Reading: Lesson 6 - A classified balance sheet

The balance sheets we presented so far have been unclassified balance sheets. As shown in Exhibit

23, an unclassified balance sheet has three major categories: assets, liabilities, and stockholders'

equity. A classified balance sheet contains the same three major categories and subdivides them to

provide useful information for interpretation and analysis by users of financial statements.

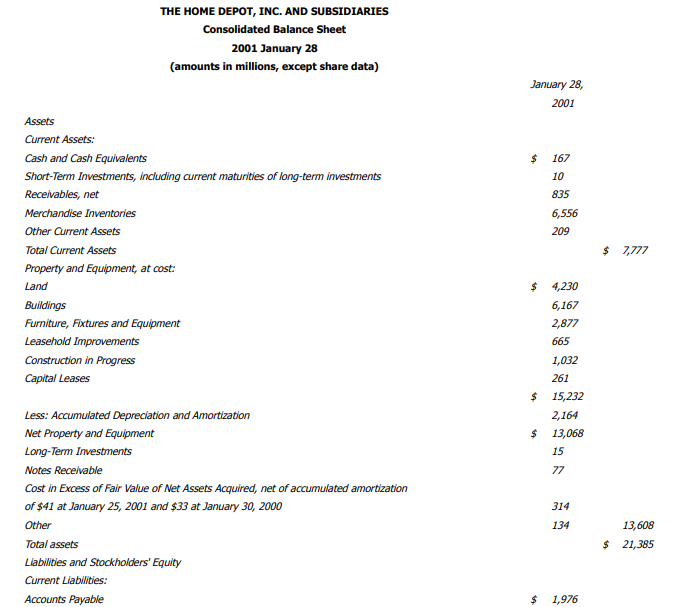

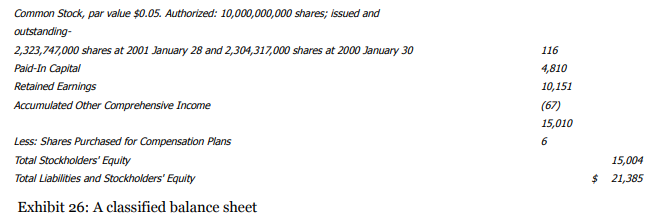

Exhibit 26, shows a slightly revised classified balance sheet for The Home Depot, Inc., and

subsidiaries.1 Note that The Home Depot classified balance sheet is in a vertical format (assets

appearing above liabilities and stockholders' equity) rather than the horizontal format (assets on the

left and liabilities and stockholders' equity on the right). The two formats are equally acceptable.

The Home Depot classified balance sheet subdivides two of its three major categories. The Home

Depot subdivides its assets into current assets, property and equipment, long-term investments, longterm

notes receivable, intangible assets (cost in excess of the fair value of net assets acquired), and

other assets. The company subdivides its liabilities into current liabilities and long-term liabilities

(including deferred income taxes). A later chapter describes minority interest. Stockholders' equity is

the same in a classified balance sheet as in an unclassified balance sheet. Later chapters describe

further subdivisions of the stockholders' equity section.

We discuss the individual items in the classified balance sheet later in the text. Our only purpose

here is to briefly describe the items that can be listed under each category. Some of these items are not

in The Home Depot's balance sheet.

Current assets are cash and other assets that a business can convert to cash or uses up in a

relatively short period—one year or one operating cycle, whichever is longer. An operating cycle is

the time it takes to start with cash, buy necessary items to produce revenues (such as materials,

supplies, labor, and/or finished goods), sell services or goods, and receive cash by collecting the

resulting receivables. Companies in service industries and merchandising industries generally have

operating cycles shorter than one year. Companies in some manufacturing industries, such as distilling

and lumber, have operating cycles longer than one year. However, since most operating cycles are

shorter than one year, the one-year period is usually used in identifying current assets and current

liabilities. Common current assets in a service business include cash, marketable securities, accounts

receivable, notes receivable, interest receivable, and prepaid expenses. Note that on a balance sheet,

current assets are in order of how easily they are convertible to cash, from most liquid to least liquid.

Cash includes deposits in banks available for current operations at the balance sheet date plus cash

on hand consisting of currency, undeposited checks, drafts, and money orders. Cash is the first current

asset to appear on a balance sheet. The term cash normally includes cash equivalents.

Cash equivalents are highly liquid, short-term investments acquired with temporarily idle cash

and easily convertible into a known cash amount. Examples are Treasury bills, short-term notes

maturing within 90 days, certificates of deposit, and money market funds.

Marketable securities are temporary investments such as short-term ownership of stocks and

bonds of other companies. Such investments do not qualify as cash equivalents. These investments

earn additional money on cash that the business does not need at present but will probably need within

one year.

Accounts receivable (also called trade accounts receivable) are amounts owed to a business by

customers. An account receivable arises when a company performs a service or sells merchandise on

credit. Customers normally provide no written evidence of indebtedness on sales invoices or delivery tickets except their signatures. Notice the term net in the balance sheet of The Home Depot (Exhibit

26). This term indicates the possibility that the company may not collect some of its accounts

receivable. In the balance sheet, the accounts receivable amount is the sum of the individual accounts

receivable from customers shown in a subsidiary ledger or file.

Merchandise inventories are goods held for sale. Chapter 6 begins our discussion of

merchandise inventories.

A note is an unconditional written promise to pay another party the amount owed either when

demanded or at a certain specified date, usually with interest (a charge made for use of the money) at a

specified rate. A note receivable appears on the balance sheet of the company to which the note is

given. A note receivable arises (1) when a company makes a sale and receives a note from the customer,

(2) when a customer gives a note for an amount due on an account receivable, or (3) when a company

loans money and receives a note in return. Unit 10 discusses notes at length.

Other current assets might include interest receivable and prepaid expenses. Interest receivable

arises when a company has earned but not collected interest by the balance sheet date. Usually, the

amount is not due until later. Prepaid expenses include rent, insurance, and supplies that have been

paid for but all the benefits have not yet been realized (or consumed) from these expenses. If prepaid

expenses had not been paid for in advance, they would require the future disbursement of cash.

Furthermore, prepaid expenses are considered assets because they have service potential.

Long-term assets are assets that a business has on hand or uses for a relatively long time.

Examples include property, plant, and equipment; long-term investments; and intangible assets.

Property, plant, and equipment are assets with useful lives of more than one year; a company

acquires them for use in the business rather than for resale. (These assets are called property and

equipment in The Home Depot's balance sheet.) The terms plant assets or fixed assets are also used for

property, plant, and equipment. To agree with the order in the heading, balance sheets generally list

property first, plant next, and equipment last. These items are fixed assets because the company uses

them for long-term purposes. We describe several types of property, plant, and equipment next.

Land is ground the company uses for business operations; this includes ground on which the

company locates its business buildings and that is used for outside storage space or parking. Land

owned for investment is not a plant asset because it is a long-term investment.

Buildings are structures the company uses to carry on its business. Again, the buildings that a

company owns as investments are not plant assets.

Office furniture includes file cabinets, desks, chairs, and shelves.

Office equipment includes computers, copiers, FAX machines, and phone answering machines.

Leasehold improvements are any physical alterations made by the lessee to the leased property

when these benefits are expected to last beyond the current accounting period. An example is when the

lessee builds room partitions in a leased building. (The lessee is the one obtaining the rights to possess

and use the property.)

Construction in progress represents the partially completed stores or other buildings that a

company such as The Home Depot plans to occupy when completed.

Accumulated depreciation is a contra asset account to depreciable assets such as buildings,

machinery, and equipment. This account shows the total depreciation taken for the depreciable assets.

On the balance sheet, companies deduct the accumulated depreciation (as a contra asset) from its

related asset.

Long-term investments A long-term investment usually consists of securities of another

company held with the intention of (1) obtaining control of another company, (2) securing a permanent

source of income for the investor, or (3) establishing friendly business relations. The long-term

investment classification in the balance sheet does not include those securities purchased for shortterm

purposes. For most businesses, long-term investments may be stocks or bonds of other

corporations. Occasionally, long-term investments include funds accumulated for specific purposes,

rental properties, and plant sites for future use.

Intangible assets Intangible assets consist of the noncurrent, nonmonetary, nonphysical

assets of a business. Companies must charge the costs of intangible assets to expense over the period

benefited. Among the intangible assets are rights granted by governmental bodies, such as patents and

copyrights. Other intangible assets include leaseholds and goodwill.

A patent is a right granted by the federal government; it gives the owner of an invention the

authority to manufacture a product or to use a process for a specified time.

A copyright granted by the federal government gives the owner the exclusive privilege of

publishing written material for a specified time.

Leaseholds are rights to use rented properties, usually for several years.

Accumulated amortization is a contra asset account to intangible assets. This account shows

the total amortization taken on the intangible assets.

Current liabilities are debts due within one year or one operating cycle, whichever is longer. The

payment of current liabilities normally requires the use of current assets. Balance sheets list current

liabilities in the order they must be paid; the sooner a liability must be paid, the earlier it is listed.

Examples of current liabilities follow.

Accounts payable are amounts owed to suppliers for goods or services purchased on credit.

Accounts payable are generally due in 30 or 60 days and do not bear interest. In the balance sheet, the

accounts payable amount is the sum of the individual accounts payable to suppliers shown in a

subsidiary ledger or file.

Notes payable are unconditional written promises by the company to pay a specific sum of money

at a certain future date. The notes may arise from borrowing money from a bank, from the purchase of

assets, or from the giving of a note in settlement of an account payable. Generally, only notes payable

due in one year or less are included as current liabilities.

Salaries payable are amounts owed to employees for services rendered. The company has not

paid these salaries by the balance sheet date because they are not due until later.

Sales taxes payable are the taxes a company has collected from customers but not yet remitted to

the taxing authority, usually the state.

Other accrued expenses might include taxes withheld from employees, income taxes payable, and

interest payable. Taxes withheld from employees include federal income taxes, state income taxes,

and social security taxes withheld from employees' paychecks. The company plans to pay these

amounts to the proper governmental agencies within a short period. Income taxes payable are the

taxes paid to the state and federal governments by a corporation on its income. Interest payable is

interest that the company has accumulated on notes or bonds but has not paid by the balance sheet

date because it is not due until later.

Dividends payable, or amounts the company has declared payable to stockholders, represent a

distribution of income. Since the corporation has not paid these declared dividends by the balance

sheet date, they are a liability.

Unearned revenues (revenues received in advance) result when a company receives payment for

goods or services before earning the revenue, such as payments for subscriptions to a magazine. These

unearned revenues represent a liability to perform the agreed services or other contractual

requirements or to return the assets received.

Companies report any current installment on long-term debt due within one year under current

liabilities. The remaining portion continues to be reported as a long-term liability.

Long-term liabilities are debts such as a mortgage payable and bonds payable that are not due

for more than one year. Companies should show maturity dates in the balance sheet for all long-term

liabilities. Normally, the liabilities with the earliest due dates are listed first.

Notes payable with maturity dates at least one year beyond the balance sheet date are long-term

liabilities.

Bonds payable are long-term liabilities and are evidenced by formal printed certificates

sometimes secured by liens (claims) on property, such as mortgages. Maturity dates should appear on

the balance sheet for all major long-term liabilities.

The deferred income taxes on The Home Depot's balance sheet result from a difference between

income tax expense in the accounting records and the income tax payable on the company's tax return.

Stockholders' equity shows the owners' interest in the business. This interest is equal to the

amount contributed plus the income left in the business.

The items under stockholders' equity in The Home Depot's balance sheet are paid-in capital (including common stock) and retained earnings. Paid-in capital shows the capital paid into the company as the owners' investment. Retained earnings shows the cumulative income of the company less the amounts distributed to the owners in the form of dividends. Cumulative translation adjustments result from translating foreign currencies into US dollars (a topic discussed in advanced accounting courses).

Остання зміна: вівторок 28 травня 2019 12:11 PM