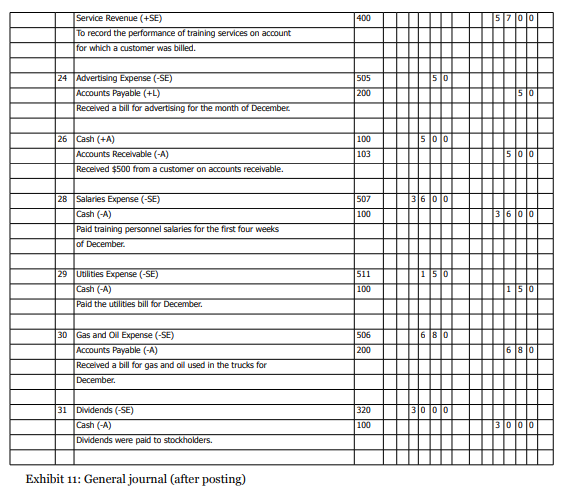

Reading: Lesson 7 - The use of ledger accounts

A journal entry is like a set of instructions. The carrying out of these instructions is known as

posting. As stated earlier, posting is recording in the ledger accounts the information contained in the

journal. A journal entry directs the entry of a certain dollar amount as a debit in a specific ledger

account and directs the entry of a certain dollar amount as a credit in a specific ledger account. Earlier,

we posted the journal entries for MicroTrain Company to T-accounts. In practice, however, companies

post these journal entries to ledger accounts.

Using a new example, Jenks Company, we illustrate posting to ledger accounts. Later, we show you

how to post the MicroTrain Company journal entries to ledger accounts.

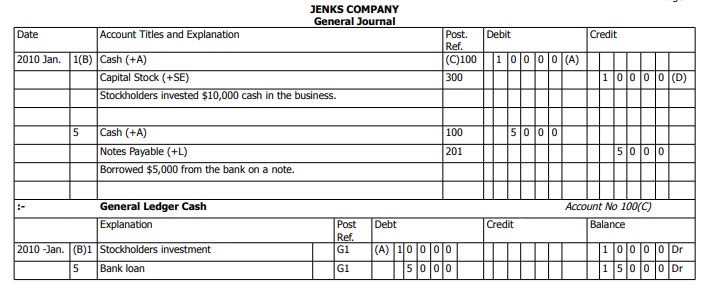

In Exhibit 10, the first journal entry for the Jenks Company directs that USD 10,000 be posted in

the ledger as a debit to the Cash account and as a credit to the Capital Stock account. We post the debit

in the general ledger Cash account by using the following procedure: Enter in the Cash account the

date, a short explanation, the journal designation ("G" for general journal) and the journal page

number from which the debit is posted, and the USD 10,000 in the Debit column. Then, enter the

number of the account to which the debit is posted in the Posting Reference column of the general

journal. Post the credit in a similar manner but as a credit to Account No. 300. The arrows in Exhibit

10 show how these amounts were posted to the correct accounts.

Exhibit 10 shows the ledger account. In contrast to the two-sided T-account format shown so far,

the three-column format has columns for debit, credit, and balance. The three-column form has the advantage of showing the balance of the account after each item has been posted. In addition, in this

chapter, we indicate whether each balance is a debit or a credit. In later chapters and in practice, the

nature of the balance is usually not indicated since it is understood. Also, notice that we give an

explanation for each item in the ledger accounts. Often accountants omit these explanations because

each item can be traced back to the general journal for the explanation.

Posting is always from the journal to the ledger accounts. Postings can be made (1) at the time the

transaction is journalized; (2) at the end of the day, week, or month; or (3) as each journal page is

filled. The choice is a matter of personal taste. When posting the general journal, the date used in the

ledger accounts is the date the transaction was recorded in the journal, not the date the journal entry

was posted to the ledger accounts.

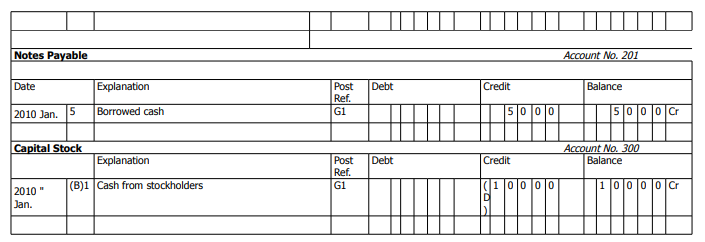

Frequently, accountants must check and trace the origin of their transactions, so they provide crossindexing.

Cross-indexing is the placing of (1) the account number of the ledger account in the

general journal and (2) the general journal page number in the ledger account. As shown in Exhibit 10,

the account number of the ledger account to which the posting was made is in the Posting Reference

column of the general journal. Note the arrow from Account No. 100 in the ledger to the 100 in the

Posting Reference column beside the first debit in the general journal. Accountants place the number

of the general journal page from which the entry was posted in the Posting Reference column of the

ledger account. Note the arrow from page 1 in Exhibit 10 the general journal to G1 in the Posting

Reference column of the Cash account in the general ledger. The notation "G1" means general journal,

page 1. The date of the transaction also appears in the general ledger. Note the arrows from the date in

the general journal to the dates in the general ledger.

Exhibit 10: General journal and general ledger; posting and cross-indexing

Cross-indexing aids the tracing of any recorded transaction, either from general journal to general

ledger or from general ledger to general journal. Normally, they place cross-reference numbers in the

Posting Reference column of the general journal when the entry is posted. If this practice is followed,

the cross-reference numbers indicate that the entry has been posted.

To understand the posting and cross-indexing process, trace the entries from the general journal to

the general ledger. The ledger accounts need not contain explanations of all the entries, since any

needed explanations can be obtained from the general journal.

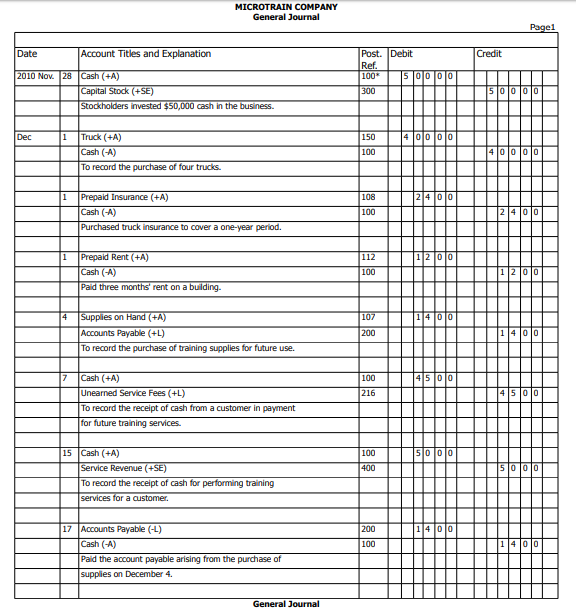

Look at Exhibit 11 to see how all the November and December transactions of MicroTrain Company

would be journalized. As shown in Exhibit 11, you skip a line between journal entries to show where

one journal entry ends and another begins. This procedure is standard practice among accountants.

Note that no dollar signs appear in journals or ledgers. When amounts are in even dollar amounts,

accountants leave the cents column blank or use zeros or a dash. When they use lined accounting work papers, commas or decimal points are not needed to record an amount. When they use unlined paper,

they add both commas and decimal points.

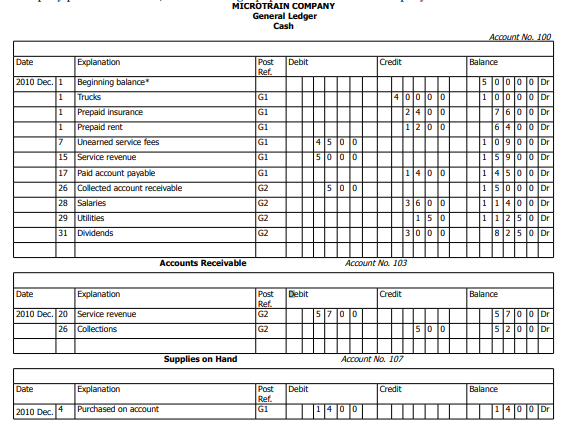

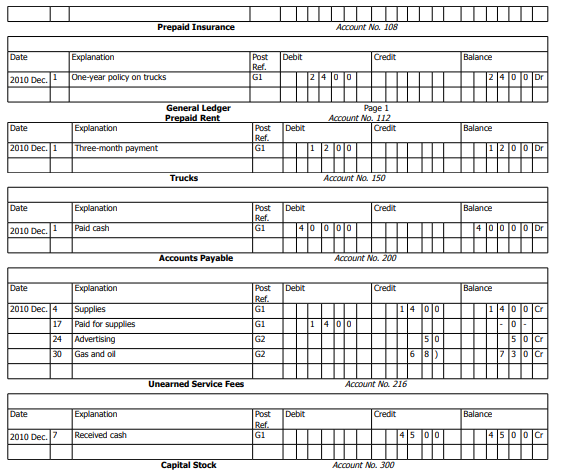

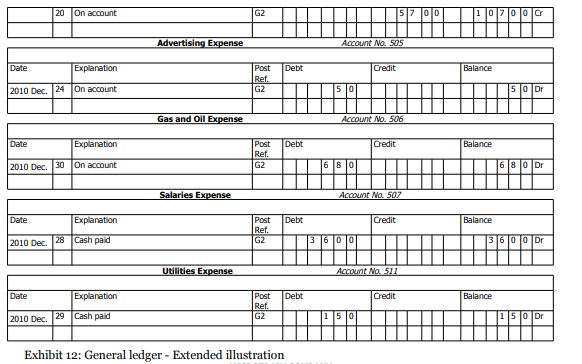

Next, observe Exhibit 12, the three-column general ledger accounts of MicroTrain Company after

the journal entries have been posted. Each ledger account would appear on a separate page in the

ledger. Trace the postings from the general journal to the general ledger to make sure you know how to

post journal entries.

All the journal entries illustrated so far have involved one debit and one credit; these journal entries

are called simple journal entries. Many business transactions, however, affect more than two

accounts. The journal entry for these transactions involves more than one debit and/or credit. Such

journal entries are called compound journal entries.

As an illustration of a compound journal entry, assume that on 2011 January 2, MicroTrain

Company purchased USD 8,000 of training equipment from Wilson Company. See below.

MicroTrain paid USD 2,000 cash with the balance due on 2011 March 3. The general journal entry

for MicroTrain Company is:

Note that the firm credits two accounts, Cash and Accounts Payable, in this one entry. However, the

dollar totals of the debits and credits are equal.

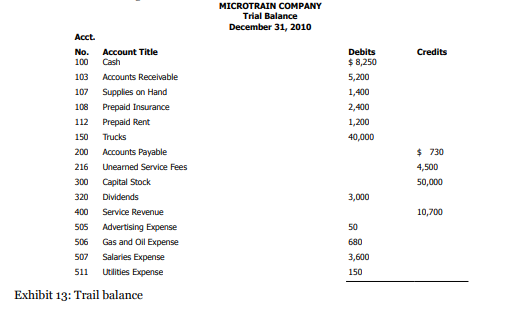

Periodically, accountants use a trial balance to test the equality of their debits and credits. A trial

balance is a listing of the ledger accounts and their debit or credit balances to determine that debits

equal credits in the recording process. The accounts appear in this order: assets, liabilities,

stockholders' equity, dividends, revenues, and expenses. Within the assets category, the most liquid

(closest to becoming cash) asset appears first and the least liquid appears last. Within the liabilities,

those liabilities with the shortest maturities appear first. Study Exhibit 13, the trial balance for

MicroTrain Company. Note the listing of the account numbers and account titles on the left, the

column for debit balances, the column for credit balances, and the equality of the two totals.

When the trial balance does not balance, try re-totaling the two columns. If this step does not locate

the error, divide the difference in the totals by 2 and then by 9. If the difference is divisible by 2, you

may have transferred a debit-balanced account to the trial balance as a credit, or a credit-balanced

account as a debit. When the difference is divisible by 2, look for an amount in the trial balance that is

equal to one-half of the difference. Thus, if the difference is USD 800, look for an account with a

balance of USD 400 and see if it is in the wrong column.

If the difference is divisible by 9, you may have made a transposition error in transferring a balance

to the trial balance or a slide error. A transposition error occurs when two digits are reversed in an

amount (e.g. writing 753 as 573 or 110 as 101). A slide error occurs when you place a decimal point

incorrectly (e.g. USD 1,500 recorded as USD 15.00). Thus, when a difference is divisible by 9, compare

the trial balance amounts with the general ledger account balances to see if you made a transposition

or slide error in transferring the amounts.

If you still cannot find the error, it may be due to one of the following causes:

- Failing to post part of a journal entry.

- Posting a debit as a credit, or vice versa.

- Incorrectly determining the balance of an account.

- Recording the balance of an account incorrectly in the trial balance.

- Omitting an account from the trial balance.

- Making a transposition or slide error in the accounts or the journal.

Usually, you should work backward through the steps taken to prepare the trial balance. Assuming

you have already re-totaled the columns and traced the amounts appearing in the trial balance back to

the general ledger account balances, use the following steps: Verify the balance of each general ledger

account, verify postings to the general ledger, verify general journal entries, and then review the

transactions and possibly the source documents.

The equality of the two totals in the trial balance does not necessarily mean that the accounting

process has been error-free. Serious errors may have been made, such as failure to record a

transaction, or posting a debit or credit to the wrong account. For instance, if a transaction involving

payment of a USD 100 account payable is never recorded, the trial balance totals still balance, but at an

amount that is USD 100 too high. Both cash and accounts payable would be overstated by USD 100.

You can prepare a trial balance at any time—at the end of a day, a week, a month, a quarter, or a year. Typically, you would prepare a trial balance before preparing the financial statements.

Last modified: Tuesday, May 28, 2019, 12:09 PM