Reading: Lesson 5 - The Accounts - Debits and Credits

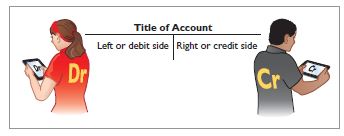

The Account

The account represents an individual accounting record with increases and decreases within the assets, liabilities, and the owner's equity. The account has three parts: (1) a title, (2) a left or debit side, and (3) a right or credit side. The Format of the account looks like the letter T, it is referred to as the T-account.

Debits and Credits

The left side of the account is referred to as a debit and the right side of the account is referred to as a credit. The abbreviation for debit is Dr. and credit is Cr. They do not represent an increase or a decrease. The terms debit and credit are used in the recording process to determine where the entries are placed within the account. The term debiting is referred to when an amount is entered on the left side of the account. Crediting is the term used when entries are made on the left side of the account.

An account will show a debit balance if the debit balance exceeds the credit balance. The account will have a credit balance if the credit balance exceeds the debit balance.

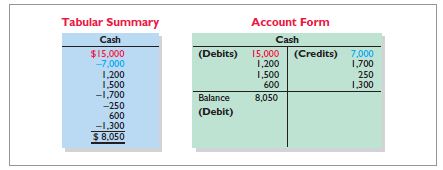

The illustration below shows a Tabular Summary and Account Form for a Cash Account.

The positive figures in the tabular summary represent an addition to the cash account. All of the negative figures represent a deduction from the cash account.

Recording the increases on one side and the decreases on the other side will help in reducing errors. It will help determine the totals of each side of the account as well as the account balance.

The balance of the account will be determined by netting the two sides together. The account had a debit balance of $8,050 indicating that the owner had more increases than decreases in cash.

DEBIT AND CREDIT PROCEDURE

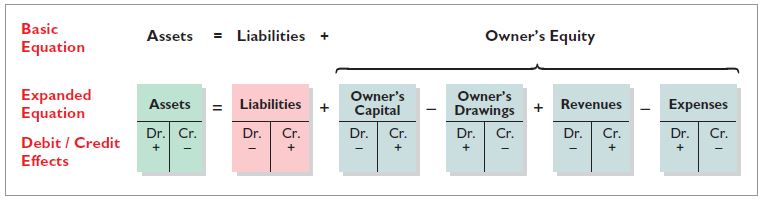

In order for the accounting equation to remain in balance, each transaction must affect at least two or more accounts. The debits and credits of each transaction must equal. This process represents the double-entry system. This system provides a method of recording transactions, helps ensure the accuracy of the recorded amounts and the detection of errors.

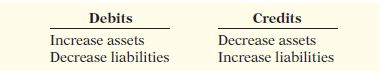

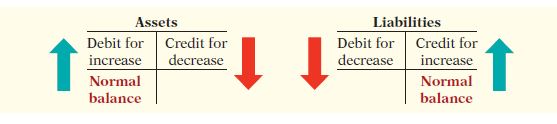

Debits increase assets and decrease liabilities. Credits decrease assets and increase liabilities.

The side of the account where there is an increase is called the normal balance. Assets have a debit balance as their normal balance. Liabilities have a credit balance.

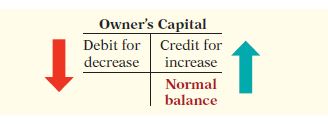

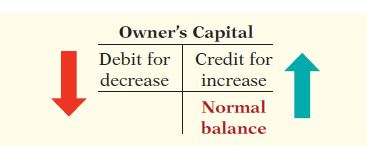

When an owner makes an investment in their business, it is credited to Owner's Capital. Debits will decrease the owners capital. The Owner's Capital account has a credit as a normal account balance.

When the owner's make withdrawals from the business, whether it be cash or another type of asset, they are recorded in the Owner's Drawing account. The normal balance for this account is a debit balance. Withdrawals can be made in the Capital account; however, using the Drawing account makes it easier to determine the number of total withdrawals for a certain period of time.

Revenue is the income that a business earns from sales of goods and services. Expenses are the cost incurred by the business. The effect that the debits and credits have on the revenue account is the same as the effect on the Owner's Capital accounts. Expense will have the opposite effect. The revenue account carries a credit balance as its normal balance. The expenses carry a debit balance as its normal balance.

Below represents the summary of the debit and credit rules and the effects on each of the type of accounts.

Остання зміна: вівторок 28 травня 2019 12:04 PM