Reading: Lesson 1 - Financial Institutions

9.1.A - Financial Institutions

1. BANKS AND BANKING

- Businesses rely on the services of financial institutions. A business like Kilgore Kitchens in the opening scenario must deposit cash, make payments, invest excess funds, and borrow money. Knowledge of the types of financial institutions and the services they provide help managers and owners like Andrew and Julie use their financial resources wisely. A financial institution is an organization that collects money from clients and uses it for investments to benefit both the client and the organization. Banks were probably the best-known financial institutions for many years. Other nonbank financial institutions provided specialized services that banks were not legally allowed to offer. However, each year it is getting more and more difficult to distinguish among the services provided by various financial institutions. Nonbank financial institutions have rapidly expanded the services they offer, competing directly with banks in areas such as checking and savings accounts. The deregulation of banking has made it possible for banks to offer a variety of new investment products and other financial services. Computer technology and the Internet allow businesses and consumers to conduct many financial transactions online and have contributed much to changing how financial activities are completed around the world.

- Banks in the United States are financial institutions that historically have been regulated by the government to make sure financial services are widely available and that financial resources of individuals and businesses are protected. In order to operate, a bank must receive a charter. A bank charter authorizes the operation of a bank following the regulations established by the state or federal government. To be recognized as a bank, a financial institution must accept demand deposits, make consumer and commercial loans, and buy and sell currency and government securities. A demand deposit is money put into a financial institution that the depositors can withdraw at any time without penalty. A checking account is an example of a demand deposit account. Time deposits (also known as certificates of deposit or CDs) are made for a specified period of time and cannot be withdrawn early without some financial penalty. A commercial loan is a loan made to a business, whereas a consumer loan is a loan made to an individual for personal use. If the primary purpose of an institution is to offer financial products and services other than deposits and loans, it is classified as a nonbank financial institution. Although nonbank financial institutions initially developed to offer financial products such as insurance and investments, they have increasingly begun to offer services traditionally reserved for banks. The distinction between banks and nonbanks is fading fast.

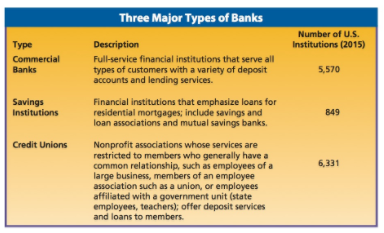

- Banks are often known as deposit institutions because their customers deposit excess funds for the purpose of earning interest on the deposits. Depending on the type of institution, deposits are accepted from individual consumers, businesses, organizations, and government agencies. The banks use those deposits to make loans to customers who need the financial resources for short or long periods of time. Those customers pay interest to the bank for the use of the funds. The bank accepts the risk that the loan may not be repaid. It takes steps to reduce the risk by carefully evaluating loan applicants and spreading the risk across a large number of loans. There are three major types of banks, based on the customers served and the types of deposits and loans offered. The three types are described in the Figure below.

- Commercial banks as a group are the largest and most important type of deposit institution. Commercial banks offer a broad range of services, and they serve many types of customers. More than 5,500 U.S. commercial banks have assets of more than $14.7 trillion, made up of loans to businesses, government, and consumers; private and public securities; cash; and real estate. They hold deposits from customers of more than $11 trillion. Commercial banks provide most short-term loans to consumers. Nearly 16 percent of their loans are consumer loans, with about 8 percent in credit card loans. They also make a large number of loans to businesses to finance operations as well as commercial real estate loans. About 50 percent of all loans are made to finance business and individual real estate purchases. Commercial banks provide checking and savings accounts for both consumers and businesses. Almost 18 percent of all deposits are demand deposits, and nearly 82 percent are various types of time deposits. The number of commercial banks peaked in the mid 1980's at nearly 15,000 banks. Since that time, competition and deregulation reduced that number significantly. The severe economic downturn of the mid to late 2000's led to many bank failures and more consolidations through mergers. The Figure above shows that the number of commercial banks declined by over 60 percent by 2015. Despite that decline, consumers still have ready access to commercial banks. The total number of branch offices has doubled in that same time from 41,000 to 82,000. The ten largest U.S. commercial banks are listed in the Figure below.

Savings institutions developed as local or neighborhood locations to promote thrift and savings. They encouraged community members to deposit some of their earnings and other funds and in return offered loans to borrowers needing funds. There are two common types of savings institutions—mutual savings banks and savings and loan associations. Mutual savings banks began in the early 1800's and are owned by their customers. Rather than buying shares as in a corporation, ownership is based on establishing a relationship with the bank as a depositor or borrower. The profits are divided and distributed in proportion to the amount of deposits of each owner. Customers who borrow funds from mutual savings banks do not have to be depositors or “owners.” Both short-and long-term loans are made for a variety of purposes, but a large percentage of the loans are made within the community for long-term needs such as financing home mortgages. Savings and loan associations served a similar purpose as mutual savings banks. They were often started by pooling the small savings of a large number of people and in turn lending that money back to their members for the purpose of building housing. Often the original savings and loan associations were dissolved when the building needs of members were met. Savings and loans were formed either as closely held corporations where members bought shares or as mutual companies where ownership was based on the value of deposits. Today, most savings and loans have expanded their purpose and no longer require membership to use their services. However, they still emphasize loans for real estate mortgages. Because of their limited size and services compared to many commercial banks, they often pay a slightly higher interest rate on deposits and charge lower mortgage rates. Together, mutual savings banks and savings and loan associations have assets of about $1.04 trillion, made up mostly of loans and leases. They hold customer deposits of just over $803 billion, over 91 percent of which is in time deposits.

Credit unions are not-for-profit financial organizations owned and managed by their members. Rather than making a profit, credit unions provide financial benefits to members such as higher interest rates on deposits and lower rates on loans. They also emphasize more personal service than many other financial institutions. Credit unions provide both demand and time deposits and emphasize shorter-term consumer loans such as personal loans, auto loans, and home loans of three to five years. Although there are large credit unions, many credit unions serve a very small number of customers who have a common relationship, such as employment, an organizational affiliation, or location. You must be a member to use the services of a credit union. Today nearly 100 million people in the United States are credit union members. Credit unions hold assets of nearly $1.2 trillion, including loans valued at over $734 billion. Because credit union members are owners, their savings make up most of the owner’s equity of the organizations. Total member deposits are just over $997 billion.

Banks operate in an environment of high risk. Customers who deposit funds with banks risk that the bank will not have adequate funds to pay the interest or return the money when the customer requests its return. When banks make loans to customers, they risk that the customer will be unable to repay the loan with interest according to the terms of the loan. Of course, customers should be careful to deposit money with banks that have the financial strength and history to protect deposits. Banks carefully review loan applicants and their applications to determine if they are creditworthy. However, there are many examples of bank failures that resulted in large financial losses to businesses and individuals. The bank failures during the Great Depression in the 1930's were so dramatic in terms of the number of people affected and the size of their financial losses that the federal government increased its regulation of banks and banking. Since that time there have been other economic downturns that have placed severe pressure on financial institutions. Even though banks sometimes fail, federal regulation has reduced the effect of failures on the economy and protected depositors’ assets.

The Federal Reserve System (Fed) is the central bank of the United States. It was developed to regulate banking and manage the economy through control of the money supply. Approved by Congress in 1913, the Fed is made up of a chairman and a board of governors appointed by the president of the United States. The chairman and board members are financial and economic experts who establish the interest rates at which member banks can borrow money. These rates in turn affect the rates on many of the loans and deposits made by consumers and businesses. Most commercial banks and savings banks are members of the Fed system and must meet its requirements and regulations, which affect the types of loans they can make, the amount of assets that can be loaned, and the security requirements for loans. Banks are required to keep a percentage of their assets in reserve, with some deposited in one of the 12 Federal Reserve district banks.

In 1933, consumers lost confidence in banks and tried to withdraw all of their money at nearly the same time. Banks had not kept enough money in reserve to cover all of the withdrawals. As a result, more than 4,000 U.S. banks closed, with losses averaging nearly $1,000,000 each. Those losses were actually suffered by the banks’ customers, who could not withdraw their deposits. Although many of those funds were eventually recovered and nearly 80 percent was repaid to consumers, Congress wanted to avoid another “rush” on the banks in the future. It established the Federal Deposit Insurance Corporation (FDIC), a federal agency that insures deposits in banks and savings institutions up to $250,000 per depositor in an insured institution. If a depositor has money in several accounts, the total amount insured is typically $250,000 with a few exceptions based on the type of account ownership. Since its creation in 1934, no insured deposits have been lost by customers of failed members of the FDIC. The FDIC charges member banks premiums for the cost of insurance. Only bank deposits are insured. Many banks offer a variety of other financial products, but these are not covered by the FDIC insurance. The FDIC also regularly examines the financial condition and financial statements of member banks to make sure they have adequate capital. If a bank becomes undercapitalized (having a high loan volume in relation to assets), the FDIC can force the bank to take corrective action, including a change in management. It can even force the bank to close if the problems are not corrected.

Credit unions cannot be members of the FDIC. However, credit unions that are members of the National Credit Union Association (NCUA) have a similar federal insurance plan. The National Credit Union Share Insurance Fund (NCUSIF) offers the same $250,000 insurance on member deposits as the FDIC.

2. NONBANK FINANCIAL INSTITUTIONS

- Nonbank financial institutions have grown rapidly because of the many valuable financial services they offer. Customers value being able to obtain many of their financial services through one organization. The growth of nonbank institutions can be traced to new laws and regulations that reduced restrictions on the traditional banking services they could offer, such as demand and time deposits. At the same time, the banking industry successfully lobbied for other laws that allow traditional banks to offer a broader range of financial services, including investments and insurance, which they previously could not offer. The resulting competition has led to an emerging group of full-service financial institutions, consolidation of businesses in the industry, and many new forms of products and customer services.

- Nonbanks exist in many forms. Stock brokerage firms, for example, not only buy and sell stocks and bonds but also offer checking and even credit card services. Some large brokerage firms also provide mortgages and insurance policies. On the other hand, banks are now allowed to sell stocks and bonds if they wish. Insurance companies and business pension funds are also nonbank financial institutions that offer long-term loans in large amounts to eligible businesses. Nonbanks also include investment companies such as mortgage, insurance, and finance businesses as well as investment firms. Competition to provide banking and other financial services has become fierce. New products and services are regularly developed to attract customers. With the growing number of choices, consumers and business investors must carefully study, understand, and compare companies and products to make the best financial choices and avoid unnecessary risks.

- A finance company specializes in providing installment loans and leases to consumers and businesses. Unlike banks, it does not accept deposits but obtains funds to make loans by issuing securities. A finance company often works with retailers selling expensive consumer products or manufacturers and vendors selling equipment to business customers. The products are sold on credit, and the finance company approves and owns the credit account. Many finance companies such as CIT Group and Springleaf Financial Services are independent companies specializing in consumer and business loans and related financial services. Some large manufacturers have a financial division that operates as a finance company, such as Nissan Motor Acceptance Corporation (NMAC) and John Deere Financial.

- Insurance companies collect premiums on insurance products and invest the premiums in securities, real estate, and other low to moderate-risk investments to earn money. In that role, they provide both business and consumer loans. In addition to selling insurance, most insurance companies offer a number of savings and investment products.

- Many companies offer employees retirement benefits. Those benefits are often invested in pension funds. Some pension funds are owned and managed by the employer or by an employee union. However, most are managed by an independent financial services firm. Both employer and employee make regular contributions to the pension fund throughout the employee’s working career. Those contributions are invested by the pension fund in stocks, bonds, real estate, and government securities. When the employee retires, money is returned from the fund as a lump-sum payment or as a regular series of payments over a period of years.

- A mutual fund is a company that pools the resources of a large number of investors to make a variety of investments. Depending on the type of mutual fund, the investments may be in stocks, bonds, government securities, or other financial instruments. Some mutual funds focus their investments in particular industries or types of securities, whereas others look for a more balanced set of investments. Investors purchase shares in the mutual fund. The price of shares increases or decreases based on the performance of the investments. Many mutual funds charge a small administrative fee for their services. The number of mutual funds and the value of their assets have grown dramatically as people rely on the expertise of fund administrators to increase the value of their investments. In 2014, there were more than 9,200 mutual funds in the United States serving over 90 million investors. The total asset value of those funds was $15.8 trillion.

- Securities and investment firms provide a variety of professional financial services for clients. Many serve as brokers, buying and selling securities, stocks, and bonds for their clients. Another service is underwriting new stock or bond issues. As an underwriter, the company purchases new securities from a company and then resells them to investors. It can also be a dealer, locating and purchasing securities with the intent of reselling them at a profit.

- Large companies that have been a part of the financial services industry have seen the value of offering customers a full range of financial products and services. They often buy companies that offer specialized services such as credit cards, installment credit, or insurance and combine them under the management of one corporation. They serve both business clients and individual consumers with savings and investment plans, loans and credit choices, fund management, and financial counseling. Companies such as American Express, HSBC, Merrill Lynch, and Barclays operate worldwide and manage trillions of dollars in client assets. Financial services companies have been the leaders in the blending of traditional banking and non-banking products and services. Large banks now sell insurance, securities, and other investments and provide financial counseling. Nonbank companies accept deposits, make loans, and provide credit card and check-writing services.

Última modificación: martes, 14 de agosto de 2018, 08:30