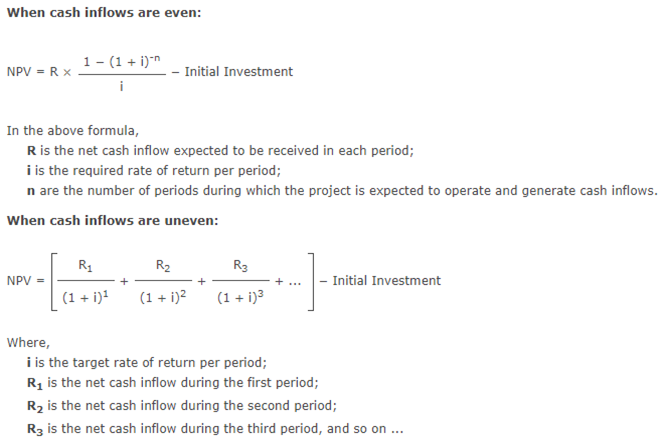

Reading: Net Present Value

Net

Present Value

•The

first step involved in the calculation of NPV is the estimation of net cash

flows from the project over its life. The second step is to discount those cash

flows at the hurdle rate.

•

•The

net cash flows may be even (i.e. equal cash flows in different periods) or

uneven (i.e. different cash flows in different periods). When they are even,

present value can be easily calculated by using the formula for present value

of annuity. However, if they are uneven, we need to calculate the present value

of each individual net cash inflow separately.

•

•Once

we have the total present value of all project cash flows, we subtract the

initial investment on the project from the total present value of inflows to

arrive at net present value.

•Decision

Rule

- In case of standalone projects, accept a project only if its NPV is positive, reject it if its NPV is negative and stay indifferent between accepting or rejecting if NPV is zero.

- In case of mutually exclusive projects (i.e. competing projects), accept the project with higher NPV.

- In case of standalone projects, accept a project only if its NPV is positive, reject it if its NPV is negative and stay indifferent between accepting or rejecting if NPV is zero.

- In case of mutually exclusive projects (i.e. competing projects), accept the project with higher NPV.

Net

Present Value Example

Net

Present Value Example

.

Example 1: Even Cash Inflows: Calculate the net present value of a project which requires an initial investment of $243,000 and it is expected to generate a cash inflow of $50,000 each month for 12 months. Assume that the salvage value of the project is zero. The target rate of return is 12% per annum.

Solution

We have,

Initial Investment = $243,000

Net Cash Inflow per Period = $50,000

Number of Periods = 12

Discount Rate per Period = 12% ÷ 12 = 1%

Net Present Value

= $50,000 × (1 − (1 + 1%)^-12) ÷ 1% − $243,000

= $50,000 × (1 − 1.01^-12) ÷ 0.01 − $243,000

≈ $50,000 × (1 − 0.887449) ÷ 0.01 − $243,000

≈ $50,000 × 0.112551 ÷ 0.01 − $243,000

≈ $50,000 × 11.2551 − $243,000

≈ $562,754 − $243,000

≈ $319,754

Net

Present Value Example

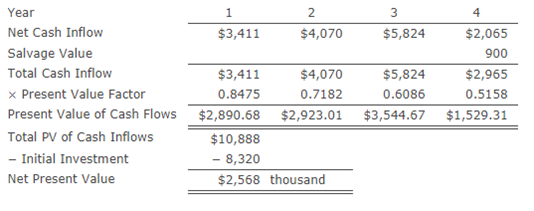

Example 2: Uneven Cash Inflows: An initial investment of $8,320 thousand on plant and machinery is expected to generate cash inflows of $3,411 thousand, $4,070 thousand, $5,824 thousand and $2,065 thousand at the end of first, second, third and fourth year respectively. At the end of the fourth year, the machinery will be sold for $900 thousand. Calculate the net present value of the investment if the discount rate is 18%. Round your answer to nearest thousand dollars.

Solution

PV Factors:

Year 1 = 1 ÷ (1 + 18%)^1 ≈ 0.8475

Year 2 = 1 ÷ (1 + 18%)^2 ≈ 0.7182

Year 3 = 1 ÷ (1 + 18%)^3 ≈ 0.6086

Year 4 = 1 ÷ (1 + 18%)^4 ≈ 0.5158

Net

Present Value Example

Strengths

and Weaknesses of NPV

•Strengths

-Net present value accounts for time value of money which makes it a sounder approach than other investment appraisal techniques which do not discount future cash flows such payback period and accounting rate of return.

-Net present value is even better than some other discounted cash flows techniques such as IRR. In situations where IRR and NPV give conflicting decisions, NPV decision should be preferred.

-Net present value accounts for time value of money which makes it a sounder approach than other investment appraisal techniques which do not discount future cash flows such payback period and accounting rate of return.

-Net present value is even better than some other discounted cash flows techniques such as IRR. In situations where IRR and NPV give conflicting decisions, NPV decision should be preferred.

•Weaknesses

- NPV is after all an estimation. It is sensitive to changes in estimates for future cash flows, salvage value and the cost of capital.

-Net present value does not take into account the size of the project. For example, say Project A requires initial investment of $4 million to generate NPV of $1 million while a competing Project B requires $2 million investment to generate an NPV of $0.8 million. If we base our decision on NPV alone, we will prefer Project A because it has higher NPV, but Project B has generated more shareholders’ wealth per dollar of initial investment ($0.8 million/$2 million vs $1 million/$4 million).

- NPV is after all an estimation. It is sensitive to changes in estimates for future cash flows, salvage value and the cost of capital.

-Net present value does not take into account the size of the project. For example, say Project A requires initial investment of $4 million to generate NPV of $1 million while a competing Project B requires $2 million investment to generate an NPV of $0.8 million. If we base our decision on NPV alone, we will prefer Project A because it has higher NPV, but Project B has generated more shareholders’ wealth per dollar of initial investment ($0.8 million/$2 million vs $1 million/$4 million).

Última modificación: martes, 14 de agosto de 2018, 08:51