Reading: Lesson 3 - Investing and Investments

9.3.A - Investing and Investments

1. INVESTMENT INSTRUMENTS

- Individuals, families, businesses, and other organizations need adequate financial resources to meet their needs. Money can be obtained in two ways—earnings resulting from the work of individuals or the operation of businesses, and earnings from investments. An investment is the use of money to make more money. When individuals or businesses have cash that is not immediately needed, it should be invested. There are many investment options available, whether the money to be invested is a small or large amount and whether it is available for a short or long time period. Some types of investments carry greater risks than others and some provide greater returns or earnings than others. Interest rates on some options can change rapidly while others remain the same for months or even years. To make wise investment decisions, business managers and individual investors need to know about the types of investment instruments and how to choose among them to meet their investment goals. Most investments are made using the services of financial institutions. Those institutions are constantly seeking new and better ways to serve customers. They offer a wide variety of financial instruments from which customers can select to best fit their investment needs.

- A checking account is a demand deposit through which investors can safely maintain money in a financial institution yet access it at any time through writing a check or making an electronic withdrawal. Many checking accounts pay a very low interest rate if the account balance is kept above a certain minimum amount. If a balance falls below the minimum, the bank may charge a service fee or eliminate the interest. Investors with small sums of money find interest-bearing checking accounts a convenient way to save while having easy access to the funds to pay expenses. Because checking accounts are not primarily designed as savings instruments, however, they serve an investment purpose only to a limited extent. Often the fees associated with a checking account are greater than the interest earned.

- A savings account is also a demand deposit account that allows customers to make deposits, earn interest, and make withdrawals at any time without financial penalties. Investors may deposit small amounts, but the interest rates are usually lower than those on other investment instruments. The bank may charge a service fee if the amount on deposit falls below the minimum balance required. Interest rates may increase slightly if the amount placed in savings is relatively high. However, the interest rate is still quite low compared to rates on other investment choices.

- A certificate of deposit (CD) is a time deposit account that requires a specified minimum deposit for a fixed period at a fixed interest rate. Banks offer CDs for $500 or more and for periods ranging from three months to ten years. Typically, the longer the term of the CD, the higher the interest rate earned. For example, the interest rate on a six-month CD is normally less than on a two-year CD. Although CDs usually pay a higher rate of interest than savings accounts, a CD cannot be withdrawn before its stated time without penalty—a substantial loss of earned interest. Interest is paid regularly on a certificate of deposit, and the interest can be withdrawn as it is earned. If the interest is not withdrawn, it is added to the value of the CD and earns additional interest during the remaining term. CDs are negotiable instruments, so if money is needed, the CD can be sold. Usually the bank where the CD was purchased will buy it but at a lower amount than its current value. If the value of the CD is significant, it may be worth the effort to search for other buyers and compare offers. If current interest rates are much lower than the rate being earned by the CD, it may be possible to sell it for more than it has earned. This situation is unusual but can occur with CDs that are purchased for long terms such as five or ten years.

- A money market account is a type of savings account in which the deposits are invested by the financial institution in short-term, low-risk investments, such as government-backed securities. The interest rate on the account is not fixed. It goes up and down as interest rates in the economy change. Financial institutions often grant check-writing privileges on money market accounts. The number of checks written during a given time period, such as a month, may be limited and a minimum balance is usually required. Unlike CDs, there is no minimum time the money must remain in the money market account. Depositors can withdraw their money at any time. Also, initial deposits may be as low as $500. Investors often put funds in money market accounts when they will need the money soon or when they want to earn some interest while waiting for a more profitable investment opportunity. Because government-backed securities are not very risky, the interest paid on money market accounts is generally lower than for other stock or bond investment options. However, money market accounts generally pay slightly higher interest than a typical savings account.

- A savings bond is a non-negotiable security sold by the U.S. Treasury. Non-negotiable means the bond cannot be sold; it must be held and redeemed by the original registered owner. Savings bonds are especially useful to small investors because they can be purchased frequently in small amounts starting at just $25. However, they can also be owned by companies, estates, and trusts and can be purchased in any amount up to $10,000. The total amount of savings bonds that can be purchased by an investor during any year is $10,000 per series.

- Savings bonds offer several advantages to investors. Interest earned is exempt from all state and local income taxes. Federal income tax must be paid but can be deferred until the bonds are redeemed. Interest earnings may be excluded from Federal income tax when bonds are used to finance education. Savings bonds are one of the safest investments because they are backed by the U.S. government. Bonds can be used as short- or long-term investments. Savings bonds must be held for a minimum of one year before they can be redeemed. If a bond is redeemed in fewer than five years, a three-month interest penalty will be applied. Savings bonds continue to earn interest for up to 30 years. In the past, savings bonds were sold in both paper and electronic form, but direct purchase of paper bonds has been phased out. People who currently own paper bonds can still hold them until they are redeemed. Bonds can be purchased through an online account opened at TreasuryDirect, the financial services website of the U.S. Department of the Treasury. A one-time purchase can be made, or an investor can arrange to make regular purchases by scheduling a recurring deduction from a bank account. Savings bonds can also be redeemed online with appropriate information and authorization. The money is transferred directly into the owner’s bank account.

- There are currently two series of savings bonds being sold, Series I and Series EE. The primary difference between the two series is the way the interest rate is determined. Series I bonds earn interest in two components: a basic fixed-rate and an additional adjustable rate called the inflation rate. Both rates are set each May and November. The fixed rate applies to all bonds sold during the six-month period after the rate is announced. That rate is paid for the life of the bond. The adjustable rate (inflation rate) is applied to the Series I bond every six months based on the current Consumer Price Index (CPI). During times of inflation, the inflation rate increases the total rate of interest paid on the bonds. If the economy is experiencing deflation, the total rate may actually fall below the fixed rate for the six-month period but can never fall below zero percent. Series I bonds are electronic unless purchased through tax refunds. Series EE bonds earn interest at a fixed rate for the life of the bond. As with Series I bonds, the rates are set each May and November and apply to all bonds sold during that six-month period. Series EE bonds are guaranteed to double in value if held for 20 years. If the fixed interest rate does not result in the bond doubling in value, the U.S. Treasury will make a one-time adjustment at the end of 20 years. If the bond is not sold, it will continue to earn the original fixed rate for an additional 10 years.

- A mutual fund pools the money of many investors primarily for the purchase of stocks and bonds. Many investors believe they do not have the time or expertise to select individual stocks and bonds and prefer to purchase shares in mutual funds. A mutual fund company develops one or more funds and makes the decisions about the types of investments for each one. Professional fund managers and their staff carefully evaluate and select a variety of securities in which to invest the fund’s money. Fund managers work to select stocks or other securities that will increase in value from the time they are purchased until they are sold. The goal is to earn a high rate of return on investors’ money. Most mutual funds require a minimum investment of $500 or more. Also, investors may need to document that they have adequate financial resources to risk in the mutual fund investment. Investors can easily transfer money from one fund to another, but there may be administrative charges for those changes as well as for general fund management. Risk is a major consideration in selecting mutual funds. There is no guarantee that the total investment will not be lost if fund managers make poor investment decisions or the economy suffers a serious downturn. Some funds reduce the level of risk by investing in bonds and other relatively safe investments. Those funds aim to generate a steady income for investors who do not expect the rapid growth in their investments that more risky funds might produce. Whenever sales of stocks and bonds are made by the fund manager that result in profits, or if dividends are paid on the stocks held in the fund, investors must usually pay taxes on their share of those profits. When investors sell their shares in a mutual fund, they will usually have to pay taxes on any increase in the value of the fund during the time they participated.

- The U.S. government borrows money from investors by selling bills, notes, and bonds backed by the Treasury. Treasury instruments are securities issued by the U.S. government. They are used to finance the costs of running the government when income from taxes is not available or when costs exceed the revenues collected. Approximately $7 trillion in government securities were issued in 2014. Treasury instruments are considered one of the safest of all short-term investments because they are backed by the U.S. government, which has the resources to meet interest payments on the securities as they become due. The instruments differ in the term of investment and the interest rates paid. Treasury instruments are sold at auctions where prospective purchasers bid based on the interest rate they are willing to accept. The securities are sold at the lowest available interest rates. Treasury securities are normally purchased from the government by financial institutions and brokers. They then are resold to individual and business investors. Individuals are also able to purchase securities online directly from the Department of the Treasury. Today all Treasury securities are issued in electronic form rather than paper.

- Businesses and individual investors with large sums of money frequently invest in Treasury securities because they are practically risk free and are easy to buy and sell. All Treasury securities are very liquid, meaning they are easily traded even though they may not mature for several years. Because the interest rates on securities fluctuate based on demand and economic conditions, investors are willing to purchase securities owned by other investors, usually at a discounted price, with the hope of making a profit. A Treasury bill, or T-bill, is a short-term security that pays the lowest interest rates of the various Treasury instruments. T-bills are sold in $100 multiples, but investors can purchase multiple amounts up to a total of $5 million. The bills mature in 4, 13, 26, or 52 weeks. T-bills are purchased at a discount based on the interest rate of the security. For example, a $1,000 bill may cost $960. When it matures in one year, the owner is paid the full $1,000. The $40 difference reflects a 4 percent interest rate.

- A Treasury note is a medium-length security that is available in $100 multiples and matures in 2, 3, 5, 7, or 10 years. Treasury notes are fixed-rate securities, meaning the interest rate remains the same throughout the term of the note. Interest is paid every six months. When the note is initially purchased, the investor may pay a premium or discount from the face value of the note. That increase or decrease in price reflects the demand for the notes and the value investors believe the note will have at its maturity.

- A Treasury bond is the longest-term U.S. government security. As with the other securities, the bonds can be purchased in $100 multiples. Treasury bonds pay a fixed rate of interest every six months until they mature. The bonds mature in 30 years, although they can be bought and sold on bond markets for shorter periods of time. Investors can purchase up to $5 million of bonds at an auction. Treasury bonds are auctioned as needed by the government but not usually as frequently as notes and bills. Sometimes not all of the available bonds are sold at the original auction, and the government may later hold a reissue auction to sell the remaining amount.

- Investors concerned about the effects of inflation can purchase TIPS. Treasury Inflation-Protected Securities (TIPS) are marketable securities issued by the U.S. Department of Treasury. Their principal is adjusted based on changes in the Consumer Price Index (CPI). Like other U.S. government securities, TIPS are sold at auction and can be purchased by individual investors or businesses. Purchases can be made directly from the U.S. government or through banks and brokers. They are frequently purchased as a part of a mutual fund so investors can own shares of the fund rather than individual securities. Since TIPS are marketable securities, they can be bought and sold by investors during their term and are traded on securities markets.

- TIPS are sold in increments of $100 with a purchase amount ranging from $100 to $5 million. TIPS are issued for 5-, 10-, and 30-year terms. The unique feature of TIPS is how they are adjusted by the CPI. The securities are originally sold at auction with a fixed interest rate that is determined by the auction. That interest rate remains the same for the term of the security and is paid on the principal every six months. However, the principal is adjusted to reflect the current CPI. Therefore, if the CPI rises, the principal increases; a decline in the CPI reduces the principal. At the end of the term, the owner is paid the adjusted principal or the original principal, whichever is greater. In that way, investors have protection against both inflation with the semiannual CPI adjustment and deflation with the final principal adjustment.

2. MAKING INVESTMENT CHOICES

- Business managers need to make investment decisions carefully. They need to consider the financial condition of the company, the amount of available cash and cash flow projections, and all available alternatives for investments. To make good choices, business investors must understand how investment trading works and set investment goals based on the amount of liquidity, safety, growth, and diversification that is best for the business.

- Buyers and sellers trade all types of securities through special financial markets. The securities are typically bought and sold through the services of securities and investment organizations. For help in making investments, individuals and businesses often consult investment advisers, brokers, or dealers. Investors ask their brokers to buy or sell certain securities. The brokers then process the requests through the appropriate financial market that connects buyers and sellers. Public corporations that want to sell their stock to investors must be listed on a stock exchange. Although there are a number of such exchanges, the two largest U.S. exchanges are the New York Stock Exchange (NYSE) and the NASDAQ exchange. Technology firms, such as Microsoft, Intel, and Cisco Systems, are listed on NASDAQ, which is the nation’s first electronic stock market. The much older New York Stock Exchange trades on Wall Street. Floor traders, who historically bought and sold securities face to face, now have been replaced by electronic trades. The NYSE attracts more traditional companies. Most stock exchanges handle stocks, bonds, and other types of investments. Mergers and partnerships among stock exchanges continue to evolve as electronic trading grows worldwide. Other U.S. exchanges exist to trade commodities, including the Chicago Board of Trade, Chicago Mercantile Exchange, Memphis Cotton Exchange, and the Minneapolis Grain Exchange.

- A stock index is a kind of average of the prices of selected stocks considered to be representative of a certain class of stocks or of the economy in general. Investors watch the movement of the indexes to get a sense of stock market trends for those types of stocks and for the overall growth of the economy. The most well-known indexes in the United States are the Dow Jones Industrial Average Index, the NASDAQ Market Index, and Standard & Poor’s 500 Index (S&P 500). When compared over time, each index provides investors with a picture of what is happening in the nation’s and the world’s financial markets. An index trend of rising share prices may influence investors to buy more shares, and a downward trend may prompt them to sell some shares. Unfortunately, predicting when the market will reach its low and high points is nearly impossible, even for the most skilled investors.

- Managers need to understand financial investing in order to maximize returns for their business, employee retirement plans, and their own personal investments. Investment planning involves developing a strategy that balances the trade-off between risk and returns as well as identifies the planning horizon, or length of time the funds will be invested. A short planning horizon requires that investments be liquid. Liquidity refers to the ease of turning an investment into cash without significant loss.

- For example, checking accounts are very liquid. Depositors can withdraw their deposit as cash whenever they want without penalty. Certificates of deposit are less liquid. If depositors withdraw their money from a CD before the end of its term, they have to pay a penalty, which may be substantial. If a small company, such as Kilgore Kitchens in the opening scenario, needs cash regularly, it should choose more liquid investments. Kilgore’s owners might choose to invest in money market accounts rather than mutual funds so they can get cash when they need it with a low risk of financial loss. On the other hand, an established, profitable firm may have a steady source of cash from its operations. Instead of needing cash soon, it may need to replace costly equipment in five years, so it may choose to invest in less liquid but more profitable investments. The different objectives of these two firms will determine, in part, the investments they select.

- A second investment goal is the degree of safety desired. In general, riskier investments should have higher earning potential than less risky investments. However, with riskier choices, investors are more likely to lose all or part of their investment. Some investors want maximum safety—they do not want to risk losing any of their money. Treasury notes and bills might be appropriate choices for these investors. To achieve a high degree of safety, they will likely have to accept smaller earnings on the investment. Investment in savings accounts, money market accounts, and government securities should appeal to them because of the low risk. Other investors like to take some risks for the opportunity to earn more money. These investors might prefer to buy stock in a rapidly growing corporation, in international companies operating in countries with strong economies, or in companies developing exciting new technologies.

- The third investment goal involves the trade-off between investment growth and a stable income from the investment. Investors who do not need a steady income from their investments and are willing to invest for long periods of time will choose to invest in growth-oriented corporations. They hope to see their investments grow at a faster rate than inflation. Investors who want to count on a regular income might choose to invest in stocks or mutual funds with a history of paying high dividends.

- Most experienced investors also suggest another rule that pertains to safety: “Don’t put all your eggs in one basket.” Investors should diversify, that is, spread their risk by placing money in different categories of investments. A diverse investment plan creates an investment portfolio. An investment portfolio includes a variety of investments such as stocks, government bonds, real estate investments, mutual funds, and other types of investments. For example, a diversified portfolio investment plan might put one-third of available investment money into bonds, one-third into stocks, and one-third into money market accounts. To follow this rule further, not all investments in bonds should be in one company, nor should all stock investments be in one corporation. Diversification greatly reduces the risk factor.

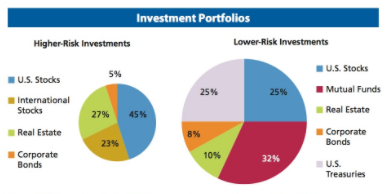

- The planning horizons of individual investors will influence the portfolio. For example, the Figure below shows two investment portfolios. The higher-risk investment portfolio is considered more aggressive because of its higher percentage of stocks, including international stocks which can be more volatile. Real estate, depending on the type of investment, can also have higher risks. High- yield corporate bonds will have a higher risk than low-yield government bonds. Younger investors planning for retirement may choose this portfolio. Because they have a longer planning horizon, they can take greater risks and adjust the portfolio over time. A lower-risk investment portfolio will most likely have a lower-risk profile made up of high-grade, low-risk stocks and corporate bonds. Mutual funds, such as those tied to the S&P 500 Index, are a lower-risk investment. U.S. Treasuries are likely to provide the lowest return but will protect the principal invested. This low-risk portfolio may fit the needs of retirees who want more certainty of returns in the short term. Money managers for institutions make these same calculations. A money manager for a city would most likely invest funds in low-risk investments. Some banks allow their money managers to choose more risky investments. This can result in higher returns but can also create grave risks. In 2012, JPMorgan Chase suffered a $2 billion trading loss due to the “egregious” failure of the bank’s management to control investment risks.

Investing requires a trade-off between a short-term need for funds and a long- term expectation of returns. To pay bills, individuals and businesses need liquid assets, or assets that can be turned into cash quickly. Businesses may use a short-term budget plan, such as five years, for strategic growth. To ensure a secure retirement, individuals need to make investment decisions for a long-term horizon. The U.S. stock market, as measured by the S&P 500 Index, has a historic return of over 11 percent over a long-term period (1928–2014) and an intermediate-term period (1965–2014). Over these periods of time, the market has both climbed and dropped. For example, a $500 investment in 1995 with an S&P 500 Index mutual fund would have grown to over $1,500 by March of 2000. By October of 2002, the Index dropped to just over $800. The market climbed again to reach almost $1,600 in October of 2007 before dropping to just over $683 in March of 2009. By 2015, the market recovered to reach over $2,000. A long-term investment from 1995 to 2015 would have provided a total return (gain) of over $1,500 on the $500 investment. This is a 7.18 percent annual return on the original investment.

Lower-risk investments often provide a lower return, but the investment interest can compound over time. Compound interest is accumulated interest on an investment added to the original principal, with the new total earning additional interest in the following period. For example, a $500 investment earning 5 percent compound interest each year will pay back $25 in interest the first year. The new total of $525 is used to determine the second year’s return. At the end of the second year, an additional $26.25 ($525 × .05) will be added for a total of $551.25. Over the same 20-year period from 1995 to 2015, a $500 investment compounded annually at 5 percent would return a total of $1,326.65. While this is a lower return than the S&P 500 Index, it was obtained with lower risk.

Modifié le: mardi 14 août 2018, 08:30