Reading: Lesson 6 - Subsidiary records used to control plant assets

Most companies maintain formal records (ranging from handwritten documents to

computer tapes) to ensure control over their plant assets. These records include an

asset account and a related accumulated depreciation account in the general ledger for

each major class of depreciable plant assets, such as buildings, factory machinery,

office equipment, delivery equipment, and store equipment.

Because the general ledger account has no room for detailed information about each

item in a major class of depreciable plant assets, many companies use plant asset

subsidiary ledgers. Subsidiary ledgers for Accounts Receivable and Accounts Payable

were explained briefly in An accounting perspective in Chapter 4. A company may

also use subsidiary ledgers for plant assets. For instance, assume a company has a

general ledger account for office furniture. The subsidiary ledger for office furniture

might contain four separate accounts entitled: Desks, Chairs, File Cabinets and

Bookshelves. Alternatively, a company could even have a separate subsidiary account

for each piece of furniture. The total of all the subsidiary account balances must equal

the total of the general ledger "control" account for Office Furniture at the end of the

accounting period. Each general ledger account for each class of depreciable asset, such as Buildings, Delivery Equipment, and so on, could have a subsidiary ledger backing it

up and showing information such as the description, cost, and purchase date for each

asset. These subsidiary ledgers and detailed records provide more information and

allow the company to maintain better control over plant and equipment.

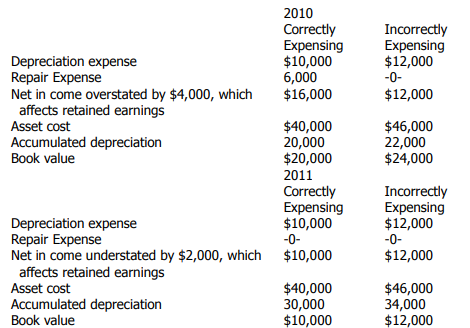

Exhibit 14: Effect of revenue expenditure treated as capital expenditure

When they are kept for each major class of plant and equipment, a company may

have subsidiary ledgers for factory machinery, office equipment, and other classes of

depreciable plant assets. Then there may be an additional subsidiary ledger for each

type of asset within each category. For example, the subsidiary office equipment ledger

may contain accounts for microcomputers, printers, fax machines, copying machines,

and so on. Companies also keep a detailed record for each item represented in a

subsidiary ledger account. For example, there may be a separate detailed record for

each microcomputer represented in the Microcomputer subsidiary ledger account.

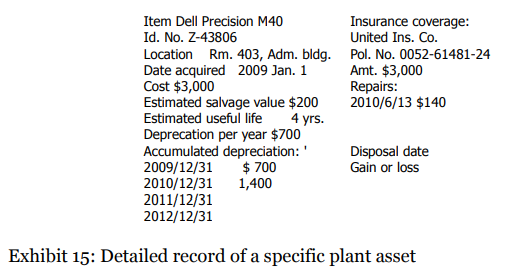

Each detailed record should include a description of the asset, identification or serial

number, location of the asset, date of acquisition, cost, estimated salvage value,

estimated useful life, annual depreciation, accumulated depreciation, insurance

coverage, repairs, date of disposal, and gain or loss on final disposal of the asset. Note

the detailed record for one particular microcomputer as of 2010 December 31, in

Exhibit 15.

To enhance control over plant and equipment, companies stencil on or attach the

identification or serial number to each asset. Periodically, firms must take a physical inventory to determine whether all items in the accounting records actually exist,

whether they are located where they should be, and whether they are still being used. A

company that does not use detailed records and identification numbers or take

physical inventories finds it difficult to determine whether assets have been discarded

or stolen.

The general ledger control account balance for each major class of plant and

equipment should equal the total of the amounts in the subsidiary ledger accounts for

that class of plant assets. Also, the totals in the detailed records for a specific subsidiary

ledger account (such as Microcomputers) should equal the balance of that account.

Each time a plant asset is acquired, exchanged, or disposed of, the firm posts an entry

to both a general ledger control account and the appropriate subsidiary ledger account.

It also updates the detailed record for the items affected.

最后修改: 2019年05月28日 星期二 12:14