Reading: Marginal Revenue and Marginal Cost

Marginal

Revenue and Marginal Cost

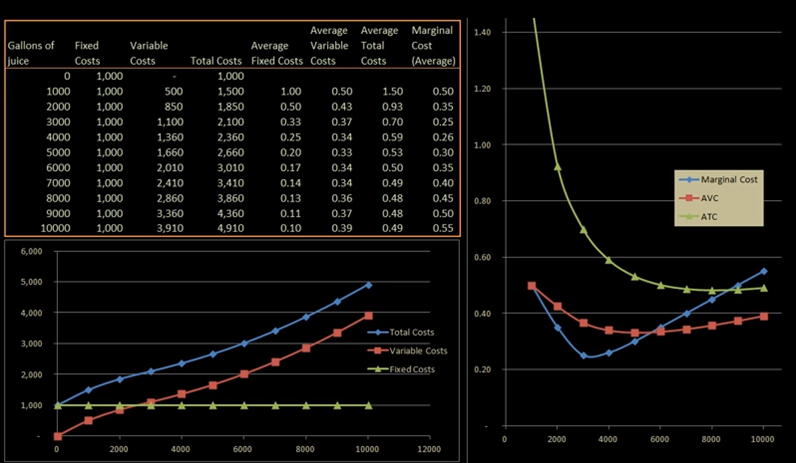

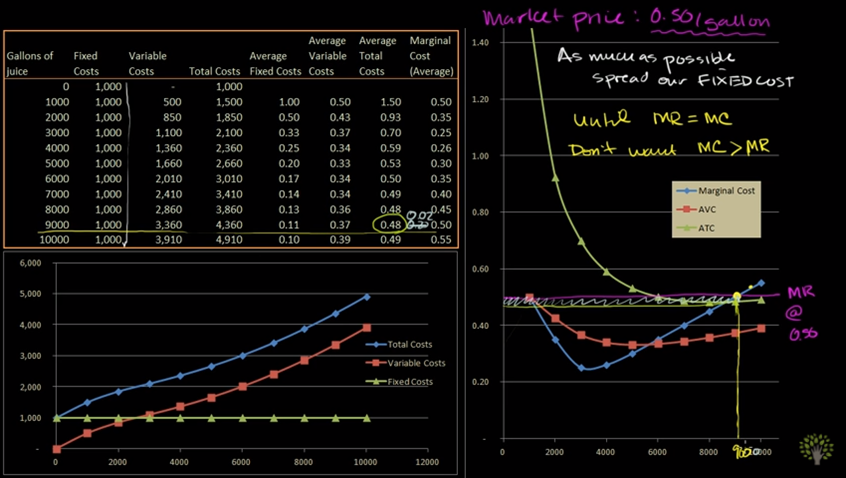

The marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per unit of a product to maximize profits. A rational company always seeks to maximize its profit, and the relationship between marginal revenue and the marginal cost of production helps to find the point at which this occurs. The point at which marginal revenue equals marginal cost maximizes a company's profit.

The marginal cost of production measures the change in total cost of a good that arises from producing one additional unit of that good. The marginal cost is calculated by dividing the change in the total cost by the change in quantity.

For example, the total cost of producing 100 units of a good is $200. The total cost of producing 101 units is $204. The average cost of producing 100 units is $2, or $200/100; however, the marginal cost for producing the 101st unit is $4, or ($204 - $200)/(101-100).

The marginal revenue measures

the change in the revenue that arises when one additional unit of a product is

sold. The marginal revenue is calculated by dividing the change in the total

revenue by the change in the quantity.

For example, suppose the price of a product is $10 and a company produces 20 units per day. The total revenue is calculated by multiplying the price by the quantity produced. In this case, the total revenue is $200, or $10*20. The total revenue from producing 21 units is $205. The marginal revenue is calculated as $5, or ($205 - $200)/(21-20).

When marginal revenue and the marginal cost of production is equal, profit is maximized at that level of output and price.

For example, a toy company can sell 15 toys at $10 each. However, if the company sells 16 units, the selling price falls to $9.50 each. The marginal revenue is $2, or ((16*9.50)-(15*10))/(16-15). Suppose the marginal cost is $2; the company maximizes its profit at this point because the marginal revenue is equal to its marginal cost.

When marginal revenue is less than the marginal cost of production, a company is producing too much and should decrease its quantity supplied until marginal revenue equals the marginal cost of production. When the marginal revenue is greater than the marginal cost, the firm is not producing enough goods and should increase its output until profit is maximized.

Last modified: Tuesday, August 14, 2018, 10:10 AM