Reading: Lesson 4 - Performance Evaluation

2.4.A - Performance Evaluation

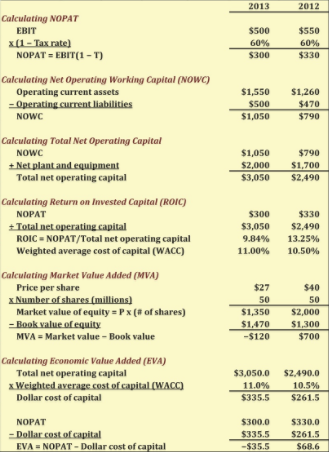

1. The Return on Invested Capital

- There is nothing wrong with value-adding growth, even if it causes negative free cash flows, but it is vital to determine whether growth is actually adding value. For this we use the return on invested capital (ROIC), which shows how much NOPAT is generated by each dollar of operating capital:

2.To determine whether this ROIC is high enough to add value, compare it to the weighted average cost of capital (WACC). Chapter 9 explains how to calculate the WACC; for now accept that the WACC considers a company’s individual risk as well as overall market conditions.

2. Market Value Added

- One measure of shareholder wealth is the difference between the market value of the firm’s stock and the cumulative amount of equity capital that was supplied by shareholders. This difference is called the Market Value Added (MVA):

2. To illustrate, consider Coca-Cola. In February 2012, its total market equity value, commonly called market capitalization, was $157 billion, while its balance sheet showed that stockholders had put up only $32 billion. Thus, Coca-Cola’s MVA was $157 − $32 = $125 billion. This $125 billion represents the difference between the money that Coca-Cola’s stockholders have invested in the corporation since its founding—including indirect investment by retaining earnings—and the cash they could get if they sold the business. The higher its MVA, the better the job management is doing for the firm’s shareholders. Sometimes MVA is defined as the total market value of the company minus the total amount of investor-supplied capital:

3. For most companies, the total amount of investor-supplied capital is the sum of equity, debt, and preferred stock. We can calculate the total amount of investor-supplied capital directly from their reported values in the financial statements. The total market value of a company is the sum of the market values of common equity, debt, and preferred stock. It is easy to find the market value of equity because stock prices are readily available, but it is not always easy to find the market value of debt. Hence, many analysts use the value of debt reported in the financial statements, which is the debt’s book value, as an estimate of the debt’s market value.

4. For Coca-Cola, the total amount of reported debt was about $29 billion; Coca-Cola had no preferred stock. Using the debt’s book value as an estimate of the debt’s market value, Coke’s total market value was $157 + $29 = $186 billion. The total amount of investor-supplied funds was $32 + $29 = $61 billion. Using these total values, the MVA was $186 − $61 = $125 billion. Note that this is the same answer as when we used the previous definition of MVA. Both methods will give the same result if the market value of debt is approximately equal to its book value.

3. Economic Value Added

- Economic Value Added is an estimate of a business’s true economic profit for the year, and it differs sharply from accounting profit.10 EVA represents the residual income that remains after the cost of all capital, including equity capital, has been deducted, whereas accounting profit is determined without imposing a charge for equity capital. As we discuss in Chapter 9, equity capital has a cost because shareholders give up the opportunity to invest and earn returns elsewhere when they provide capital to the firm. This cost is an opportunity cost rather than an accounting cost, but it is real nonetheless.

- Note that when calculating EVA we do not add back depreciation. Although it is not a cash expense, depreciation is a cost because worn-out assets must be replaced, and it is therefore deducted when determining both net income and EVA. Our calculation of EVA assumes that the true economic depreciation of the company’s fixed assets exactly equals the depreciation used for accounting and tax purposes. If this were not the case, adjustments would have to be made to obtain a more accurate measure of EVA.

- Economic Value Added measures the extent to which the firm has increased shareholder value. Therefore, if managers focus on EVA, they will more likely operate in a manner consistent with maximizing shareholder wealth. Note too that EVA can be determined for divisions as well as for the company as a whole, so it provides a useful basis for determining managerial performance at all levels. Consequently, many firms include EVA as a component of compensation plans.

- MVA measures the effects of managerial actions since the inception of a company, Economic Value Added (EVA) focuses on managerial effectiveness in a given year. The EVA formula is:

4. Intrinsic Value, MVA, and EVA

- There is a relationship between MVA and EVA, but it is not a direct one. If a company has a history of negative EVAs, then its MVA will probably be negative; conversely, its MVA probably will be positive if the company has a history of positive EVAs. However, the stock price, which is the key ingredient in the MVA calculation, depends more on expected future performance than on historical performance. Therefore, a company with a history of negative EVAs could have a positive MVA, provided investors expect a turnaround in the future.

- The second observation is that when EVAs or MVAs are used to evaluate managerial performance as part of an incentive compensation program, EVA is the measure that is typically used. The reasons are: (1) EVA shows the value added during a given year, whereas MVA reflects performance over the company’s entire life, perhaps even including times before the current managers were born, and (2) EVA can be applied to individual divisions or other units of a large corporation, whereas MVA must be applied to the entire corporation.

Última modificación: martes, 14 de agosto de 2018, 08:38