Reading: Lesson 7 - Employee Stock Ownership Plan

10.7.A - Employee Stock Ownership Plan

1. Employee Stock Ownership Plans (ESOPs)

- Studies show that 90% of the employees who receive stock under option plans sell the stock as soon as they exercise their options, so the plans motivate employees only for a limited period.18 Moreover, many companies limit their stock option plans to key managers and executives. To help provide long-term productivity gains and improve retirement incomes for all employees, Congress authorized the use of Employee Stock Ownership Plans (ESOPs). Today almost 10,000 privately held companies and about 330 publicly held firms have ESOPs, accounting for over 10 million workers. Typically, the ESOP’s major asset is shares of the common stock of the company that created it, and of the 10,000 total ESOPs, about half of them actually own a majority of their company’s stock.

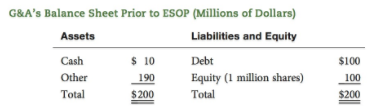

- To illustrate how an ESOP works, consider Gallagher & Abbott Inc. (G&A), a construction company located in Knoxville, Tennessee. G&A’s simplified balance sheet is shown below:

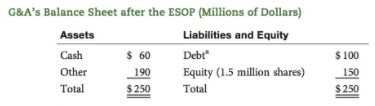

Now G&A creates an ESOP, which is a new legal entity. The company issues 500,000 shares of new stock at $100 per share, or $50 million in total, which it sells to the ESOP. The company’s employees are the ESOP’s stockholders, and each employee receives an ownership interest based on the size of his or her salary and years of service. The ESOP borrows the $50 million to buy the newly issued stock.19 Financial institutions are willing to lend the ESOP the money because G&A signs a guarantee for the loan. Here is the company’s new balance sheet:

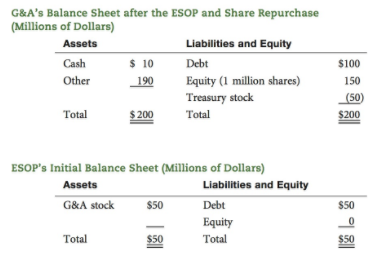

The company now has an additional $50 million of cash and $50 million more of book equity, but it has a de facto liability owing to its guarantee of the ESOP’s debt. It could use the cash to finance an expansion, but many companies use the cash to repurchase their own common stock, so we assume that G&A will do likewise. The company’s new balance sheets, and that of the ESOP, are shown below:

Note that though the company’s balance sheet looks exactly as it did initially, there is actually a huge difference—the company has guaranteed the ESOP’s debt and hence it has an off–balance sheet liability of $50 million. Moreover, because the ESOP has no equity, the guarantee is very real indeed. Finally, observe that operating assets have not been increased at all, but the total debt outstanding supported by those assets has increased by $50 million.

If this were the whole story, then there would be no reason to have an ESOP. However, G&A has promised to make payments to the ESOP in sufficient amounts to enable the ESOP to pay interest and principal charges on the debt, amortizing it over 15 years. Thus, after 15 years, the debt will be paid off and the ESOP’s equity holders (the employees) will have equity with a book value of $50 million and a market value that could be much higher if G&A’s stock increases, as it should over time. Then, as employees retire, the ESOP will distribute a pro rata amount of the G&A stock to each employee, who can then use it as a part of his or her retirement plan.

An ESOP is clearly beneficial for employees, but why would a company want to establish one? There are five primary reasons.

1. Congress passed the enabling legislation in hopes of enhancing employees’ productivity and thus making the economy more efficient. In theory, employees who have equity in the enterprise will work harder and smarter. Note too that if employees are more productive and creative then this will benefit outside shareholders, because productivity enhancements that benefit ESOP shareholders also benefit outside shareholders.

2. The ESOP represents additional compensation to employees: in our example, there is a $50 million (or more) transfer of wealth from existing shareholders to employees over the 15-year period. Presumably, if the ESOP were not created then some other form of compensation would have been required, and that alternative compensation might not have the secondary benefit of enhancing productivity. Also note that the ESOP’s payments to employees (as opposed to the payment by the company) come primarily at retirement, and Congress wanted to boost retirement incomes.

3. Depending on when an employee’s rights to the ESOP are vested, the ESOP may help the firm retain employees.

4. There are strong tax incentives that encourage a company to form an ESOP. First, Congress decreed that when the ESOP owns 50% or more of the company’s common stock, financial institutions that lend money to ESOPs can exclude from taxable income 50% of the interest they receive on the loan. This improves the financial institutions’ after-tax returns, which allows them to lend to ESOPs at below-market rates. Therefore, a company that establishes an ESOP can borrow through the ESOP at a lower rate than would otherwise be available—in our example, the $50 million of debt would be at a reduced rate. There is also a second tax advantage. If the company were to borrow directly, it could deduct interest but not principal payments from its taxable income. However, companies typically make the required payments to their ESOPs in the form of cash dividends. Dividends are not normally deductible from taxable income, but cash dividends paid on ESOP stock are deductible if the dividends are paid to plan participants or are used to repay the loan. Thus, companies whose ESOPs own 50% of their stock can in effect borrow on ESOP loans at subsidized rates and then deduct both the interest and principal payments made on the loans. American Airlines and Publix Supermarkets are two of the many firms that have used ESOPs to obtain this benefit, along with motivating employees by giving them an equity interest in the enterprise.

5. A less desirable use of ESOPs is to help companies avoid being acquired by another company. The company’s CEO, or someone appointed by the CEO, typically acts as trustee for its ESOP, and the trustee is supposed to vote the ESOP’s shares according to the will of the plan participants. Moreover, the participants, who are the company’s employees, usually oppose takeovers because they frequently involve labor cutbacks. Therefore, if an ESOP owns a significant percentage of the company’s shares, then management has a powerful tool for warding off takeovers. This is not good for outside stockholders.Are ESOPs good for a company’s shareholders? In theory, ESOPs motivate employees by providing them with an ownership interest. That should increase productivity and thereby enhance stock values. Moreover, tax incentives mitigate the costs associated with some ESOPs. However, an ESOP can be used to help entrench management, and that could hurt stockholders. How do the pros and cons balance out? The empirical evidence is not entirely clear, but certain findings are worth noting. First, if an ESOP is established to help defend against a takeover, then the firm’s stock price typically falls when plans for the ESOP are announced. The market does not like the prospect of entrenching management and having to give up the premium normally associated with a takeover. However, if the ESOP is established for tax purposes and/or to motivate employees, the stock price generally goes up at the time of the announcement. In these cases, the company typically has a subsequent improvement in sales per employee and other long-term performance measures, which stimulates the stock price. Indeed, a study showed that companies with ESOPs enjoyed a 26% average annual stock return compared to a return of only 19% for peer companies without ESOPs. It thus appears that ESOPs, if used appropriately, can be a powerful tool for creating shareholder value.

Última modificación: martes, 14 de agosto de 2018, 08:53