Reading: Lesson 2 - Statement of Shareholders Equity & Statement of Cash Flows

2.2.A - Statement of Shareholder's Equity and Statement of Cash Flows

1. Statement of Shareholder's Equity

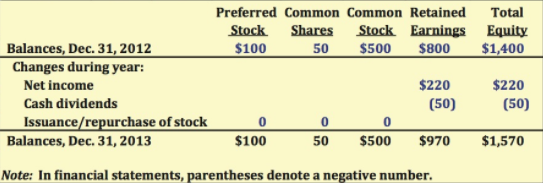

- Changes in stockholders’ equity during the accounting period are reported in the statement of stockholders’ equity.

- A firm earned $220 million during 2013, paid out $50 million in common dividends, and plowed $150 million back into the business.

- The balance sheet item “Retained earnings” increased from $800 million at year-end 2012 to $970 million at year-end 2013.

- Note that “retained earnings” does not represent assets but is instead a claim against assets. In 2013, a firm's stockholders allowed it to reinvest $170 million instead of distributing the money as dividends, and management spent this money on new assets.

- Retained earnings, as reported on the balance sheet, does not represent cash and is not “available” for the payment of dividends or anything else.

2. Statement of Cash Flows

- Even if a company reports a large net income during a year, the amount of cash reported on its year-end balance sheet may be the same or even lower than its beginning cash. The reason is that the company can use its net income in a variety of ways, not just keep it as cash in the bank.

- For example, the firm may use its net income to pay dividends, to increase inventories, to finance accounts receivable, to invest in fixed assets, to reduce debt, or to buy back common stock. Indeed, many factors affect a company’s cash position as reported on its balance sheet.

- The statement of cash flows separates a company’s activities into three categories—operating, investing, and financing— and summarizes the resulting cash balance.

3. Operating Activities

- As the name implies, the section for operating activities focuses on the amount of cash generated (or lost) by the firm’s operating activities.

- Noncash Adjustments: Some revenues and expenses reported on the income statement are not received or paid in cash during the year. For example, depreciation and amortization reduce reported net income but are not cash payments. Reported taxes often differ from the taxes that are paid, resulting in an account called deferred taxes, which is the cumulative difference between the taxes that are reported and those that are paid. Deferred taxes can occur in many ways, including the use of accelerated depreciation for tax purposes but straight-line depreciation for financial reporting. This increases reported taxes relative to actual tax payments in the early years of an asset’s life, causing the resulting net income to be lower than the true cash flow. Therefore, increases in deferred taxes are added to net income when calculating cash flow, and decreases are subtracted from net income. Another example of noncash reporting occurs if a customer purchases services or products that extend beyond the reporting date, such as a 3-year extended warranty for a computer. Even if the company collects the cash at the time of the purchase, it will spread the reported revenues over the life of the purchase. This causes income to be lower than cash flow in the first year and higher in subsequent years, so adjustments must be made when calculating cash flow.

- Changes in Working Capital: Increases in current assets other than cash (such as inventories and accounts receivable) decrease cash, whereas decreases in these accounts increase cash. For example, if inventories are to increase, then the firm must use cash to acquire the additional inventory. Conversely, if inventories decrease, this generally means the firm is selling inventories and not replacing all of them, hence generating cash. Here’s how we keep track of whether a change in assets increases or decreases cash flow: If the amount we own goes up (like getting a new laptop computer), it means we have spent money and our cash goes down. On the other hand, if something we own goes down (like selling a car), our cash goes up. Now consider a current liability, such as accounts payable. If accounts payable increase then the firm has received additional credit from its suppliers, which saves cash; but if payables decrease, this means it has used cash to pay off its suppliers. Therefore, increases in current liabilities such as accounts payable increase cash, whereas decreases in current liabilities decrease cash. To keep track of the cash flow’s direction, think about the impact of getting a student loan. The amount you owe goes up and your cash goes up. Now think about paying off the loan: The amount you owe goes down, but so does your cash.

4. Investing Activities

- Investing activities include transactions involving fixed assets or short-term financial investments. For example, if a company buys new IT infrastructure, its cash goes down at the time of the purchase. On the other hand, if it sells a building or T-bill, its cash goes up.

5. Financing Activities

- Financing activities include raising cash by issuing short-term debt, long-term debt, or stock. Because dividend payments, stock repurchases, and principal payments on debt reduce a company’s cash, such transactions are included here.

6. Putting the Pieces Together

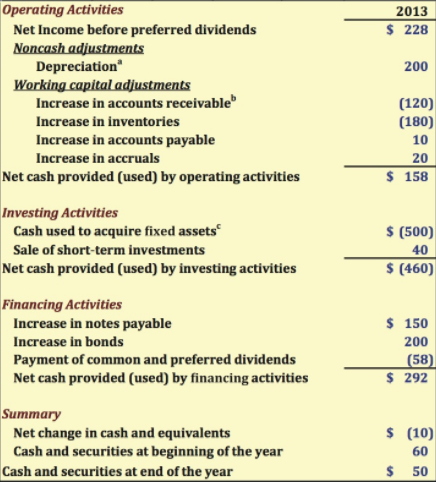

- The statement of cash flows is used to help answer questions such as these: Is the firm generating enough cash to purchase the additional assets required for growth? Is the firm generating any extra cash it can use to repay debt or to invest in new products? Such information is useful both for managers and investors, so the statement of cash flows is an important part of the annual report. This firm’s statement of cash flows as it would appear in the company’s annual report. The top section shows cash generated by and used in operations—for this firm, operations provided net cash flows of $158 million. This subtotal is in many respects the most important figure in any of the financial statements. Profits as reported on the income statement can be “doctored” by such tactics as depreciating assets too slowly, not recognizing bad debts promptly, and the like. However, it is far more difficult to simultaneously doctor profits and the working capital accounts. Therefore, it is not uncommon for a company to report positive net income right up to the day it declares bankruptcy. In such cases, however, the net cash flow from operations almost always began to deteriorate much earlier, and analysts who kept an eye on cash flow could have predicted trouble. Therefore, if you are ever analyzing a company and are pressed for time, look first at the trend in net cash flow provided by operating activities, because it will tell you more than any other single number. The second section shows investing activities. The firm purchased fixed assets totaling $500 million and sold $40 million of short-term investments, for a net cash flow from investing activities of minus $460 million. The third section, financing activities, includes borrowing from banks (notes payable), selling new bonds, and paying dividends on common and preferred stock. The firm raised $350 million by borrowing, but it paid $58 million in preferred and common dividends. Therefore, its net inflow of funds from financing activities was $292 million. In the summary, when all of these sources and uses of cash are totaled, we see that the Firm’s cash outflows exceeded its cash inflows by $10 million during 2013; that is, its net change in cash was a negative $10 million. The firm’s statement of cash flows should be worrisome to its managers and to outside analysts. The company had $5 billion in sales but generated only $158 million from operations, not nearly enough to cover the $500 million it spent on fixed assets and the $58 million it paid in dividends. It covered these cash outlays by borrowing heavily and by liquidating short-term investments. Obviously, this situation cannot continue year after year, so the firm's managers will have to make changes.

Última modificación: martes, 14 de agosto de 2018, 08:38