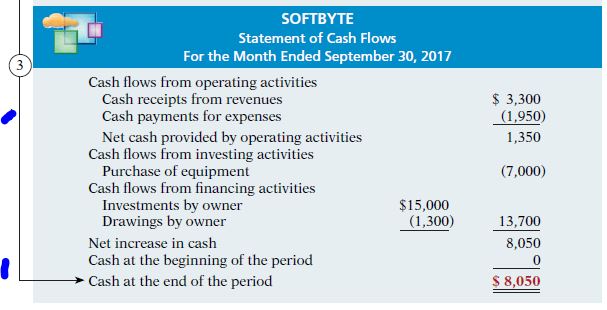

4.) Statement of Cash Flows. This statement represents the cash receipts and payments for a specific period of time. It reports the cash effects of a company's operations, its investing activities, its financing activities, the net increase or decrease in cash, and the cash amount at the end of the period.

We will go into financial statements in more depth later in the class.

The following is the recording of a net loss:

最后修改: 2019年05月28日 星期二 12:04