Reading: Lesson 7 - Types of Business Insurance

9.7.A - Types of Business Insurance

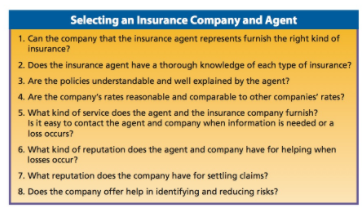

1. SELECTING AND BUYING INSURANCE

- Most insurance contracts are purchased from insurance agents. Insurance agents represent insurance companies and sell insurance to individuals and businesses. Some agents represent several different insurance companies and can provide many types of insurance for a business. Other agents represent only one company and sell only the policies offered by that company. Most communities have agents offering all types of insurance. However, there may be differences in the policies and services offered by different insurance companies and agents. A businessperson should discuss insurance needs with two or three agents before selecting a company and the type and amount of insurance. It is often not the best business practice to select an agent just because he or she is able to offer the lowest rates. The service another agent and company provide if a loss occurs may more than make up for slightly higher insurance premiums. The Figure below describes important factors to consider when choosing an insurance company and an agent.

The primary objectives when purchasing insurance are to get the proper coverage of risks at a reasonable cost and to make certain that the insurance company will pay the claim and provide needed services in the event of loss. For example, a business that needs fire insurance wants to be sure that the insurance company that issues the policy will pay a claim promptly so that business activities will not be interrupted longer than necessary. A business that buys liability insurance wants to be sure that if a person is injured, the insurance company will help determine the business’s responsibility and make a fair settlement with the injured person. Business owners should consider the areas where major losses could occur when planning the purchase of insurance.

A business may obtain various types of insurance to fit its needs in protecting its property. The major types of property insurance that a business might have are (1) fire insurance, (2) burglary and robbery insurance, (3) business income insurance, (4) transportation insurance, and (5) vehicle insurance.

Fire insurance provides funds to replace such items as buildings, furniture, machinery, raw materials, and inventory damaged or destroyed by fire. Fire insurance on a building may not cover the equipment, machinery, and materials in the building. Separate policies may be required to protect the building’s contents from fire loss. The owners of a building should obtain insurance to protect their investment. The occupants of a rented building should look into insurance to protect their property inside the building. You should know exactly what the policy covers when buying fire insurance. Some basic fire insurance policies may be extended to cover additional What types of businesses might seek insurance against robberies? risks, such as wind, hail, and hurricanes. Additional protection beyond the primary peril is called extended coverage. It is obtained by paying an additional premium and adding a special clause to the insurance contract. Because extended coverage costs more, businesses generally buy it only if the additional perils are fairly common in their area. For example, West Coast businesses in the United States may buy earthquake insurance because earthquakes occur there, but businesses in the Southeast usually do not need this coverage. In some areas of the country, insurance companies will not sell extended coverage for some perils because the chance of loss is too high. For example, insurance companies are not willing to sell flood insurance to cover homes built in an area close to rivers or along coasts where flooding regularly occurs. Because of that, the federal government manages the National Flood Insurance Program (NFIP). The flood insurance program follows strict regulations and provides standard policies through approved insurance companies.

Burglary and robbery insurance provides protection from loss resulting from the theft of money, inventory, and other business assets. Because of the differences in types of businesses and operating methods, the risks vary considerably, as do premium rates. Burglary and robbery insurance does not cover the loss of products and equipment taken by employees or shoplifted merchandise. Separate insurance is available to cover these losses, but it is often very expensive. Businesses usually spend a great deal on security equipment and training to prevent these losses. However, they may purchase insurance as well to protect against unusually large losses.

Business income insurance (also known as business interruption insurance) is designed to compensate firms for loss of income during the time required to restore damaged property. For instance, after a hurricane, a damaged store suffers an additional loss because it cannot earn an income until its facilities are restored and it can start selling merchandise again. Some of its expenses may continue even though the business cannot operate, such as interest on loans, taxes, rent, insurance payments, advertising, and salaries.

Transportation insurance protects against damage, theft, or complete loss of goods while being shipped. Although the transportation company may be responsible for many losses during shipment, some losses may be the responsibility of the seller or buyer. The seller can purchase insurance, or the transportation company may provide insurance as part of the cost of transportation. Anytime businesses ship products, they should find out if the goods are insured and who is paying the cost of the insurance.

Many businesses own a large number of vehicles, including cars, trucks, and specialty equipment. Several different kinds of vehicle insurance are needed for protection against theft, property damage, and personal injury. Collision insurance provides protection against damage to the insured’s own vehicle when it is in a collision with another car or object. Comprehensive insurance, included in many basic vehicle policies, covers loss caused by something other than collisions, such as rocks hitting a windshield, fire, theft, storm damage, and vandalism. Vehicle liability insurance provides protection against damage caused by the insured’s vehicle to other people or their property. Most states require all vehicle owners to carry a minimum amount of liability insurance. Medical payments insurance covers medical, hospital, and related expenses caused by injuries to any occupant of the vehicle. These payments are made regardless of the legal liability of the policyholder. Normally, the insurance company of the person responsible for an accident must pay the costs of damages. However, some states have passed no-fault insurance laws. Under no-fault insurance, each insurance company is required to pay the losses of its insured when an accident occurs, regardless of who was responsible for the accident. The intent of no-fault insurance is to reduce automobile insurance costs that result from legal actions taken to determine fault and obtain payment for losses.

2. INSURING PEOPLE

- People are important to the success of all businesses. Owners and managers, employees, people working for suppliers or other businesses, and customers influence the financial success of the business. There are economic risks that involve all these people. Insurance is available to protect businesses from those risks. The primary types of insurance related to employees are health, disability, life, and liability insurance, as well as employee bonding.

- Health insurance provides protection against the expenses of individual health care. Typically, businesses offer three categories of coverage to their employees: (1) medical payments, (2) major medical, and (3) disability. Medical payments insurance covers normal health care and treatment costs. Major medical insurance provides additional coverage for more critical illnesses or treatments that are particularly extensive and expensive.

- Disability insurance offers payments to employees who are not able to work because of accidents or illnesses. Insurance companies typically do not pay disability claims unless the injured employee is unable to perform any work for the company over a period of time. Then it usually pays a portion of the salary the employee was earning before the disability. Recognizing the problems of rapidly rising health care costs and the numbers of uninsured and underinsured individuals, the U.S. Congress passed the Patient Protection and Affordable Care Act (ACA) of 2010. As a result of the ACA, many employers are required to provide health insurance coverage to employees or face fines. Even when health insurance is not provided by an employer, the majority of individuals are required to still possess coverage. Employers providing any assistance to employees seeking health care must ensure that all plans offered or recommended are compliant with the minimal standards of the ACA. Because the health and wellness of employees are important to both the business and the employee, both often share the cost of health insurance. Most medium and large businesses offer a group insurance policy. Under this type of plan, all employees can obtain insurance, regardless of their health, and the cost is typically lower than if they purchased coverage individually. Health insurance has become an important concern for American businesses, individuals, and government. Because of the high costs of medical care, insurance costs have increased to the point that many people and even companies cannot afford them. Businesses, insurance companies, the health care industry, and government continue to study alternatives that can control costs while providing basic coverage to as many people as possible.

- An alternative health insurance plan for employees is a health maintenance organization (HMO). An HMO is a cooperative agreement between a business and a group of physicians and other medical professionals to provide for the health care needs of the business’s employees. The HMO receives a regular payment for each employee that covers an agreed-upon set of medical services. To control services and costs, employees obtain treatment from the health care providers in the HMO. The goal of the HMO is to keep people healthy rather than waiting until they become sick and only then seeking treatment. Some people prefer to receive health care services from a physician and hospital they select rather than from the assigned health care practitioners in an HMO. To fill this need, insurance companies offer another alternative: the preferred provider organization (PPO). A PPO is an agreement among insurers, health care providers, and businesses that allows employees to choose from a list of physicians and health care facilities. The insurance company negotiates with a number of physicians and hospitals for a full range of health care services. The contracts establish the costs that the insurer will pay for those services to control costs while still offering consumers a choice of providers.

- Another common form of insurance for people is life insurance. Life insurance pays money upon the death of the insured. The person or persons identified in the insurance policy to whom the payment is made upon the death of the insured are beneficiaries. With life insurance, individuals can provide some financial protection for their families in the event of their death. Some companies provide a specific amount of life insurance as a standard part of employee benefits. Others offer the opportunity for employees to purchase life insurance at a favorable rate, but the employees must pay most or all of the cost. Many businesses insure the lives of owners and top managers because of their importance to the financial success of the business. In the case of sole proprietorships, owners usually find it easier to borrow money if they carry adequate life insurance on themselves because lenders would be paid if the proprietor were to die. Life insurance has an especially important place in partnerships. Generally, a partnership is dissolved upon the death of one partner. Each partner usually carries life insurance on the other partner, so that if one dies, the other will receive, as beneficiary of the insurance policy, sufficient money to buy the other’s share of the business. Life insurance on the owners, top managers, or employees with skills that would be difficult to replace is known as key person life insurance.

3. OTHER BUSINESS INSURANCE NEEDS

- In addition to insuring business operations and people, businesses often buy insurance to cover special types of risk. Two special areas of concern are the risks of business operations and international business activities.

- Businesses face many risks that result from the operation of the business. People may get hurt while on the job, products may cause damage or injury, and employees may do things that damage people or their property. Liability insurance protects against losses from injury to people or their property that result from the products, services, or operations of the business. For example, if a toy injures a child, the child’s family may file a lawsuit or claim against the toy manufacturer. Liability insurance would protect the company in such circumstances. Clients sometimes sue professionals, such as lawyers and physicians, who provide personal services. Malpractice insurance is a type of liability insurance that protects against financial loss arising from suits for negligence in providing professional services. Malpractice claims are a major cost to many professionals. Even if the businessperson is not proven guilty of malpractice, the legal fees can be very high. Some businesses need a special type of insurance protection called bonding. Bonding pays damages to people whose losses are caused by the negligence or dishonesty of an employee or by the failure of a business to complete a contract. Bonding is often required for contractors hired to construct buildings, highways, or bridges, and for companies that transport large sums of money between businesses and financial institutions.

- Many businesses operate or sell products in other countries. Insurance policies typically do not cover losses or liability resulting from international operations. Special coverage may be available at additional cost within existing insurance policies. Businesspeople should keep in mind that the insurance laws of the country in which the business is operating apply to loss situations. To encourage international business with developing countries, the U.S. government formed the Overseas Private Investment Corporation (OPIC). The corporation provides insurance coverage for businesses that suffer losses or damage to foreign investments as the result of political risks. Companies can even purchase insurance that covers losses suffered if the purchasers of exports do not pay for their purchases. Although coverage is expensive, companies that are beginning to engage in international trade or that have not previously worked with a specific international company may want to consider such insurance. Businesses shipping products to other countries should also obtain special transportation insurance, because several different companies and transportation methods may be involved as the products move from country to country.

Последнее изменение: вторник, 14 августа 2018, 08:30