Reading: Lesson 6 - Adjustments for accrued items

Accrued items require two types of adjusting entries: asset/revenue adjustments and

liability/expense adjustments. The first group—asset/revenue adjustments—involves accrued assets;

the second group—liability/expense adjustments—involves accrued liabilities.

Accrued assets are assets, such as interest receivable or accounts receivable, that have not been

recorded by the end of an accounting period. These assets represent rights to receive future payments

that are not due at the balance sheet date. To present an accurate picture of the affairs of the business

on the balance sheet, firms recognize these rights at the end of an accounting period by preparing an

adjusting entry to correct the account balances. To indicate the dual nature of these adjustments, they

record a related revenue in addition to the asset. We also call these adjustments accrued revenues

because the revenues must be recorded.

Interest revenue Savings accounts literally earn interest moment by moment. Rarely is payment

of the interest made on the last day of the accounting period. Thus, the accounting records normally do

not show the interest revenue earned (but not yet received), which affects the total assets owned by the

investor, unless the company makes an adjusting entry. The adjusting entry at the end of the

accounting period debits a receivable account (an asset) and credits a revenue account to record the

interest earned and the asset owned.

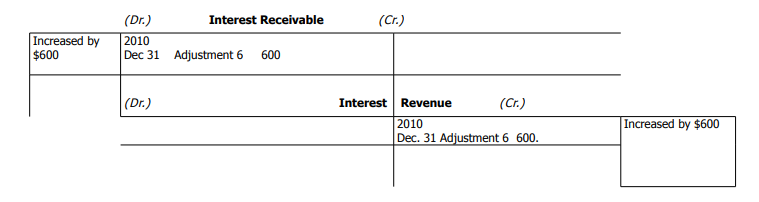

For example, assume MicroTrain Company has some money in a savings account. On 2010

December 31, the money on deposit has earned one month’s interest of USD 600, although the company has not received the interest. An entry must show the amount of interest earned by 2010

December 31, as well as the amount of the asset, interest receivable (the right to receive this interest).

The entry to record the accrual of revenue is:

The T-accounts relating to interest would appear as follows:

MicroTrain reports the USD 600 debit balance in Interest Receivable as an asset in the 2010

December 31, balance sheet. This asset accumulates gradually with the passage of time. The USD 600

credit balance in Interest Revenue is the interest earned during the month. Recall that in recording

revenue under accrual basis accounting, it does not matter whether the company collects the actual

cash during the year or not. It reports the interest revenue earned during the accounting period in the

income statement.

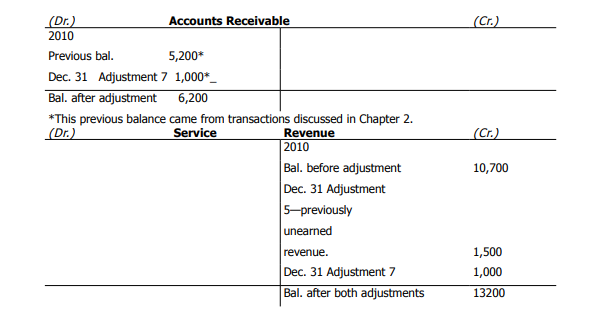

Unbilled training fees A company may perform services for customers in one accounting period

while it bills for the services in a different accounting period.

MicroTrain Company performed USD 1,000 of training services on account for a client at the end of

December. Since it takes time to do the paper work, MicroTrain will bill the client for the services in

January. The necessary adjusting journal entry at 2010 December 31, is:

After posting the adjusting entry, the T-accounts appear as follows:

The service revenue appears in the income statement; the asset, accounts receivable, appears in the

balance sheet.

Accrued liabilities are liabilities not yet recorded at the end of an accounting period. They

represent obligations to make payments not legally due at the balance sheet date, such as employee

salaries. At the end of the accounting period, the company recognizes these obligations by preparing an

adjusting entry including both a liability and an expense. For this reason, we also call these obligations

accrued expenses.

Salaries The recording of the payment of employee salaries usually involves a debit to an expense

account and a credit to Cash. Unless a company pays salaries on the last day of the accounting period

for a pay period ending on that date, it must make an adjusting entry to record any salaries incurred

but not yet paid.

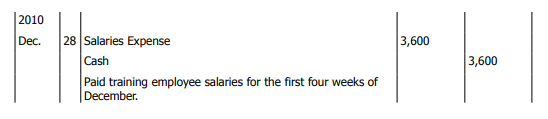

MicroTrain Company paid USD 3,600 of salaries on Friday, 2010 December 28, to cover the first

four weeks of December. The entry made at that time was:

Assuming that the last day of December 2010 falls on a Monday, this expense account does not

show salaries earned by employees for the last day of the month. Nor does any account show the

employer’s obligation to pay these salaries. The T-accounts pertaining to salaries appear as follows

before adjustment:

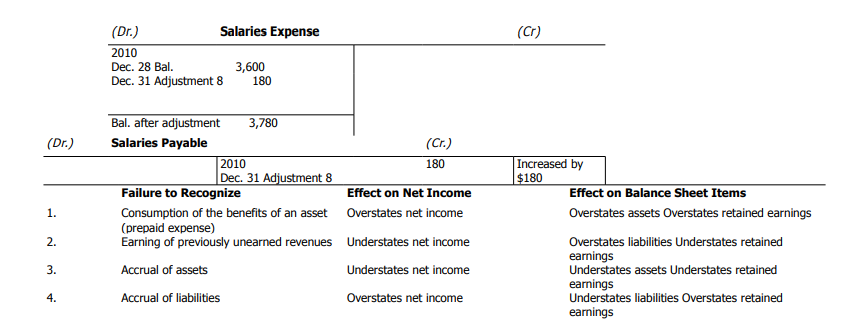

If salaries are USD 3,600 for four weeks, they are USD 900 per week. For a five-day workweek,

daily salaries are USD 180. MicroTrain makes the following adjusting entry on December 31 to accrue

salaries for one day:

After adjustment, the two T-accounts involved appear as follows:

Exhibit 18: Effects of failure to recognize adjustments

The debit in the adjusting journal entry brings the month’s salaries expense up to its correct USD

3,780 amount for income statement purposes. The credit to Salaries Payable records the USD 180

salary liability to employees. The balance sheet shows salaries payable as a liability. Another example of a liability/expense adjustment is when a company incurs interest on a note

payable. The debit would be to Interest Expense, and the credit would be to Interest Payable.

Effects of failing to prepare adjusting entries

Failure to prepare proper adjusting entries causes net income and the balance sheet to be in error.

You can see the effect of failing to record each of the major types of adjusting entries on net income and

balance sheet items in Exhibit 18.

Using MicroTrain Company as an example, this chapter has discussed and illustrated many of the

typical entries that companies must make at the end of an accounting period. Later chapters explain

other examples of adjusting entries.

Analyzing and using the financial results—trend percentages

It is sometimes more informative to express all the dollar amounts as a percentage of one of the

amounts in the base year rather than to look only at the dollar amount of the item in the financial

statements. You can calculate trend percentages by dividing the amount for each year for an item,

such as net income or net sales, by the amount of that item for the base year:

![]()

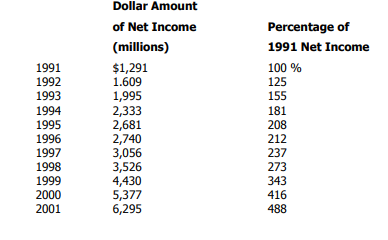

To illustrate, assume that ShopaLot, a large retailer, and its subsidiaries reported the following net

income for the years ended 2001 January 31, through 2010. The last column expresses these dollar

amounts as a percentage of the 2001 amount. For instance, we would calculate the 125 per cent for

2002 as:

[(USD 1,609,000/USD 1,291,000)5 100]

Examining the trend percentages, we can see that ShopaLot's s net income has increased steadily over the 10-year period. The 2010 net income is over 4 times as much as the 2001 amount. This is the kind of performance that management and stockholders seek, but do not always get. In the first three chapters of this text, you have learned most of the steps of the accounting process.

Last modified: Tuesday, May 28, 2019, 12:10 PM