Reading: Lesson 6 - Recording Process - Journals, Ledgers, and the Trial Balance

THE RECORDING PROCESS

The transaction begins the recording process. First, each transaction is analyzed for its effects on the accounts. Then the transaction information is entered in a journal. Finally, the journal information is transferred to the ledger.

Business documents provide the evidence for the transaction. Sales receipts, a check from a customer, a bill from a vendor are all types of business documents. The documents will be examined to determine the effects it will have on the accounts. Once the accounts that are being affected are determined, the information will be entered in the journal. Finally, based on the journal entry, the information will be entered in the ledger.

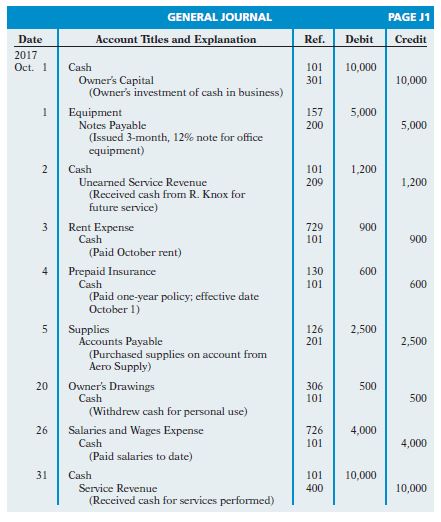

The book of original entry is referred to as the journal. Usually, the journal will have spaces for dates, account titles and explanations, references, and two amount columns. The two columns represent the debits and the credits.

There are three significant contributions that the journal makes to recording process:

1.) The complete effects of the transaction are disclosed in one area.

2.) The journal provides a chronological record of the transactions.

3.) The debit and credit amounts are easily compared, providing help in locating and preventing errors.

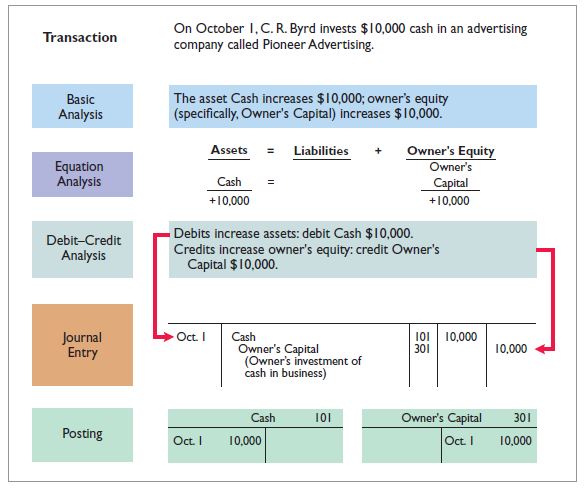

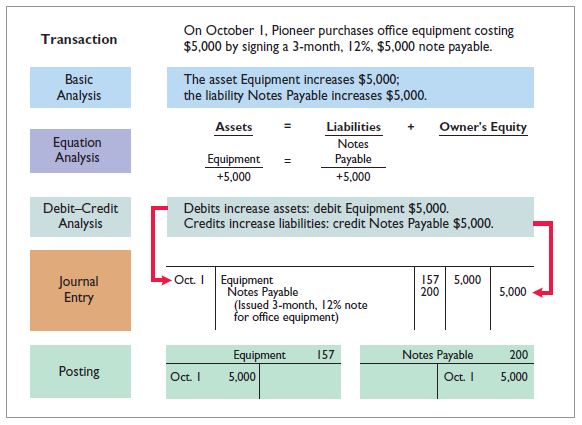

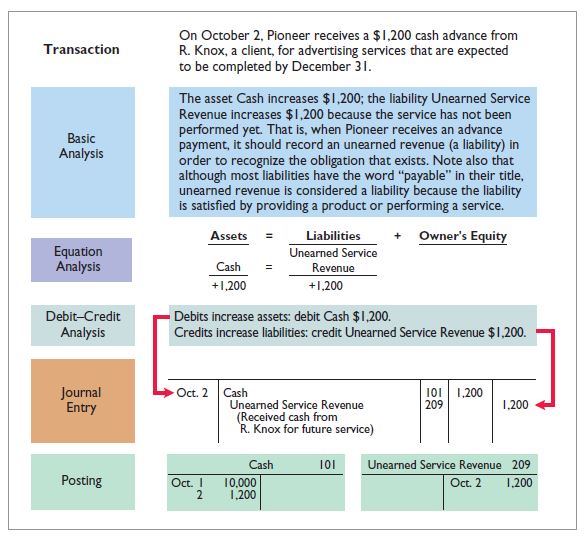

When the data from the transaction is entered in the journal, this is known as journalizing. Each transaction will have its own journal entry. In order for an entry to be complete, it needs the date of the transaction, the accounts and amounts that are to be debited and credited, a brief explanation of the transaction, and a reference.

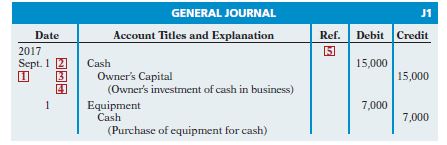

The above demonstrates a proper journal entry. The numbers in the red boxes represent the following:

1 - The date of the transaction

2 - "Cash" is the debit account title. The debit accounts are listed first and to the far left of the margin of the column. The debit amount is listed under the "Debit Column".

3 - "Owner's Capital" is the credit account title. It is indented on the next line down. The credit amount is listed under the "Credit column".

4 - A brief explanation is listed on the next line down. A blank space will separate the journal entries. The journal is easier to read when there is a space between the entries.

5 - A reference column. It is left blank until the entries are ready to be transferred to the ledger accounts.

A simple entry consists of two accounts, one debit and one credit. A compound entry consists of three or more accounts. The standard format for compound entries requires that the debit accounts are listed before the credit accounts.

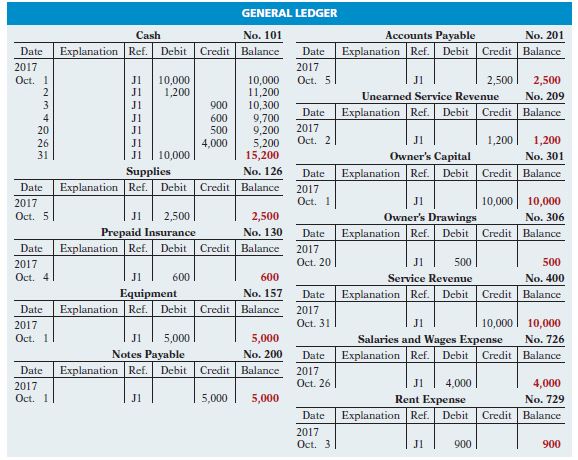

THE LEDGER

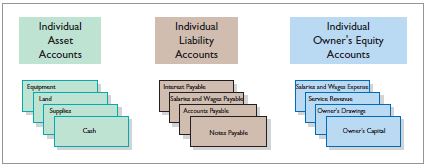

The ledger is the entire group of accounts that a company maintains. It keeps track of the all the balances and changes to the balances of each account. There are various types of ledgers. The most common type of ledger is the general ledger. Every company has this type of ledger. This ledger contains all the asset, liability and owner's equity accounts.

The ledger is arranged based on how the accounts present in the financial statements, beginning with the balance sheet accounts. They consist of assets, liabilities, and owner's capital, the owner's drawing, revenues, and expenses. The accounts are numbered so that they can be identified easier.

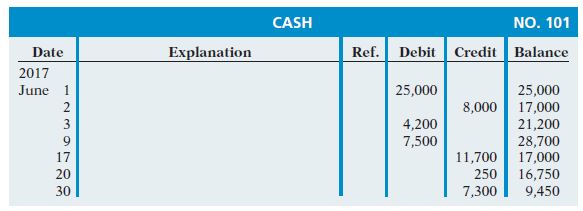

The format of the account is called the three-column form of account. There are three money columns. They are the debit, credit, and balance. The explanation and ref. columns are used to provide information about the transaction.

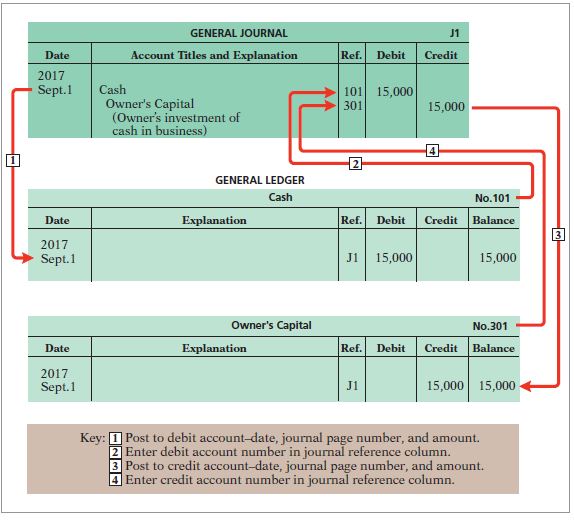

Posting is when the journal entries are transferred to the ledger. The following is a step by step process of posting:

The posting of entries is performed in chronological order. One journal entry should be posted in completion before posting the next. The entries should be posted in a timely manner, so the ledger remains up-to-date. The explanation column in the ledger is hardly ever used because the explanation for the entry is recorded in the journal entry.

THE CHART OF ACCOUNTS

Each business will determine how detailed they want their accounts to be. For instance, one business may decide to have a "utilities account" to post all of the gas, electric and water entries. Where another company may choose to have individual accounts for the gas, electric and water. This is at the sole discretion of the business.

The chart of accounts lists the name and number of each account in the general ledger. The number of the account identifies where the account is located in the ledger. Normally, the numbering system starts with the balance sheet accounts and end with the income statement accounts. Asset accounts are indicated by the numbers 100 - 199, liability accounts by 200 - 299, owner's equity accounts by 300-399, revenues accounts by 400 - 499, expense accounts by 600 - 999.

The account numbers can be in a format based on the businesses needs. An account number can contain an account, a department, and a region number -- 631-421-302, supplies expense for department 421 in region 302.

Gaps are between numbers so that future accounts can be added as needed.

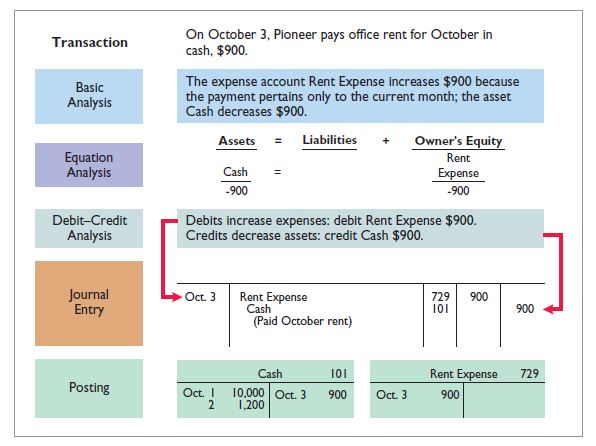

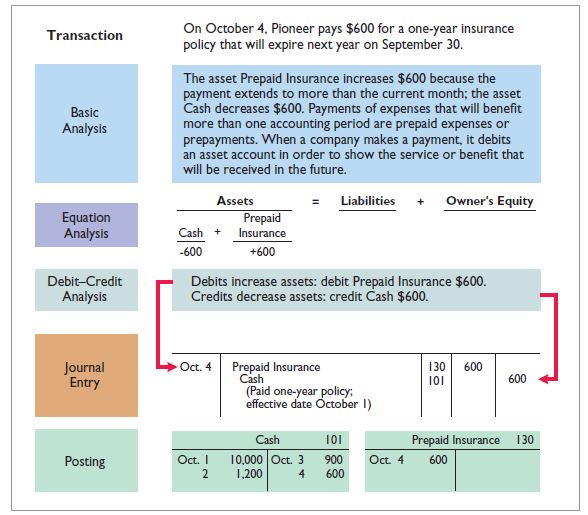

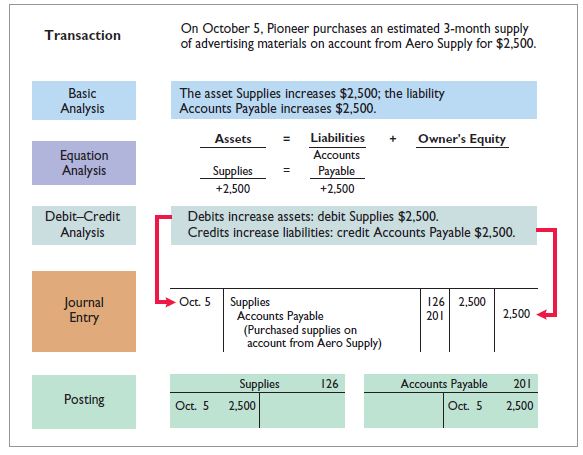

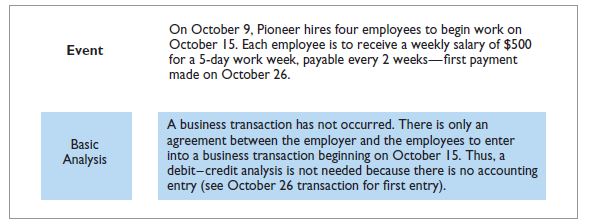

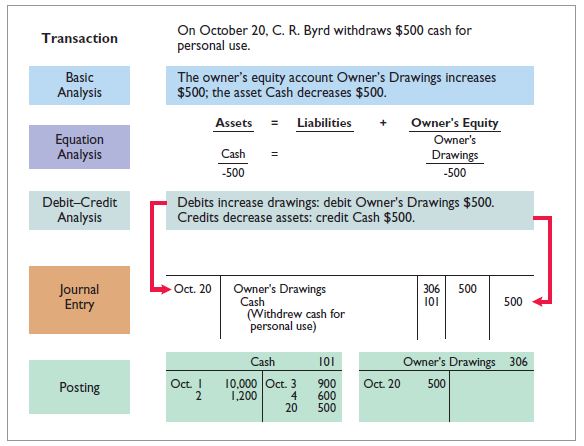

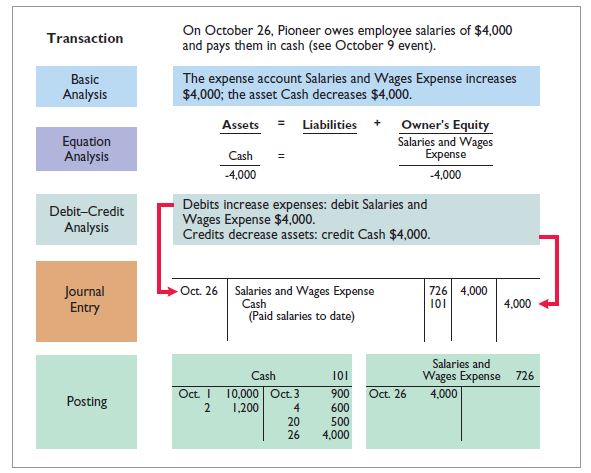

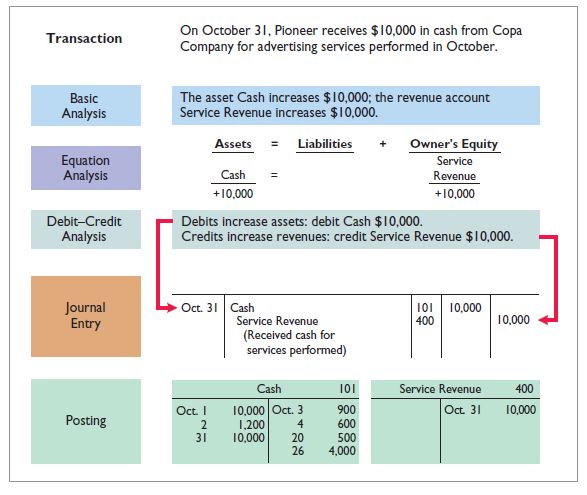

Each transaction requires an analysis. This analysis will determine the type of accounts involved and whether it is a debit or credit. The next illustrations will show how to put the analysis into action. Then we will see the transactions summarized in the general journal and the general ledger.

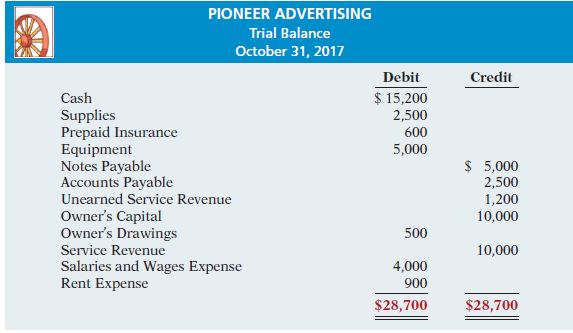

THE TRIAL BALANCE

At any given time, a list of accounts and their balance is called a trial balance. This document is usually prepaid at the end of an accounting period. It proves the equality that "debits equal credits". It is also used when preparing financial statements. Errors can be detected with the trial balance. The accounts are listed in the order of the general ledger; assets, liabilities, owner's equity, revenues and expenses.

The trial balance does not guarentee that the accounts are error free. It may continue to balance even when there are errors within the general ledger. Dollar signs do not appear in the journals and ledgers. They are used typically in the trial balance and financial statements. They are placed with the first item in each column and the total. A singled ruled underline is placed under the column of numbers to be calculated. Once calculated, A double ruled underline is placed under the total. The double ruled underline represents a final total.

Última modificación: martes, 28 de mayo de 2019, 12:05