Reading: Lesson 6 - Insurance Principles

9.6.A - Insurance Principles

1. INSURANCE AND RISK REDUCTION

- If you have $5 in your pocket, there is a risk that you might lose it. Although you do not want to lose the money, the loss would be an inconvenience rather than a serious problem. However, if you own a $400 bicycle, you may not be able to afford to replace it if it is stolen. You may choose to buy insurance to protect against the larger loss. If you own a business, you face uncontrollable events that could result in financial loss. A fire could destroy your building. Someone might steal your property or cash. A customer or employee could get hurt at the business and sue you. Or an important employee could suddenly leave the firm, leaving a gap in the skills needed to run the business. Some events could be minor (like a broken window) and have little effect on the business. However, a major loss could result in the failure of the business. Consider the problem Ivy Montaigne (from the Reality Check) would face if a fire destroyed her jewelry store. Without proper insurance, she would have no way to replace her losses and reopen the business. Without insurance, most businesses do not have the resources to survive a loss of that size. Businesses face risks every day. Managers must determine the types of risk the business is likely to face and find ways to reduce or eliminate the risk. If an important risk cannot be eliminated or reduced, the business may purchase insurance to protect against a loss that would result in its failure. Insurance is a risk management tool that exchanges the uncertainty of a possible large financial loss for a certain smaller payment.

- Just as you would not buy insurance to protect against the loss of a $5 bill, businesses do not insure against every possible financial loss. As a normal part of operations, businesses experience losses due to operational problems. Planning can anticipate some problems and prevent them from harming the business so much that it cannot continue to operate. Most businesses expect a certain amount of shoplifting and employee theft. Rather than insuring against that loss, they take steps to improve security. For example, if Ivy loses one inexpensive piece of jewelry, she might be able to make up for the loss through additional sales. However, she would not be able to handle the financial loss associated with the theft of many expensive pieces as the result of a burglary. She needs to manage risk by making sure theft protection equipment and procedures are in place and by having insurance. Businesses can also lose money if employees do not show up for work. An absent employee’s work will not be completed unless the company takes some action to get the work done. Because large businesses expect a number of employees to be absent on any given day, they may have part-time workers available on short notice or have a contract with a temporary employment agency to provide replacements. Some businesses may actually employ more people than necessary because of the expected absentee rates. Managers should watch absentee rates carefully and keep them as low as possible through policies, incentives, and penalties.

- In most manufacturing processes, small amounts of materials are wasted or damaged. To make sure that losses do not interfere with production, a company should keep a larger quantity of those materials on hand to ensure an adequate supply to complete production. Planning, training, and controls for production processes should also reduce the amount of material loss in the manufacturing process. Many businesses, such as banks, investment firms, and insurance companies, base their operations on records. The records are so valuable that the businesses could not operate if the records were damaged or destroyed. In this case, insurance is not adequate protection. The businesses must rely on the safety and security of their records. Physical records are stored in well-protected, secured areas, and electronic records are backed-up frequently and held on secured servers. They also keep duplicate records in a separate location, often in another city.

- Another way businesses attempt to protect their vital operations is with an emergency operations plan. Businesses anticipate the types of emergencies that could occur, the protection required, and ways to respond. Each department in the company regularly practices the plan. For example, a manager may be asked without warning to assume that an electrical problem has shut down all computers in a department. The department must recover and operate again as quickly as possible by following the procedures developed in the emergency operations plan. In each of the cases described, the company is gathering information, making plans, and in some cases, spending a small amount of money to prevent large losses. This may be a better strategy for the company than purchasing insurance for those losses, but it does not replace the need for insurance.

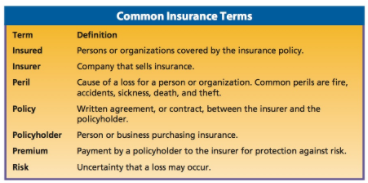

2. BASIC INSURANCE CONCEPTS

- Even with effective management, companies cannot reduce or eliminate all risks. They will need to purchase insurance to cover the possibility of large financial losses that they might suffer from many types of risks. The Figure below defines some basic terms related to the purchase of insurance.

It is difficult for one business to predict specific losses or the amount of those losses. However, many businesses face the same types of perils. Based on records kept over many years, insurance companies can estimate that a certain number of businesses will have fires each year and a percentage of merchandise will be shoplifted from retail businesses. By grouping the loss records of a very large number of businesses, insurance companies can estimate the probability of a certain type of loss and the amount of the loss that a business might suffer. For example, using historical records of fire losses over many years, insurance companies easily estimate the expected losses from fire damage that 10,000 businesses will suffer during a year. The actual amount of loss in a specific year might be different from the estimate, but over a number of years the estimates prove to be very accurate. Insurance companies insure only against losses that are reasonably predictable. Because they cannot know which specific business will suffer a loss, they spread the cost of the predicted losses across many businesses by selling many policies. Each policyholder pays a regular premium to the insurance company to insure against a specific type of loss. A premium is a small amount of money that pays for protection against a larger possible loss.

Insurance companies use the funds collected from policyholders in somewhat the same way that banks use deposits, making investments that earn an income. They then use the income to cover losses suffered by insured companies. To make a profit, the insurance company must earn more from premiums and investments than it pays out in claims to policyholders. Sometimes insurance companies lose money because they do not make wise investments or because policyholders have many more losses than the company anticipated. For example, several large natural disasters (hurricanes, earthquakes, floods, and fires) may occur in multiple areas of the United States at about the same time. Because of the number of disasters and the large amount of property in each area damaged or destroyed, insurance companies would have to pay out a much higher amount than they expected. Some small insurance companies might fail, and larger companies will raise their rates to recover their losses. To protect themselves from greater than expected losses, insurance companies often share the risks they have assumed with other companies through reinsurance. With reinsurance, another insurance company charges a premium to cover some of the risk facing the original insurer.

An insurance rate is the amount an insurance company charges a policyholder for a certain amount of insurance. For example, a business may pay $60 a year for each $10,000 of property insured against fire loss. Rates vary according to the risk involved. For instance, if a particular type of business, such as convenience stores, experiences a large number of thefts, theft insurance rates are likely to be higher for that type of business than for dry cleaners, which have a lower rate of theft. If fire protection is poor in a particular city or the building codes do not require fire walls or sprinkler systems in a building, the fire insurance rates will be high for that business owner.

Calculating insurance rates is a very scientific process performed by people known as actuaries. Actuaries review records of losses, determine the number of people or organizations to be insured, and then use statistics to calculate the rates insurance companies must charge to be able to cover the cost of losses and make a reasonable profit. Insurance companies compete with each other for business, so they must set their rates carefully. If rates are set too high, potential customers will purchase from a company with lower rates. However, if rates are set too low, the insurance company may sell many policies yet be unable to pay for the valid claims that occur among its policyholders. Insurance companies are very careful in setting insurance rates and rely on skilled and experienced professionals to determine possible losses, total amounts of premiums to be collected, and overall return on investments. In many cases, state governments have departments that review rates charged by insurance companies to make sure those rates are fair to the purchasers and insurance companies. Regardless of the basic rates set by an insurance company, the rate for a specific policyholder may be lower or higher than the basic rate, depending on circumstances. For example, a new building that has an automatic sprinkler system and is located where there is good fire protection can be insured at a lower rate than an older building that does not have a sprinkler system and is located far from the nearest fire department. In many states, automobile rates vary from the basic rate depending on the driver’s age and accident record and the brand, model, and age of the car.

An insurance policy contains information about how the contract may be terminated. Most property or liability insurance contracts may be canceled by the insurer or may not be renewed when they expire if the insurer believes the risk has increased. If the insurer cancels the insurance, it must give enough notice to policyholders to allow them time to find another insurer. Most states have passed laws that do not allow companies to arbitrarily cancel insurance without an approved reason. Many states allow companies and individuals whose insurance has been canceled to purchase insurance from a special state-sponsored fund, although often at a much higher rate.

To insure any kind of property, the policyholder must have an insurable interest in it. An insurable interest is generally defined as the possible financial loss that the policyholder will suffer if the property is damaged or destroyed. For example, if a business owns a van, it has an insurable interest in that van. If the van were stolen or destroyed in an accident, the business would suffer a financial loss. People who use a building for storage have an insurable interest in the items stored in the building, even though they do not own the building. A fire could destroy their property in the building, causing financial loss. Even if their property is not damaged, they could suffer a loss by having to relocate to another building as a result of the fire. The amount of a policyholder’s insurable interest in the property to be insured is usually specifically indicated in the policy and forms the basis for the insurance rate.

Many insurance contracts include deductibles. A deductible is the amount the insured pays for a loss before the insurance company pays anything. A deductible makes the insured responsible for part of the loss in return for a lower premium. For example, if a vehicle insurance policy has a $500 deductible and a $3,500 loss occurs, the insured is responsible for the first $500 (the amount of the deductible) and the insurer pays $3,000. If the loss is only $400, the insured would bear the entire loss, and the insurer would pay nothing. To reduce their premiums, policyholders often choose to include a higher deductible in their policy if they can afford to pay the amount of the deductible in case of a loss. For example, the premium for an auto insurance policy with a $250 deductible may be $1,850 a year. The premium for a $500 deductible policy may be $1,600. Having the $500 deductible policy saves the policyholder $250 a year if there are no claims. Of course, if there is a loss, the policyholder must pay the first $500 rather than $250.

3. NON-INSURABLE RISKS

- Businesses are also concerned with risks for which there is no insurance. It is particularly important for businesses to recognize and plan for noninsurable risks since it won’t be possible to receive payments from an insurer if a loss occurs. Examples of noninsurable risks faced by businesses are described below.

• Fashion, styles, and product features constantly change. If consumer tastes change, a business may suffer a loss if it can’t sell existing inventory or it must drastically reduce prices.

• A business that is new or has well-maintained equipment and uses the latest technology may attract customers away from a business that appears outdated or run down.

• Improved methods of order processing, product handling, delivery, or customer service may give one business an advantage over its competitors.

• The owners and managers of a business are counted on to make effective decisions. But decision making is risky. The wrong decisions or unethical or illegal actions by managers or employees can result in financial loss or even failure of the business.

• Changes in economic conditions present another serious risk. Rising unemployment rates cause people to be more careful when spending their money. Higher prices on commodities such as fuel and natural resources add to business costs and may cause customers to spend less on all types of purchases.

• Within any business community, there are numerous local risks. For example, extensive road maintenance or infrastructure repairs on a major street may cause customers to change their shopping behavior. Zoning changes made by a local government may have a negative effect on certain types of businesses. A major plant closing may result in the inability of surrounding businesses to survive. - Insurance cannot protect businesses from these and similar risks. Unless managers anticipate these risks and take action, they may find their businesses in danger of failing. Noninsurable risks pose a great challenge to managers.

Последнее изменение: вторник, 14 августа 2018, 08:30