Reading: Lesson 5 - Adjustments for deferred items

This section discusses the two types of adjustments for deferred items: asset/expense adjustments

and liability/revenue adjustments. In the asset/expense group, you learn how to prepare adjusting

entries for prepaid expenses and depreciation. In the liability/revenue group, you learn how to prepare

adjusting entries for unearned revenues.

MicroTrain Company must make several asset/expense adjustments for prepaid expenses. A

prepaid expense is an asset awaiting assignment to expense, such as prepaid insurance, prepaid

rent, and supplies on hand. Note that the nature of these three adjustments is the same.

Prepaid insurance When a company pays an insurance policy premium in advance, the purchase

creates the asset, prepaid insurance. This advance payment is an asset because the company will receive insurance coverage in the future. With the passage of time, however, the asset gradually

expires. The portion that has expired becomes an expense. To illustrate this point, recall that in

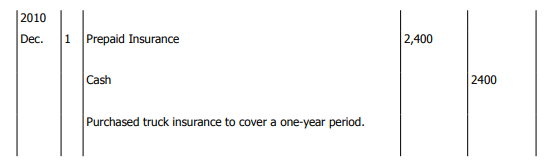

Chapter 2, MicroTrain Company purchased for cash an insurance policy on its trucks for the period

2010 December 1, to 2011 November 30. The journal entry made on 2010 December 1, to record the

purchase of the policy was:

The two accounts relating to insurance are Prepaid Insurance (an asset) and Insurance Expense (an

expense). After posting this entry, the Prepaid Insurance account has a USD 2,400 debit balance on

2010 December 1. The Insurance Expense account has a zero balance on 2010 December 1, because no

time has elapsed to use any of the policy’s benefits.

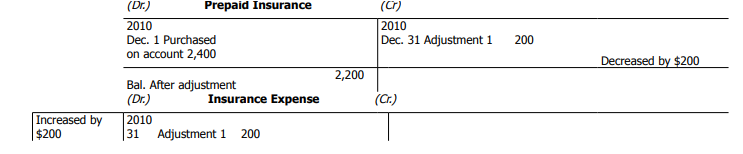

By 2010 December 31, one month of the year covered by the policy has expired. Therefore, part of

the service potential (or benefit obtained from the asset) has expired. The asset now provides less

future services or benefits than when the company acquired it. We recognize this reduction by treating

the cost of the services received from the asset as an expense. For the MicroTrain Company example,

the service received was one month of insurance coverage. Since the policy provides the same services

for every month of its one-year life, we assign an equal amount (USD 200) of cost to each month. Thus,

MicroTrain charges 1/12 of the annual premium to Insurance Expense on 2010 December 31. The

adjusting journal entry is:

After posting these two journal entries, the accounts in T-account format appear as follows:

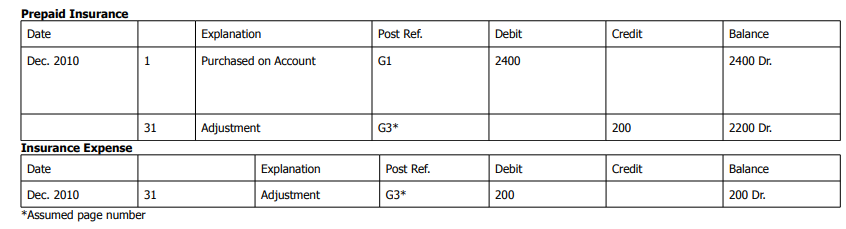

In practice, accountants do not use T-accounts. Instead, they use three-column ledger accounts that

have the advantage of showing a balance after each transaction. After posting the preceding two

entries, the three-column ledger accounts appear as follows:

Before this adjusting entry was made, the entire USD 2,400 insurance payment made on 2010

December 1, was a prepaid expense for 12 months of protection. So on 2010 December 31, one month

of protection had passed, and an adjusting entry transferred USD 200 of the USD 2,400 (USD

2,400/12 = USD 200) to Insurance Expense. On the income statement for the year ended 2010

December 31, MicroTrain reports one month of insurance expense, USD 200, as one of the expenses it

incurred in generating that year’s revenues. It reports the remaining amount of the prepaid expense,

USD 2,200, as an asset on the balance sheet. The USD 2,200 prepaid expense represents 11 months of

insurance protection that remains as a future benefit.

Prepaid rent Prepaid rent is another example of the gradual consumption of a previously

recorded asset. Assume a company pays rent in advance to cover more than one accounting period. On the date it pays the rent, the company debits the prepayment to the Prepaid Rent account (an asset

account). The company has not yet received benefits resulting from this expenditure. Thus, the

expenditure creates an asset.

We measure rent expense similarly to insurance expense. Generally, the rental contract specifies the

amount of rent per unit of time. If the prepayment covers a three-month rental, we charge one-third of

this rental to each month. Notice that the amount charged is the same each month even though some

months have more days than other months.

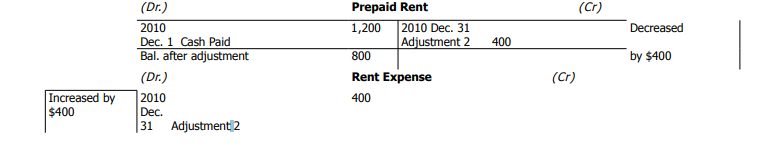

For example, MicroTrain Company paid USD 1,200 rent in advance on 2010 December 28, to cover

a three-month period beginning on that date. The journal entry would be:

The two accounts relating to rent are Prepaid Rent (an asset) and Rent Expense. After this entry is

posted, the Prepaid Rent account has a USD 1,200 balance and the Rent Expense account has a zero

balance because no part of the rent period has yet elapsed.

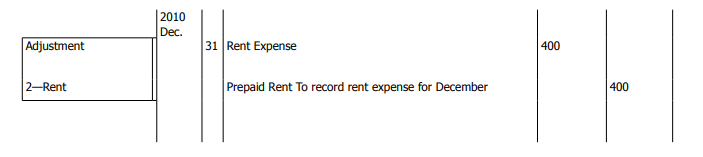

On 2010 December 31, MicroTrain must prepare an adjusting entry. Since one third of the period

covered by the prepaid rent has elapsed, it charges one-third of the USD 1,200 of prepaid rent to

expense. The required adjusting entry is:

After posting this adjusting entry, the T-accounts appear as follows:

The USD 400 rent expense appears in the income statement for the year ended 2010 December 31.

MicroTrain reports the remaining USD 800 of prepaid rent as an asset in the balance sheet on 2010

December 31. Thus, the adjusting entries have accomplished their purpose of maintaining the accuracy

of the financial statements.

Supplies on hand Almost every business uses supplies in its operations. It may classify supplies

simply as supplies (to include all types of supplies), or more specifically as office supplies (paper,

stationery, floppy diskettes, pencils), selling supplies (gummed tape, string, paper bags, cartons,

wrapping paper), or training supplies (transparencies, training manuals). Frequently, companies buy

supplies in bulk. These supplies are an asset until the company uses them. This asset may be called

supplies on hand or supplies inventory. Even though these terms indicate a prepaid expense, the firm

does not use prepaid in the asset’s title.

On 2010 December 4, MicroTrain Company purchased supplies for USD 1,400 and recorded the

transaction as follows:

MicroTrain’s two accounts relating to supplies are Supplies on Hand (an asset) and Supplies

Expense. After this entry is posted, the Supplies on Hand account shows a debit balance of USD 1,400

and the Supplies Expense account has a zero balance as shown in the following T-accounts:

An actual physical inventory (a count of the supplies on hand) at the end of the month showed only

USD 900 of supplies on hand. Thus, the company must have used USD 500 of supplies in December.

An adjusting journal entry brings the two accounts pertaining to supplies to their proper balances. The

adjusting entry recognizes the reduction in the asset (Supplies on Hand) and the recording of an

expense (Supplies Expense) by transferring USD 500 from the asset to the expense. According to the

physical inventory, the asset balance should be USD 900 and the expense balance, USD 500. So

MicroTrain makes the following adjusting entry:

After posting this adjusting entry, the T-accounts appear as follows:

The entry to record the use of supplies could be made when the supplies are issued from the

storeroom. However, such careful accounting for small items each time they are issued is usually too

costly a procedure.

Accountants make adjusting entries for supplies on hand, like for any other prepaid expense, before

preparing financial statements. Supplies expense appears in the income statement. Supplies on hand is

an asset in the balance sheet.

Sometimes companies buy assets relating to insurance, rent, and supplies knowing that they will

use them up before the end of the current accounting period (usually one month or one year). If so, an

expense account is usually debited at the time of purchase rather than debiting an asset account. This

procedure avoids having to make an adjusting entry at the end of the accounting period. Sometimes,

too, a company debits an expense even though the asset will benefit more than the current period.

Then, at the end of the accounting period, the firm’s adjusting entry transfers some of the cost from the

expense to the asset. For instance, assume that on January 1, a company paid USD 1,200 rent to cover

a three-year period and debited the USD 1,200 to Rent Expense. At the end of the year, it transfers

USD 800 from Rent Expense to Prepaid Rent. To simplify our approach, we will consistently debit the

asset when the asset will benefit more than the current accounting period.

Depreciation Just as prepaid insurance and prepaid rent indicate a gradual using up of a

previously recorded asset, so does depreciation. However, the overall time involved in using up a

depreciable asset (such as a building) is much longer and less definite than for prepaid expenses. Also,

a prepaid expense generally involves a fairly small amount of money. Depreciable assets, however,

usually involve larger sums of money.

A depreciable asset is a manufactured asset such as a building, machine, vehicle, or piece of

equipment that provides service to a business. In time, these assets lose their utility because of (1) wear

and tear from use or (2) obsolescence due to technological change. Since companies gradually use up

these assets over time, they record depreciation expense on them. Depreciation expense is the

amount of asset cost assigned as an expense to a particular period. The process of recording

depreciation expense is called depreciation accounting. The three factors involved in computing

depreciation expense are:

- Asset cost. The asset cost is the amount that a company paid to purchase the depreciable asset.

- Estimated residual value. The estimated residual value (scrap value) is the amount

that the company can probably sell the asset for at the end of its estimated useful life.

- Estimated useful life. The estimated useful life of an asset is the estimated time that a

company can use the asset. Useful life is an estimate, not an exact measurement, that a company

must make in advance. However, sometimes the useful life is determined by company policy (e.g.

keep a fleet of automobiles for three years).

Accountants use different methods for recording depreciation. The method illustrated here is the

straight-line method. We discuss other depreciation methods in Chapter 10. Straight-line depreciation

assigns the same amount of depreciation expense to each accounting period over the life of the asset.

The depreciation formula (straight-line) to compute straight-line depreciation for a one-year

period is:

![]()

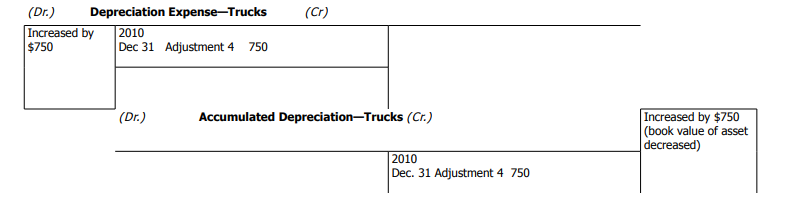

To illustrate the use of this formula, recall that on December 1, MicroTrain Company purchased

four small trucks at a cost of USD 40,000. The journal entry was:

The estimated residual value for each truck was USD 1,000, so MicroTrain estimated the total

residual value for all four trucks at USD 4,000. The company estimated the useful life of each truck to

be four years. Using the straight-line depreciation formula, MicroTrain calculated the annual

depreciation on the trucks as follows:

The amount of depreciation expense for one month would be 1/12 of the annual amount. Thus,

depreciation expense for December is USD 9,000 ÷ 12 = USD 750.

The difference between an asset’s cost and its estimated residual value is an asset’s depreciable

amount. To satisfy the matching principle, the firm must allocate the depreciable amount as an

expense to the various periods in the asset’s useful life. It does this by debiting the amount of

depreciation for a period to a depreciation expense account and crediting the amount to an

accumulated depreciation account. MicroTrain’s depreciation on its delivery trucks for December is

USD 750. The company records the depreciation as follows:

After posting the adjusting entry, the T-accounts appear as follow:

MicroTrain reports depreciation expense in its income statement. And it reports accumulated

depreciation in the balance sheet as a deduction from the related asset.

The accumulated depreciation account is a contra asset account that shows the total of all

depreciation recorded on the asset from the date of acquisition up through the balance sheet date. A

contra asset account is a deduction from the asset to which it relates in the balance sheet. The

purpose of a contra asset account is to reduce the original cost of the asset down to its remaining

undepreciated cost or book value. The accumulated depreciation account does not represent cash that

is being set aside to replace the worn out asset. The undepreciated cost of the asset is the debit balance

in the asset account (original cost) minus the credit balance in the accumulated depreciation contra

account. Accountants also refer to an asset’s cost less accumulated depreciation as the book value (or

net book value) of the asset. Thus, book value is the cost not yet allocated to an expense. In the

previous example, the book value of the equipment after the first month is:

As you may expect, the accumulated depreciation account balance increases each period by the

amount of depreciation expense recorded until the remaining book value of the asset equals the

estimated residual value.

A liability/revenue adjustment involving unearned revenues covers situations in which a customer

has transferred assets, usually cash, to the selling company before the receipt of merchandise or

services. Receiving assets before they are earned creates a liability called unearned revenue. The

firm debits such receipts to the asset account Cash and credits a liability account. The liability account

credited may be Unearned Fees, Revenue Received in Advance, Advances by Customers, or some

similar title. The seller must either provide the services or return the customer’s money. By performing

the services, the company earns revenue and cancels the liability.

Companies receive advance payments for many items, such as training services, delivery services,

tickets, and magazine or newspaper subscriptions. Although we illustrate and discuss only advanced

receipt of training fees, firms treat the other items similarly.

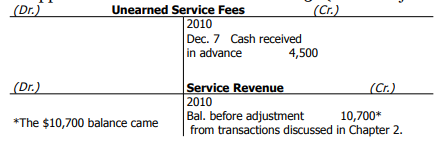

Unearned service fees On December 7, MicroTrain Company received USD 4,500 from a

customer in payment for future training services. The firm recorded the following journal entry:

The two T-accounts relating to training fees are Unearned Service Fees (a liability) and Service

Revenue. These accounts appear as follows on 2010 December 31 (before adjustment):

The balance in the Unearned Service Fees liability account established when MicroTrain received

the cash will be converted into revenue as the company performs the training services. Before

MicroTrain prepares its financial statements, it must make an adjusting entry to transfer the amount of

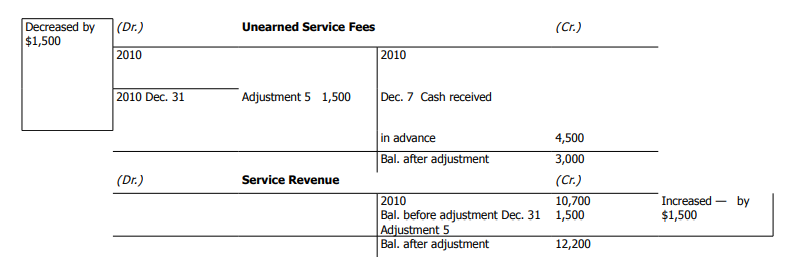

the services performed by the company from a liability account to a revenue account. If we assume that MicroTrain earned one-third of the USD 4,500 in the Unearned Service Fees account by December 31,

then the company transfers USD 1,500 to the Service Revenue account as follows:

After posting the adjusting entry, the T-accounts would appear as follows:

MicroTrain reports the service revenue in its income statement for 2010. The company reports the

USD 3,000 balance in the Unearned Service Fees account as a liability in the balance sheet. In 2011,

the company will likely earn the USD 3,000 and transfer it to a revenue account.

If MicroTrain does not perform the training services, the company would have to refund the money

to the training service customers. For instance, assume that MicroTrain could not perform the

remaining USD 3,000 of training services and would have to refund the money. Then, the company

would make the following entry:

Thus, the company must either perform the training services or refund the fees. This fact should

strengthen your understanding that unearned service fees and similar items are liabilities.

Accountants make the adjusting entries for deferred items for data already recorded in a company’s

asset and liability accounts. They also make adjusting entries for accrued items, which we discuss in

the next section, for business data not yet recorded in the accounting records.

Остання зміна: вівторок 28 травня 2019 12:10 PM