Reading: Lesson 6 - The ledger

A ledger (general ledger) is the complete collection of all the accounts of a company. The ledger

may be in loose-leaf form, in a bound volume, or in computer memory.

Accounts fall into two general groups: (1) balance sheet accounts (assets, liabilities, and

stockholders' equity) and (2) income statement accounts (revenues and expenses). The terms real

accounts and permanent accounts also refer to balance sheet accounts. Balance sheet accounts are real

accounts because they are not subclassifications or subdivisions of any other account. They are

permanent accounts because their balances are not transferred (or closed) to any other account at

the end of the accounting period. Income statement accounts and the Dividends account are nominal

accounts because they are merely subclassifications of the stockholders' equity accounts. Nominal

literally means "in name only". Nominal accounts are also called temporary accounts because they temporarily contain revenue, expense, and dividend information that is transferred (or closed) to the

Retained Earnings account at the end of the accounting period.

The chart of accounts is a complete listing of the titles and numbers of all the accounts in the

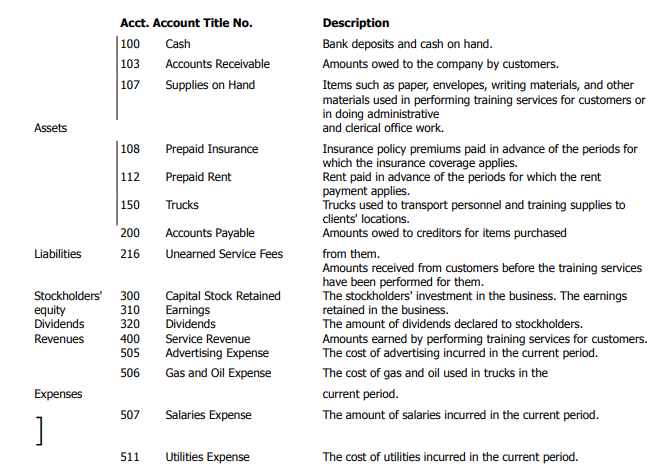

ledger. The chart of accounts can be compared to a table of contents. The groups of accounts usually

appear in this order: assets, liabilities, stockholders' equity, dividends, revenues, and expenses.

Individual accounts are in sequence in the ledger. Each account typically has an identification

number and a title to help locate accounts when recording data. For example, a company might

number asset accounts, 100-199; liability accounts, 200-299; stockholders' equity accounts and

Dividends account, 300-399; revenue accounts, 400-499; and expense accounts, 500-599. We use this

numbering system in this text. The uniform chart of accounts used in the first 11 chapters appears in a

separate file at the end of the text. You should print that file and keep it handy for working certain

problems and exercises. Companies may use other numbering systems. For instance, sometimes a

company numbers its accounts in sequence starting with 1, 2, and so on. The important idea is that

companies use some numbering system.

Now that you understand how to record debits and credits in an account and how all accounts

together form a ledger, you are ready to study the accounting process in operation.

The accounting process in operation

MicroTrain Company is a small corporation that provides on-site personal computer software

training using the clients' equipment. The company offers beginning through advanced training with

convenient scheduling. A small fleet of trucks transports personnel and teaching supplies to the clients'

sites. The company rents a building and is responsible for paying the utilities.

We illustrate the capital stock transaction that occurred to form the company (in November) and

the first month of operations (December). The accounting process used by this company is similar to

that of any small company. The ledger accounts used by MicroTrain Company are:

To begin, a transaction must be journalized. Journalizing is the process of entering the effects of a

transaction in a journal. Then, the information is transferred, or posted, to the proper accounts in the

ledger. Posting is the process of recording in the ledger accounts the information contained in the

journal. In the following example, notice that each business transaction affects two or more accounts in the

ledger. Also note that the transaction date in both the general journal and the general ledger accounts

is the same. In the ledger accounts, the date used is the date that the transaction was recorded in the

general journal, even if the entry is not posted until several days later. Our example shows the journal

entries posted to T-accounts. In practice, firms post journal entries to ledger accounts. Accountants use the accrual basis of accounting. Under the accrual basis of accounting, they

recognize revenues when the company makes a sale or performs a service, regardless of when the

company receives the cash. They recognize expenses as incurred, whether or not the company has paid

out cash. In the following MicroTrain Company example, transaction 1 increases (debits) Cash and increases

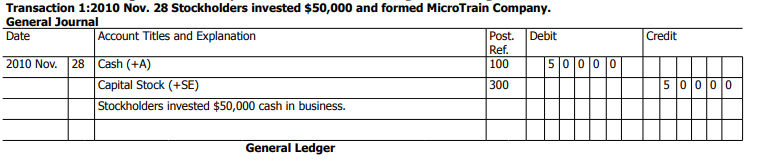

(credits) Capital Stock by USD 50,000. First, MicroTrain records the transaction in the general

journal; second, it posts the entry to the accounts in the general ledger. No other transactions occurred in November. The company prepares financial statements at the

end of each month. Exhibit 9 shows the company's balance sheet at 2010 November 30.

The balance sheet reflects ledger account balances as of the close of business on 2010 November 30.

These closing balances are the beginning balances on 2010 December 1. The ledger accounts show

these closing balances as beginning balances (Beg. bal.).

Now assume that in December 2010, MicroTrain Company engaged in the following transactions.

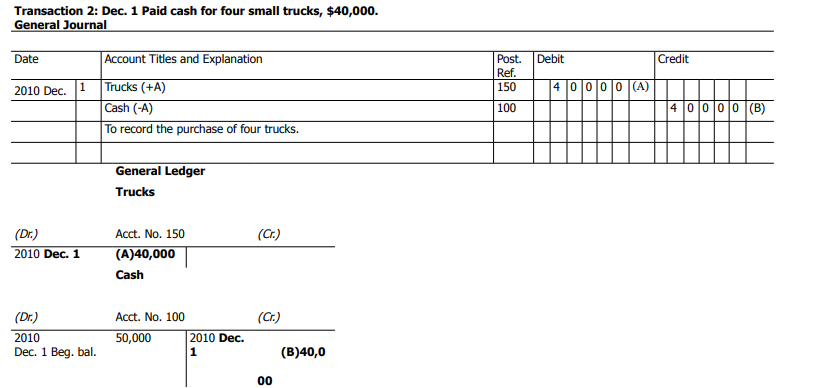

We show the proper recording of each transaction in the journal and then in the ledger accounts (in Taccount

form), and describe the effects of each transaction. Exhibit 9: Balance sheet Effects of transaction An asset, prepaid insurance, increases (debited); and an asset, cash, decreases (credited) by USD

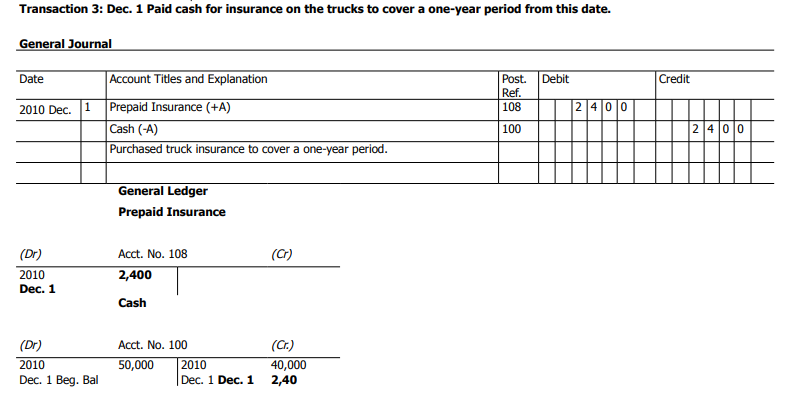

2,400. The debit is to Prepaid Insurance rather than Insurance Expense because the policy covers

more than the current accounting period of December (insurance policies are usually paid one year in

advance). As you will see in Chapter 3, prepaid items are expensed as they are used. If this insurance policy was only written for December, the entire USD 2,400 debit would have been to Insurance

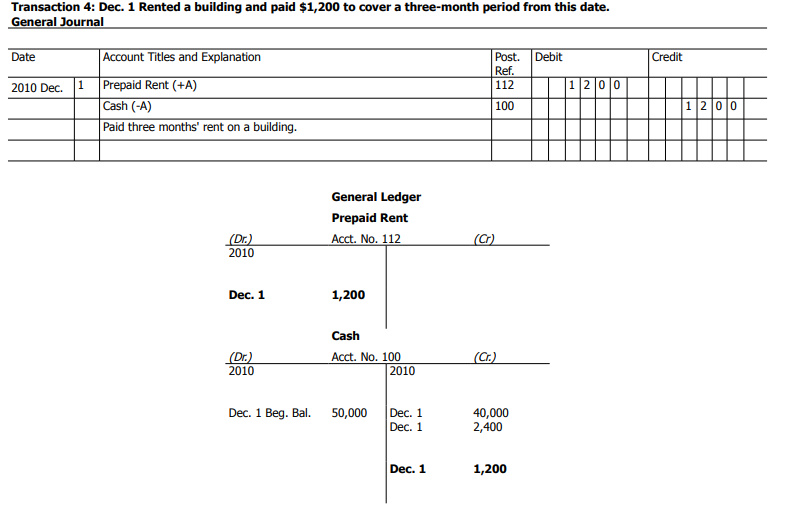

Expense. An asset, prepaid rent, increases (debited); and another asset, cash, decreases (credited) by USD

1,200. The debit is to Prepaid Rent rather than Rent Expense because the payment covers more than

the current month. If the payment had just been for December, the debit would have been to Rent

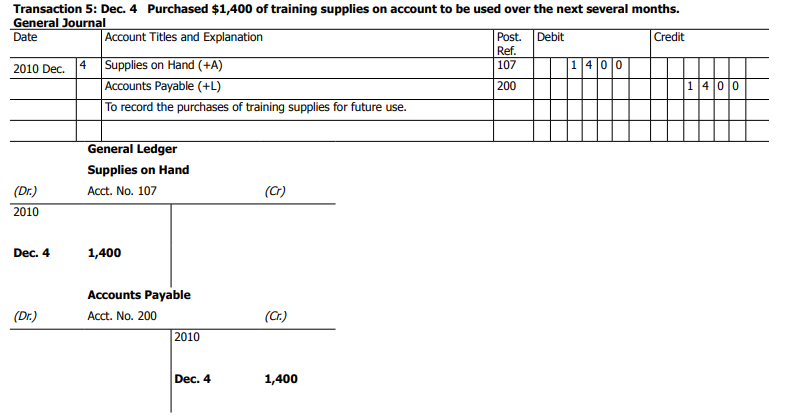

Expense. Effects of transaction An asset, supplies on hand, increases (debited); and a liability, accounts payable, increases

(credited) by USD 1,400. The debit is to Supplies on Hand rather than Supplies Expense because the

supplies are to be used over several accounting periods.

In each of the three preceding entries, we debited an asset rather than an expense. The reason is

that the expenditure applies to (or benefits) more than just the current accounting period. Whenever a

company will not fully use up an item such as insurance, rent, or supplies in the period when

purchased, it usually debits an asset. In practice, however, sometimes the expense is initially debited in

these situations. Companies sometimes buy items that they fully use up within the current accounting period. For

example, during the first part of the month a company may buy supplies that it intends to consume

fully during that month. If the company fully consumes the supplies during the period of purchase, the

best practice is to debit Supplies Expense at the time of purchase rather than Supplies on Hand. This

same advice applies to insurance and rent. If a company purchases insurance that it fully consumes

during the current period, the company should debit Insurance Expense at the time of purchase rather

than Prepaid Insurance. Also, if a company pays rent that applies only to the current period, Rent

Expense should be debited at the time of purchase rather than Prepaid Rent.

Notice the gaps left between account numbers (100, 103, 107, etc.). These gaps allow the firm to

later add new accounts between the existing accounts.

Effects of transaction

Effects of transaction

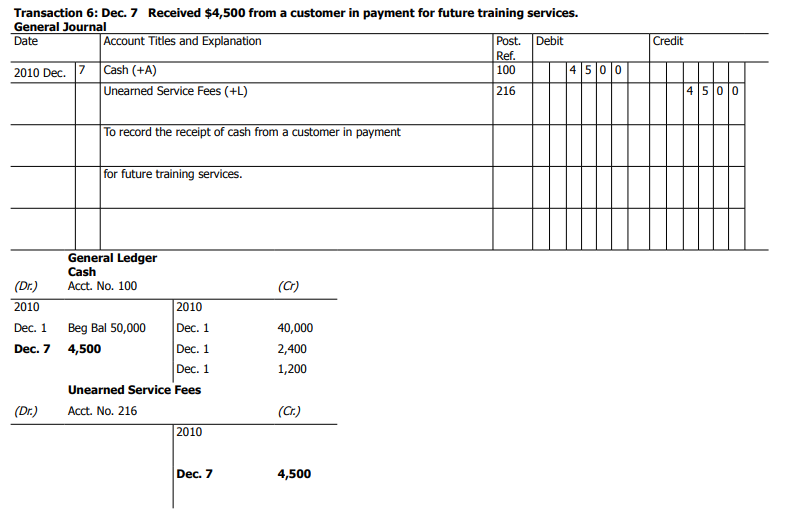

An asset, cash, increases (debited); and a liability, unearned service revenue, increases (credited) by

USD 4,500. The credit is to Unearned Service Fees rather than Service Revenue because the USD

4,500 applies to more than just the current accounting period. Unearned Service Fees is a liability

because, if the services are never performed, the USD 4,500 will have to be refunded. If the payment

had been for services to be provided in December, the credit would have been to Service Revenue.

Effects of transaction

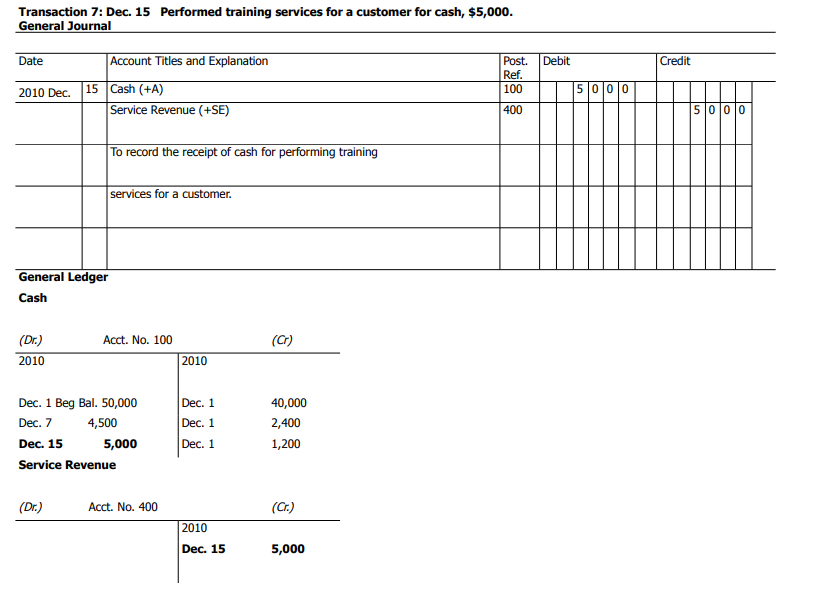

An asset, cash, increases (debited); and a revenue, service revenue, increases (credited) by USD

5,000.

Effects of transaction

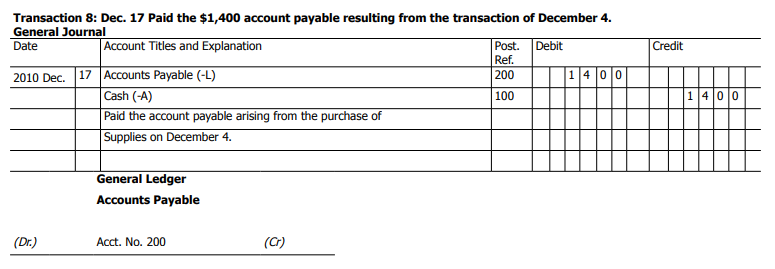

A liability, accounts payable, decreases (debited); and an asset, cash, decreases (credited) by USD

1,400.

Effects of transaction

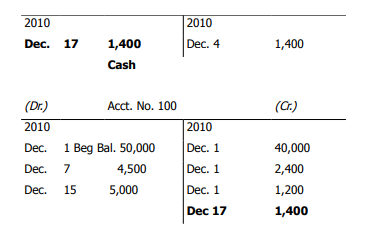

An asset, accounts receivable, increases (debited); and a revenue, service revenue, increases

(credited) by USD 5,700.

Effects of transaction

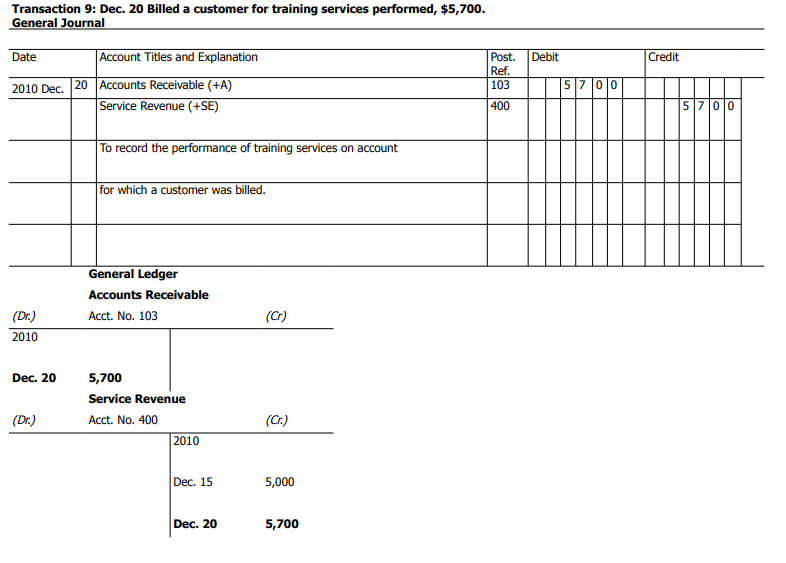

An expense, advertising expense, increases (debited); and a liability, accounts payable, increases (credited) by USD 50. The reason for debiting an expense rather than an asset is because all the cost pertains to the current accounting period, the month of December. Otherwise, Prepaid Advertising (an asset) would have been debited.

Effects of transaction

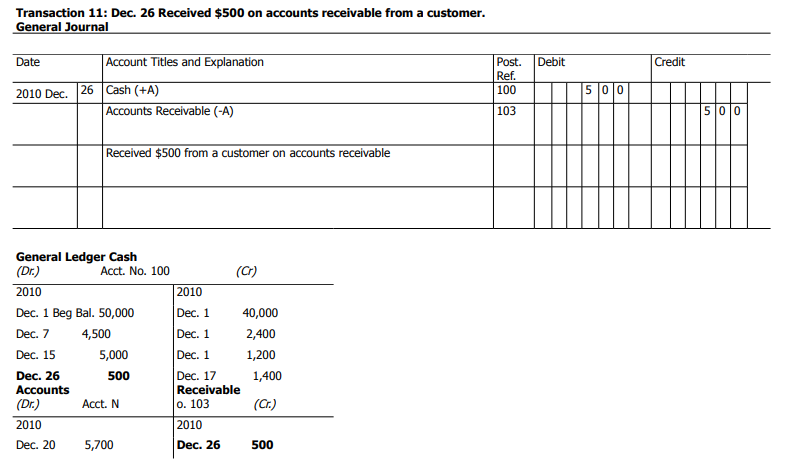

One asset, cash, increases (debited); and another asset, accounts receivable, decreases (credited) by

USD 500.

Effects of transaction

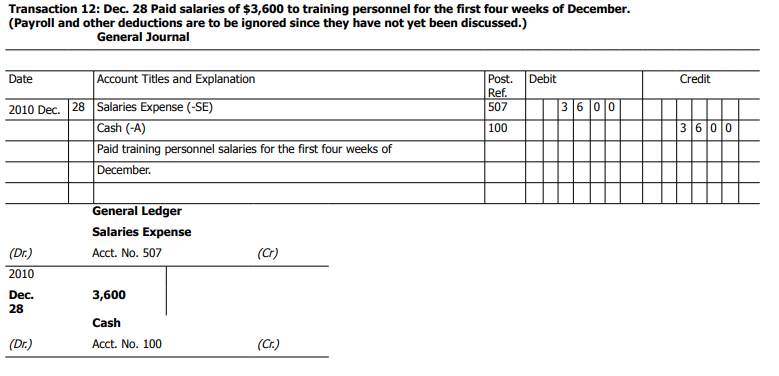

An expense, salaries expense, increases (debited); and an asset, cash, decreases (credited) by USD

3,600.

Effects of transaction

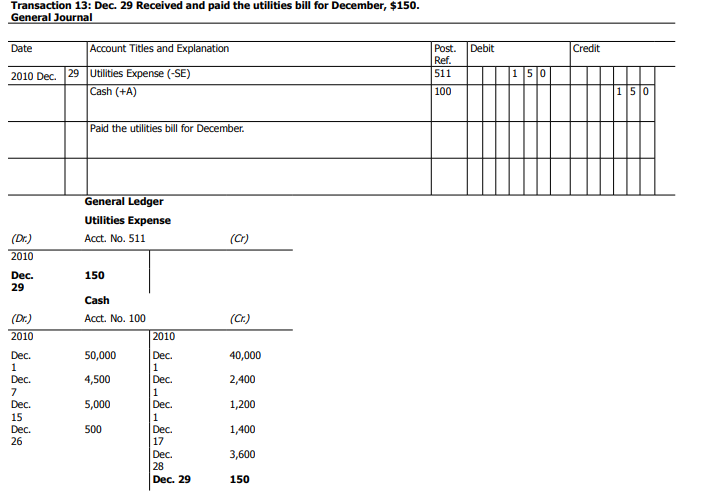

An expense, utilities expense, increases (debited); and an asset, cash, decreases (credited) by USD

150.

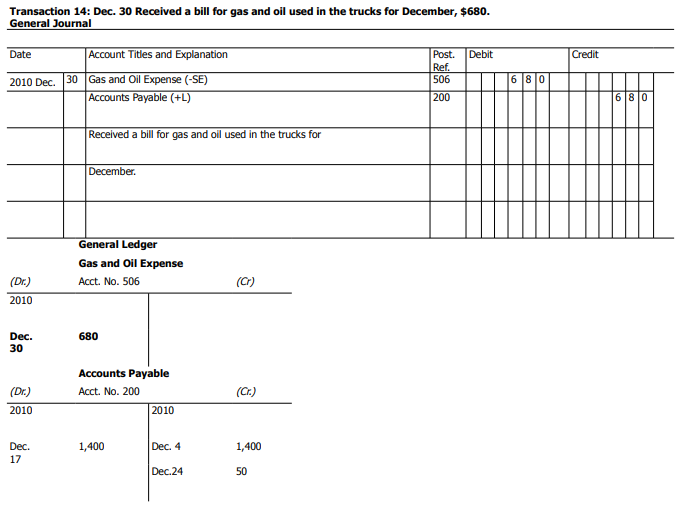

Effects of transaction

An expense, gas and oil expense, increases (debited); and a liability, accounts payable, increases

(credited) by USD 680.

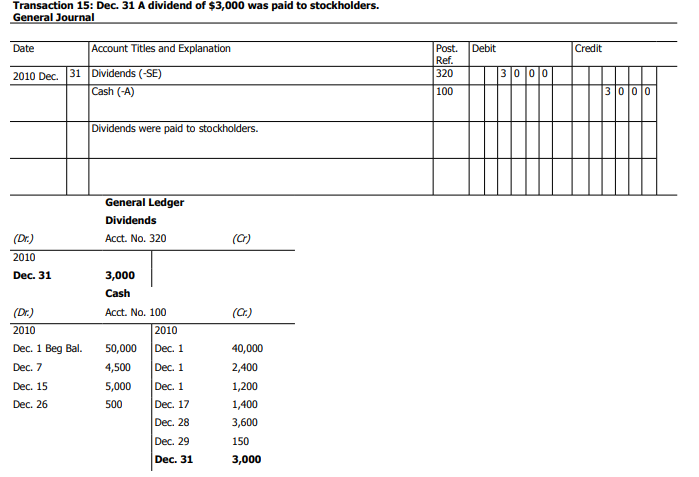

Effects of transaction

The Dividends account increases (debited); and an asset, cash, decreases (credited) by USD 3,000. Transaction 15 concludes the analysis of the MicroTrain Company transactions. The next section discusses and illustrates posting to ledger accounts and cross-indexing.

Modifié le: mardi 28 mai 2019, 12:09