Reading: Lesson 1 - Types of Financial Records

8.1.A - Types of Financial Records

1. FINANCIAL RECORDS

- All businesses—large and small—must keep records. Financial records are organized summaries of a business’s financial information and activities. While all businesses are legally required to keep some records, the main purpose of financial records is to determine if the business is profitable. If a business is not making a profit, it will not be able to continue operating for long unless things can be changed. Financial records make it possible for owners and managers to understand a business’s financial performance and make the best possible decisions regarding the use of the company’s resources. A very small business could determine how profitable it is by using a business checking account to track all income deposited and by writing checks for all payments. The total deposits (income) less the total of all checks written (expenses) tell the business owner if the business is making money. However, this simple approach does not provide adequate information to fully understand the financial condition of the business. Businesses need complete and detailed records to satisfy their information needs. All companies must determine what records to keep, how to prepare and maintain them, and who should be responsible for the records. Once a records system is in place, managers can use the information to understand the business’s finances, complete financial planning, and establish controls.

- A record-keeping system is a manual or automated process for collecting, organizing, and maintaining the financial information of a business. There are many options for businesses to organize and maintain their financial records. A small business owner can keep the records personally or hire a bookkeeper or accountant. Larger businesses have finance and accounting departments with specially trained personnel to maintain financial records, prepare reports, and help with financial planning. Some businesses hire other companies to provide specialized record-keeping services or even to maintain all of the business’s financial records.

- Whether a record keeping system is simple or complex, it contains four elements—records, people, procedures, and tools. The system must be accurate, keep information safe and secure, and provide timely and accurate information. Before computers gained widespread acceptance in businesses, bookkeepers and accountants prepared and maintained all financial records manually. Few businesses rely on manual systems today. Easy-to-use and affordable accounting software has replaced most manual systems. However, standardized accounting forms and records systems for manual record keeping are available wherever office supplies are sold. Some small retail and service businesses use a cash register to gather most of the information needed for their financial records. Cash registers create printed tapes showing the details of each sales transaction. This information is often entered directly into accounting software. However, cash registers record only information on customer sales, which is an incomplete record of the financial transactions of the business. Businesses are replacing cash registers with point- of-sale (POS) terminals. POS terminals include cash register functions but also have credit and debit card processing capabilities and a scanner that reads product barcodes to update inventory records. The revenues and costs associated with each product can be tracked and analyzed using POS technology. With specially designed software and hardware, the POS terminal can meet unique sales and information gathering requirements of the business.

- Accounting is the process of recording, analyzing, and interpreting financial activities of a business. Today most firms use accounting software programs to maintain their financial records. Accounting software simplifies and speeds the record-keeping process while reducing errors. A desktop computer is adequate for most electronic record-keeping systems, but large companies need systems that are more complex. They need systems that can quickly and accurately process huge amounts of data gathered from multiple locations. Many of the day-to-day data entry and records management activities in large and small businesses are completed by bookkeepers and accounting clerks.

- Small businesses then hire an accounting firm as needed for specialized activities. Large corporations employ many bookkeepers and accountants, many of whom have specialized skills and knowledge. Data processing is the set of activities involved in obtaining, recording, organizing, and maintaining the financial information of an organization. A data processing center is the location where data processing activities occur. It contains the computers, software, security systems, and personnel that are needed to complete those activities.

- Some businesses have their own data processing centers. However, because data processing can be a highly technical and expensive process, many companies now contract with specialized businesses that operate large data processing centers. Some businesses choose to purchase all their data processing services, while other companies purchase services for selected tasks such as maintaining inventory records or payroll systems. Today, data can be transmitted instantaneously via the Internet from the point of origin to the data processing center and back to the business in the form of records and reports. Therefore, the data processing work for a company can be completed anywhere in the world— across town, across the country, or halfway around the globe. Large companies require large and complex automated systems for keeping records. The initial recording of financial transactions occurs throughout a company, wherever the transaction occurs. The data processing center receives the transaction data and processes them. The data are then provided to the accounting department, where the financial records and reports of the business are prepared and maintained. It is common for accounting managers to divide their accounting department into several sections. Each section is typically responsible for handling one or more specific accounting activities, such as maintaining cash records, receipt and payment records, depreciation records, and tax and payroll records. Accountants prepare financial reports for managers and help them understand the financial condition of the business in order to develop plans based on the financial information.

2. TYPES OF FINANCIAL RECORDS

- Financial records in all types of businesses have similar characteristics. However, each type of record has a unique purpose and provides specific information for managers.

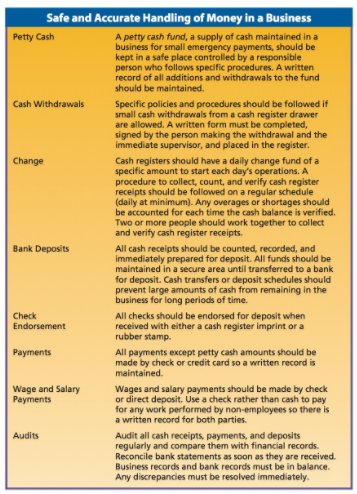

- Money, in the form of cash and checks, is constantly coming into a business from customers and other sources. Money taken in by a business is known as cash receipts. Cash goes out to pay for purchases made by a business. Small purchases may be made with actual cash, but most often businesses use checks for purchases. Cash payments made by a business are known as cash disbursements. No matter how large or small the cash receipt or payment, a written record of the transaction must be prepared and entered into the business’s record-keeping system. Regardless of how financial records are maintained, businesses must develop specific procedures for employees to follow when receiving payments by cash or checks and when using cash for purchases. Figure below lists several suggestions for the safe handling of money.

When a business sells goods and services, customers can make immediate payment with cash or check, or the business may accept credit. With credit, goods and services are provided with the expectation of future payment by the customer. The business maintains records of the credit transactions. An accounts receivable record shows what each customer purchases, pays, and owes. When a credit sale is made, an electronic or paper record of the transaction is transmitted to the accounting department. The accounting department enters the sale into the accounts receivable record. When the customer makes a payment, the record is updated with the amount of the payment. Businesses must also keep records showing money they owe and payments they make for all credit purchases. An accounts payable record identifies the credit purchases of a business, amounts owed, and payments made. Each time a credit purchase is made, details of the purchase are recorded in the accounts payable record. When payments are made, they are also recorded so the company has an accurate record of what it owes on each account.

An asset is anything of value owned. Businesses need to have a variety of assets, such as buildings, vehicles, equipment, and inventory, for use in their normal operations. The value of an asset decreases through use over time. This gradual loss of an asset’s value due to age and wear is called depreciation. For example, an auto repair shop owner buys a computerized diagnostic tool that costs $16,000. The owner knows from experience that at the end of five years the equipment will not be worth any more than $1,000. The owner estimates, therefore, that the equipment will wear out or depreciate at the average rate of $3,000 a year:

When the diagnostic equipment loses its usefulness, it must be replaced. Therefore, depreciation represents a cost to the business. Fixed assets are expensive assets of a business that are expected to last and be used for a long time. Buildings, land, and expensive equipment are common examples of fixed assets. Except for land, fixed assets depreciate over time. The value of each fixed asset is recorded by the company when it is purchased. Fixed assets become part of the property the business owns. As an asset wears out or becomes less valuable, the business is allowed, by law, to recognize the loss in value each year as an operating expense. The total amount of depreciation is deducted from the asset’s original value to determine its book value. Property may decrease in value due to obsolescence. That is, even though the asset is still usable, it becomes out-of-date or inadequate for a particular purpose. An older computer, for example, may not have the processor speed, memory, or storage capacity to run new software or meet the growing information demands of a growing business. Even though the computer still functions, it is no longer as valuable to the business. Therefore, obsolescence is a form of depreciation. The financial loss due to depreciation is very real, although it is difficult to determine objectively and with great accuracy. Therefore, the Internal Revenue Service (IRS) provides rules and procedures that businesses must follow in calculating depreciation. Businesses need to maintain depreciation records and use them in their planning so they have money available to replace assets as needed.

Financial statements list assets and their values, but they do not provide detailed information about these assets. As a result, a business must keep special records. For example, a business should maintain a precise record of insurance policies, showing such details as type of policy, the company from which it was purchased, amount, premium, purchase and expiration dates, and the amount to be charged each month as insurance expense. A business also maintains detailed special records for all fixed assets, such as trucks and forklifts. These records provide such information as asset description, date of purchase, cost, monthly depreciation expense, and asset book value. Asset book value is the original cost less accumulated depreciation. In the auto repair example above, the equipment depreciates at a rate of $3,000 per year. At the end of the second year, the $16,000 equipment will have an asset book value of $10,000:

Federal and state tax laws require every business to keep adequate records in order to report its income and expenses, file required forms, and calculate and pay taxes. Employers must withhold a certain percentage of each employee’s wages for federal income tax purposes. It must do the same for Social Security and Medicare. Other payments that employers must make to federal and state governments are for business taxes and unemployment compensation insurance. For business planning as well as for tax purposes, businesses must keep detailed payroll records for each employee: hours worked, wage or salary rate, regular and overtime wages paid, and all types of deductions and withholding made from the employee’s wages. Companies also record the value of benefits paid for each employee, such as paid vacation, sick days, and employer contributions to health insurance premiums and retirement plans.

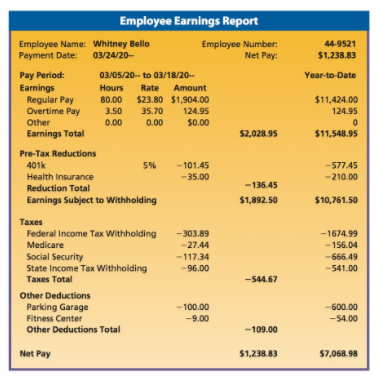

For tax purposes, each employee must fill out a W-4 form that provides information on the number of family members and exemptions. Using this information and a table furnished by the Internal Revenue Service, the employer determines the amount to withhold from the employee’s paycheck. Employers submit payments of these withholdings to the IRS. Most companies use a computerized payroll system to maintain personnel records, to calculate payroll, and to process payments for each employee. Some companies perform this function internally, but many businesses use payroll service companies. Many companies no longer issue actual paychecks to employees. The most common alternative to a paycheck is direct deposit. With direct deposit, funds are electronically deposited into employees’ bank accounts. Employers usually provide advice of deposit to let employees know that a deposit has been made. They may also provide an earnings report for each employee. This might be a printed statement given to each employee, an attachment emailed to the employee, or a secure page that can be accessed on the company’s website. An example of an earnings report appears in the Figure below.

All financial records of a business, including personal information about customers and employees, must be maintained and retained for many years. Information must be secure from theft and misuse and also should be protected from hazards of nature such as fire, floods, hurricanes, and earthquakes. Also, the growing threat of terrorism offers a new type of security issue businesses must address. Every business, therefore, should have secure areas such as vaults and safe rooms for records, computer equipment, and data storage. Disaster-proof and secure filing cabinets and other types of storage devices are also needed for maintaining important but frequently used documents. Measures to provide access to authorized people must be developed while keeping the information from those who are not authorized to access it. Important documents such as mortgages, deeds, leases, contracts, and other critical but infrequently used documents may be better placed in bank safe deposit boxes or other secure locations if there is no adequate protection in the business. Companies protect their computer records by using such precautions as firewalls and passwords to keep out intruders. Most large organizations have security personnel or consultants who regularly review computer systems and look for attempts to “hack” or illegally access information from the computer systems. Companies should also store backup copies of electronic records in a secure off-site location. Service companies rent storage space on their computers or in their climate-controlled data warehouses for safe record archiving and protection.

Última modificación: martes, 14 de agosto de 2018, 08:29