Reading: Lesson 1 - Financial Statements & Reports

2.1.A - Financial Statements & Reports

1. Financial Statements & Reports

- A company’s annual report usually begins with the chairperson’s description of the firm’s operating results during the past year and a discussion of new developments that will affect future operations. The annual report also presents four basic financial statements— the balance sheet, the income statement, the statement of stockholders’ equity, and the statement of cash flows.

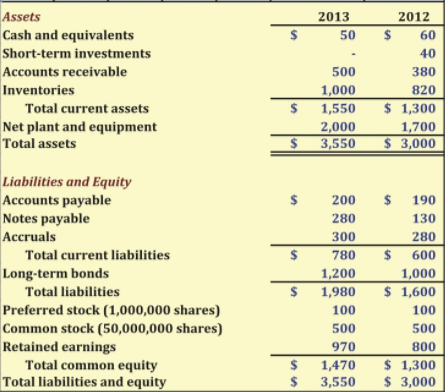

2. The Balance Sheet

- A balance sheets, represents a "snapshot” of its financial position on the last day of each year. Although most companies report their balance sheets only on the last day of a given period, the “snapshot” actually changes daily as inventories are bought and sold, as fixed assets are added or retired, or as loan balances are increased or paid down.

- The balance sheet begins with assets, which are the “things” the company owns. Assets are listed in order of “liquidity,” or length of time it typically takes to convert them to cash at fair market values. The balance sheet also lists the claims that various groups have against the company’s value; these are listed in the order in which they must be paid. For example, suppliers may have claims called “accounts payable” that are due within 30 days, banks may have claims called “notes payable” that are due within 90 days, and bond-holders may have claims that are not due for 20 years or more.

- Stockholders’ claims represent ownership (or equity) and need never be “paid off.” These are residual claims in the sense that stockholders may receive payments only if there is value remaining after other claimants have been paid. The non-stockholder claims are liabilities from the stockholders’ perspective. The amounts shown on the balance sheets are called book values because they are based on the amounts recorded by book-keepers when assets are purchased or liabilities are issued. As you will see throughout this textbook, book values may be very different from market values, which are the current values as determined in the marketplace.

3. Assets

- Cash, short-term investments, accounts receivable, and inventories are listed as current assets. Some marketable securities mature very soon, and these can be converted quickly into cash at prices close to their book values. Such securities are called “cash equivalents” and are included with cash. These securities are classified as “short-term investments.”

- Inventories show the dollars invested in raw materials, work-in-process, and finished goods available for sale. Firm can use the FIFO (first-in, first-out) method to determine the inventory value shown on its balance sheet ($1 billion). It could have used the LIFO (last-in, first-out) method. During a period of rising prices, by taking out old, low-cost inventory and leaving in new, high-cost items, FIFO will produce a higher balance sheet inventory value but a lower cost of goods sold on the income statement. (FIFO is used strictly for accounting purposes; companies actually use older items first.) Firms will use FIFO because inflation may occur: (1) its balance sheet inventories are higher than they would have been had it used LIFO, (2) its cost of goods sold is lower than it would have been under LIFO, and (3) its reported profits are therefore higher.

- Rather than treat the entire purchase price of a long-term asset (such as a factory, plant, or equipment) as an expense in the purchase year, accountants “spread” the purchase cost over the asset’s useful life.1 The amount they charge each year is called the depreciation expense. Some companies report an amount called “gross plant and equipment,” which is the total cost of the long-term assets they have in place, and another amount called “accumulated depreciation,” which is the total amount of depreciation that has been charged on those assets. Some companies report only net plant and equipment, which is gross plant and equipment less accumulated depreciation.

4. Liabilities and Equity

- Accounts payable, notes payable, and accruals are listed as current liabilities because these are expected to paid within a year. When firms purchase supplies they do not immediately pay for them, it takes on an obligation called an account payable. Similarly, when a firm takes out a loan that must be repaid within a year, it signs an IOU called a note payable. Firms do not pay its taxes or its employees’ wages daily, and the amount it owes on these items at any point in time is called an “accrual” or an “accrued expense.” Long-term bonds are also liabilities because they, too, reflect a claim held by someone other than a stockholder.

- Preferred stock is a hybrid, or a cross between common stock and debt. In the event of bankruptcy, preferred stock ranks below debt but above common stock. Also, the preferred dividend is fixed, so preferred stockholders do not benefit if the company’s earnings grow. Most firms do not use much, if any, preferred stock, so “equity” usually means “common equity” unless the words “total” or “preferred” are included.

- When a company sells shares of stock, it records the proceeds in the common stock account.2 Retained earnings are the cumulative amount of earnings that have not been paid out as dividends. The sum of common stock and retained earnings is called “common equity,” or just “equity.” If a company could actually sell its assets at their book value, and if the liabilities and preferred stock were actually worth their book values, then a company could sell its assets, pay off its liabilities and preferred stock, and the remaining cash would belong to common stockholders. Therefore, common equity is sometimes called net worth—it’s the assets minus (or “net of”) the liabilities.

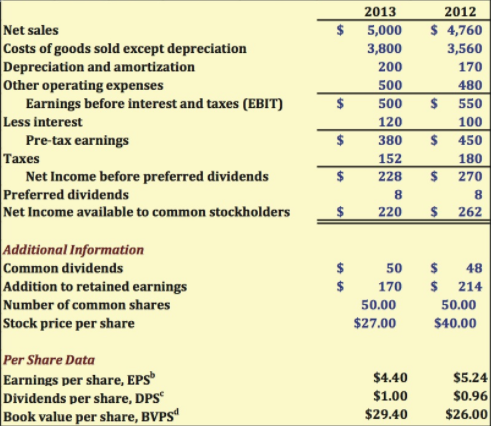

5. The Income Statement

- Income statements can cover any period of time, but they are usually prepared monthly, quarterly, and annually. Unlike the balance sheet, which is a snapshot of a firm at a resource point in time, the income statement reflects performance during the period.

- Net sales are the revenues less any discounts or returns. Depreciation and amortization reflect the estimated costs of the assets that wear out in producing goods and services. To illustrate depreciation, suppose that in 2010 a firm purchased a $100,000 machine with a life of 5 years and zero expected salvage value. This $100,000 cost is not expensed in the purchase year but is instead spread out over the machine’s 5-year depreciable life. In straight-line depreciation, which we explain in Chapter 11, the depreciation charge for a full year would be $100,000/5 = $20,000. The reported depreciation expense on the income statement is the sum of all the assets’ annual depreciation charges. Depreciation applies to tangible assets, such as plant and equipment, whereas amortization applies to intangible assets such as patents, copyrights, trademarks, and goodwill.

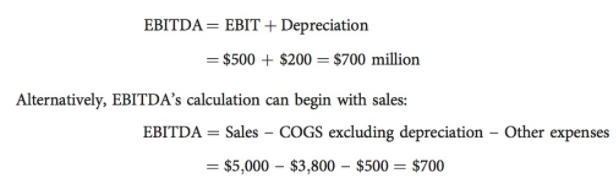

- The cost of goods sold (COGS) includes labor, raw materials, and other expenses directly related to the production or purchase of the items or services sold in that period. The COGS includes depreciation, but we report depreciation separately so that analysis later in the chapter will be more transparent. Subtracting COGS (including depreciation) and other operating expenses results in earnings before interest and taxes (EBIT). Many analysts add back depreciation to EBIT to calculate EBITDA, which stands for earnings before interest, taxes, depreciation, and amortization. Because neither depreciation nor amortization is paid in cash, some analysts claim that EBITDA is a better measure of financial strength than is net income.

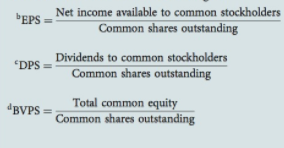

- EBITDA is not as useful to managers and analysts as free cash flow, so we usually focus on free cash flow instead of EBITDA. The net income available to common shareholders, which equals revenues less expenses, taxes, and preferred dividends (but before paying common dividends), is generally referred to as net income. Net income is also called accounting profit, profit, or earnings, particularly in financial news reports. Dividing net income by the number of shares outstanding gives earnings per share (EPS), often called “the bottom line.” Throughout this book, unless otherwise indicated, net income means net income available to common stockholders.

Última modificación: martes, 14 de agosto de 2018, 08:38