Reading: Lesson 2 - Common Financial Services

9.2.A - Common Financial Services

1. COMMON BANKING SERVICES

- In spite of the changes that have occurred in the financial world, financial services have improved greatly in recent decades. Today, the majority of banking institutions provide a host of services. Historically, the most complete line of banking services designed for individual consumers and small businesses was offered by commercial banks. Those services included a number of types of savings and checking accounts and various types and lengths of commercial and consumer loans. Many banks offer financial services such as accounting and tax preparation, financial planning, and financial advice, and even rent safe deposit boxes in which customers can store valuables securely. Now, as specialized banks and nonbanks become more competitive with commercial banks, they are offering the traditional bank services that their customers demand. At the same time, commercial banks are adding more and more nonbank financial services to respond to the competition, attract new customers, and increase their revenues. Two of the most common banking services are checking accounts and loans. Nearly all businesses and many consumers use these services.

- Checking accounts enable depositors to safely maintain cash in a bank or other financial institution and access it as needed. With most checking accounts, money is deposited in a demand account, meaning that money can be withdrawn at any time. Typically, money is withdrawn by writing a check. A check is a written order requiring the financial institution to pay previously deposited money to a third party on demand. Businesses use checks to pay for purchases or to make payments on loans and accounts payable. They also use checks to pay regular expenses such as payroll. Many businesses accept checks from customers as payment for purchases. Technology has dramatically changed the operations of checking accounts. Rather than making payments using paper checks, businesses and consumers increasingly use debit cards or ATM cards. Many businesses and most banks now offer online bill paying services, which allow customers to move funds electronically from their bank account to the company’s bank account. The results are the same as if a paper check was written and processed. However, no paper check is required and the processing of the payment is completed almost instantly.

- A typical consumer checking account requires the account holder to pay a monthly fee to cover the bank’s costs to administer the account. Banks may charge additional fees for services such as ordering checks. The bank may reduce or eliminate monthly fees if the account holder maintains a minimum average balance. Some banks even pay a very low interest rate on checking accounts with high balances. For these reasons, the costs, requirements, and interest rates should be carefully compared when opening a checking account. If fees must be paid or interest rates are very low, depositors should keep only the amount of money in the checking account needed to be able to pay upcoming bills and keep additional cash in accounts that pay a higher interest rate. Many part-time or small businesses use consumer checking accounts to handle the cash needs of their businesses. If a consumer checking account is used, the business owner should establish a separate account for the business. This prevents commingling of personal and business funds and provides accurate records for the business.

- Banks and other financial institutions offer business checking accounts that are different in some ways from consumer accounts. A checking account is used to handle most of the cash transactions of the business. This means that any cash payments made to the business, whether by cash, check, debit or credit card, or electronic payment will be routed through the business’s checking account. Also, most payments made by the company are completed by writing checks or making electronic payments from the checking account. Banks have established a variety of services that they offer with business checking accounts. The types of services available and the fees charged for those services vary. They are often based on the number and dollar amounts of transactions the bank processes for the business and the average daily or monthly balance the business maintains in the accounts it holds with the bank. Common services associated with business checking accounts include the following:

• Secure and rapid processing of cash, check, debit and credit transactions

• Accepting online customer payments and payments made through neighborhood convenience centers such as supermarkets, convenience stores, and pharmacies

• Online bill paying including sales and payroll tax payments to local, state, and federal governments

• Remote capture deposits allowing businesses to deposit customer checks by scanning, or taking a picture of, both sides of the check and transmit- ting the scanned images to the banks using an encrypted electronic file

• Print and online account reports and monthly statements documenting all transactions that have been recorded in the account including deposits, receipts, payments, and fees - Businesses with large account balances may be offered a cash management service (also known as treasury service) as a part of the checking account. With this service, the bank monitors all accounts receivable and payables as well as the cash balance maintained in the business’s checking account to minimize expenses and maximize the interest earned. Money is transferred in and out of the checking account daily with the goal of keeping the balance low and maintaining most funds in higher interest-paying accounts until needed. For more than 70 years, it was illegal for banks to pay interest on the money businesses maintained in a checking account. However, with the passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, banks and credit unions can now offer interest on all business checking accounts. Many business checking accounts still do not offer interest, and the fees charged may be greater than the interest earned. Therefore, businesses usually have interest-paying savings accounts as well as other investment accounts with financial institutions in addition to a checking account.

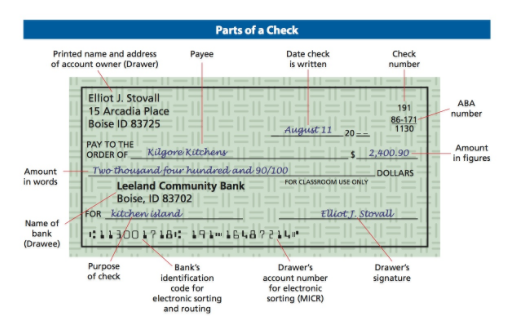

- Businesses must develop procedures and train employees to accept checks from customers. Accepting a check is the same as receiving cash. However, if the check is not completed properly, if there are not adequate funds in the customer’s account to cover the amount of the check, or if fraud is involved in the payment, the business may not receive the funds. A check written to Kilgore Kitchens appears in the Figure below. An employee accepting a check for payment must make sure all information is complete and accurate. In addition, the person writing the check must present proper identification to make sure the check is not stolen or forged. When the check is accepted, it should be properly endorsed immediately for bank deposit. An endorsement is the payee’s signature on the back of the check legally transferring ownership. Businesses often use stamped or printed endorsements on checks rather than a signature. That endorsement lists the name of the bank to which the deposit is to be made, the name of the business, and the checking account number. Many retail businesses have point-of sale-terminals or cash registers designed to process checks electronically. When a customer presents a check for payment of a purchase, the business employee examines the check and the customer’s identification. Then the check is scanned through a check-reading terminal that is connected electronically to a check clearing service. The service either approves or rejects the check based on information about the customer’s checking account balance. The terminal prints an endorsement on the back of the check so it is ready to be deposited. In the past, when businesses accepted printed checks, those checks were deposited in the business’s bank account. The bank would then route each check through other banks using a process managed by the Federal Reserve. When the check was presented to the check writer’s bank, the amount would be deducted from the depositor’s account and added to the business’s account. The process could take several days before it was completed. Today, most checks are processed electronically using procedures established by The Check Clearing for the 21st Century Act (Check 21). Rather than sending paper checks, banks can make “substitute” checks that are exact digital images of the original check. Those images can then be quickly transferred from bank to bank electronically. From its peak in the late 1990's, the number of checks written in the United States has declined about 10 percent each year. That decline has resulted from the increased use of debit cards as well as online banking and payment systems. In 2014, the Federal Reserve processed 5.7 billion checks through its system. Today nearly all checks are processed electronically.

Banks offer loans to both businesses and consumers. Before making a loan, the bank requires the prospective borrower to identify the purpose of the loan and provide financial evidence that the loan can be repaid. Most business loans provided by banks are for short time periods, often a year or less. A business may need funds to cover operating expenses at certain times, such as when it needs new equipment or when sales are temporarily slow. A common loan for reliable business customers is a line of credit, which gives the business a maximum amount it can borrow over a specified time period. The business borrows on the line of credit only when the money is needed, but it does not need additional approval as long as the maximum loan amount is not exceeded. Collateral is property a borrower pledges to assure repayment of a loan. If the borrower does not repay the loan, the lender has the right to use the pledged property for repayment. An unsecured loan is a loan that is not backed by collateral. Usually only successful, long-standing business customers can obtain unsecured loans. For new businesses, those without strong financial records, and most consumer loans, banks require a secured loan. A secured loan, also called a collateral loan, is a loan backed by something of value owned by the borrower. For example, if a business owned a fleet of delivery vans and wanted to borrow $100,000, the fleet could be acceptable collateral. In case of failure to repay the loan, the bank could sell enough of the vehicles in the fleet to collect the money loaned. Businesses may pledge inventory or accounts receivable to secure smaller loans or lines of credit. Typically a secured loan is for an amount substantially less than the actual value of the collateral. The bank does not want to own the collateral. If it must take ownership of the collateral in the event the loan is not repaid, it will want to quickly sell the collateral and recover the money loaned.

Banks earn income when they loan money by charging interest for the time period of the loan. Interest rates are based on the supply of and demand for money at any given time. As a result, the rate of interest can change daily, based on general business conditions. The lowest rate is the prime rate, which is the rate at which large banks lend large sums to the best-qualified borrowers. Small loans and loans to less-qualified customers are made at rates higher than the prime rate. Borrowers and lenders must establish a specific repayment plan so that the deal benefits both parties. Borrowers may be forced into bankruptcy and the lenders may be hurt financially if loans are not repaid. To help prevent losses, repaying a loan at regular intervals is safer than paying one lump sum at the end of the time period. Borrowers can then include the monthly payments in their budget plan and make sure they have adequate cash on hand for the payments. Rates may be set for the full term of the loan, or they may change during the loan period at predetermined times or based on specified conditions. An interest rate that does not change throughout the life of the loan is a fixed interest rate. A variable interest rate can increase or decrease during the life of the loan based on the factors used to adjust the rates. Often variable interest rates are based on changes in the prime rate or in the price of government securities. Variable interest rates are usually lower than fixed rates at the beginning of a loan but may become more expensive over the full term if economic conditions and government policies tighten the money supply.

2. TECHNOLOGY AND FINANCIAL SERVICES

- Remarkable changes are occurring in banking and financial services because of rapid advancement in computers, personal computing devices, and other forms of electronic technology. Much of the work once done by clerks, such as processing checks, recording deposits and withdrawals, and keeping customer accounts up to date, is now done electronically. Electronic funds transfer (EFT), transferring money by computer rather than by check, has enabled financial institutions to provide faster, improved services. For example, EFT transactions reduce the need for checks. Direct deposits, automatic teller machine transactions, and online banking are three common uses of EFTs.

- A direct deposit is the electronic transfer of a payment directly into a recipient’s bank account. Common uses of direct deposit include paychecks, Social Security benefit payments, and tax refunds. The use of direct-deposit banking has increased in popularity, especially for paychecks. Employees who select this service receive immediate use of their earnings. They no longer have to go to a bank to cash checks or make deposits. For each pay period, the employer must provide the employee with a record listing gross pay and all deductions. The Social Security Administration and the Internal Revenue Service encourage the use of direct deposit for benefit checks and tax refunds. In this way, the funds are immediately available to the recipient and government costs are reduced.

- An automatic teller machine (ATM) is a computer terminal that enables bank customers to deposit, withdraw, or transfer funds by using a bank-provided plastic card. The card has a magnetic stripe across the back containing account information. After swiping or inserting the card into the ATM, a card user enters a Personal Identification Number (PIN) to access a bank account. ATM's are located at banks and many other convenient places, such as grocery stores, airports, and malls. ATMs are now common throughout the world and can be used to obtain currency quickly and easily. In addition to making it much more convenient for customers to complete many banking activities, banks lower their operating costs by reducing the need for human tellers and increase income from service fees charged for some ATM transactions. Furthermore, banks use ATMs in many locations to serve their customers rather than opening additional branch offices.

- Electronic banking speeds business activities and serves customers more conveniently. Through computers, smartphones, and the Internet, banking without leaving the office or home has become common. Electronic banking makes it possible to obtain loans, pay bills, and transfer funds from one bank account to another. The Internet provides opportunities for banks and nonbanks to offer additional products and services and compete for customers. Most have websites publicizing their services. Customers can search the Internet for the best interest rates for loans, best savings account rates, and best checking account terms. Loan and credit card applications can be processed and approved quickly online. Most traditional financial institutions offer services via the Internet in addition to their on-site services. However, some banks are Internet-only banks and have no buildings customers can visit. Internet-only banks have several advantages over traditional banks. Not only can they perform most of the same services traditional banks offer, but they can also do it at lower cost. An Internet bank does not need large, costly downtown buildings with numerous branches from which to conduct business. It can operate from a single, low-rent building 24 hours a day, seven days a week, to reach worldwide customers. Banking operations centers may actually be located in other countries. For many customers, online banking can satisfy most day-to-day banking needs. A recent study found that a face-to-face banking transaction costs $1.36, an ATM transaction costs $.61, a mobile banking transaction costs $.19, a telephone transaction costs $.17, and an Internet transaction costs $.09. The relatively low-cost of Internet transactions is one reason many banks have developed easy-to-use websites, offer many Internet-based banking services, and encourage their customers to bank online.

Última modificación: martes, 14 de agosto de 2018, 08:30