Reading: Lesson 5 - Subsequent expenditures (capital and revenue) on assets

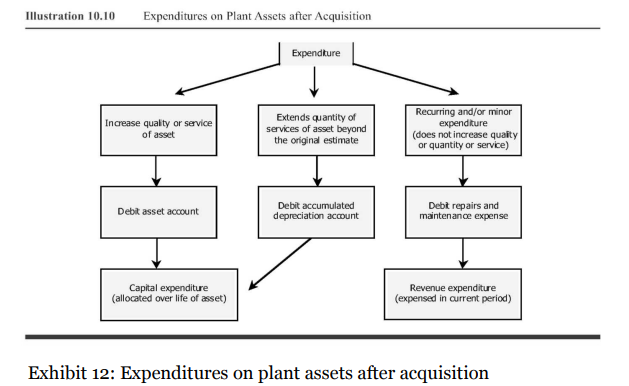

Companies often spend additional funds on plant assets that have been in use for

some time. They debit these expenditures to: (1) an asset account; (2) an accumulated

depreciation account; or (3) an expense account.

Expenditures debited to an asset account or to an accumulated depreciation account

are capital expenditures. Capital expenditures increase the book value of plant

assets. Revenue expenditures, on the other hand, do not qualify as capital

expenditures because they help to generate the current period's revenues rather than

future periods' revenues. As a result, companies expense these revenue expenditures

immediately and report them in the income statement as expenses.

Betterments or improvements to existing plant assets are capital expenditures

because they increase the quality of services obtained from the asset. Because

betterments or improvements add to the service-rendering ability of assets, firms

charge them to the asset accounts. For example, installing an air conditioner in an

automobile that did not previously have one is a betterment. The debit for such an

expenditure is to the asset account, Automobiles.

Occasionally, expenditures made on plant assets extend the quantity of services

beyond the original estimate but do not improve the quality of the services. Since these

expenditures benefit an increased number of future periods, accountants capitalize

rather than expense them. However, since there is no visible, tangible addition to, or

improvement in, the quality of services, they charge the expenditures to the

accumulated depreciation account, thus reducing the credit balance in that account.

Such expenditures cancel a part of the existing accumulated depreciation; firms often

call them extraordinary repairs.

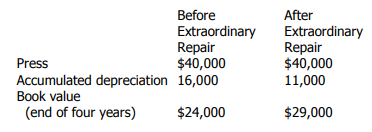

To illustrate, assume that after operating a press for four years, a company spent

USD 5,000 to recondition the press. The reconditioning increased the machine's life to 14 years instead of the original estimate of 10 years. The journal entry to record the

extraordinary repair is:

Originally, the press cost USD 40,000, had an estimated useful life of 10 years, and

had no estimated salvage value. At the end of the fourth year, the balance in its

accumulated depreciation account under the straight-line method is [(USD 40,000/10)

X 4] = USD 16,000. After debiting the USD 5,000 spent to recondition the press to the

accumulated depreciation account, the balances in the asset account and its related

accumulated depreciation account are as shown in the last column:

In effect, the expenditure increases the carrying amount (book value) of the asset by

reducing its contra account, accumulated depreciation. Under the straight-line

method, we would divide the new book value of the press, USD 29,000, equally among

the 10 remaining years in amounts of USD 2,900 per year (assuming that the estimated

salvage value is still zero).

As a practical matter, expenditures for major repairs not extending the asset's life

are sometimes charged to accumulated depreciation. This avoids distorting net income

by expensing these expenditures in the year incurred. Then, firms calculate a revised

depreciation expense, and spread the cost of major repairs over a number of years. This

treatment is not theoretically correct.

To illustrate, assume the same facts as in the previous example except that the USD

5,000 expenditure did not extend the life of the asset. Because of the size of this

expenditure, the company still charges it to accumulated depreciation. Now, it would

spread the USD 29,000 remaining book value over the remaining six years of the life of

the press. Under the straight-line method, annual depreciation would then be (USD

29,000/6) = USD 4,833.

Accountants treat as expenses those recurring and/or minor expenditures that

neither add to the asset's service-rendering quality nor extend its quantity of services

beyond its original estimated useful life. Thus, firms immediately expense regular

maintenance (lubricating a machine) and ordinary repairs (replacing a broken fan belt

on an automobile) as revenue expenditures. For example, a company that spends USD

190 to repair a machine after using it for some time, debits Maintenance Expense or

Repairs Expense.

Low-cost items Most businesses purchase low-cost items that provide years of

service, such as paperweights, hammers, wrenches, and drills. Because of the small

dollar amounts involved, it is impractical to use the ordinary depreciation methods for

such assets, and it is often costly to maintain records of individual items. Also, the

effect of low-cost items on the financial statements is not significant. Accordingly, it is

more efficient to record the items as expenses when they are purchased. For instance,

many companies charge any expenditure less than an arbitrary minimum, say, USD

100, to expense regardless of its impact on the asset's useful life. This practice of

accounting for such low unit cost items as expenses is an example of the modifying

convention of materiality that was discussed in Chapter 5. In Exhibit 12, we summarize

expenditures on plant assets after acquisition.

In practice, it is difficult to decide whether to debit an expenditure to the asset

account or to the accumulated depreciation account. For example, some expenditures

seem to affect both the quality and quantity of services. Even if the wrong account were

debited for the expenditure, the book value of the plant asset at that point would be the

same amount it would have been if the correct account had been debited. However,

both the asset and accumulated depreciation accounts would be misstated.

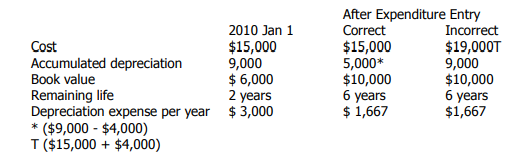

As an example of the effect of misstated asset and accumulated depreciation

accounts, assume Watson Company had an asset that had originally cost USD 15,000

and had been depreciated to a book value of USD 6,000 at the beginning of 2010. At

that time, Watson estimated the equipment had a remaining useful life of two years.

The company spent USD 4,000 in early January 2010 to install a new motor in the

equipment. This motor extended the useful life of the asset four years beyond the

original estimate. Since the expenditure extended the life, the firm should capitalize it

by a debit to the accumulated depreciation account. We show the calculations for

depreciation expense if the entry was made correctly and if the expenditure had been

improperly charged (debited) to the asset account in Exhibit 13.

If an expenditure that should be expensed is capitalized, the effects are more

significant. Assume now that USD 6,000 in repairs expense is incurred for a plant asset

that originally cost USD 40,000 and had a useful life of four years and no estimated

salvage value. This asset had been depreciated using the straight-line method for one

year and had a book value of USD 30,000 (USD 40,000 cost—USD 10,000 first-year

depreciation) at the beginning of 2010. The company capitalized the USD 6,000 that

should have been charged to repairs expense in 2010. The charge for depreciation

should have remained at USD 10,000 for each of the next three years. With the

incorrect entry, however, depreciation increases.

Regardless of whether the repair was debited to the asset account or the

accumulated depreciation account, the firm would change the depreciation expense

amount to USD 12,000 for each of the next three years [(USD 30,000 book value +

USD 6,000 repairs expense)/3 more years of useful life]. These errors would cause net

income for the year 2010 to be overstated USD 4,000: (1) repairs expense is

understated by USD 6,000, causing income to be overstated by USD 6,000; and (2)

depreciation expense is overstated by USD 2,000, causing income to be understated by

USD 2,000. In 2011, the overstatement of depreciation by USD 2,000 would cause 2011

income to be understated by USD 2,000.

Note that the USD 6,000 recording error affects more than just the expense

accounts and net income. Plant asset and Retained Earnings accounts on the balance

sheet also reflect the impact of this error. To see the effect of incorrectly capitalizing

the USD 6,000 to the asset account rather than correctly expensing it, look at Exhibit

14.

Última modificación: martes, 28 de mayo de 2019, 12:14