Reading: Lesson 7 - Qualitative characteristics

Accounting information should possess qualitative characteristics to be useful in decision

making. This criterion is difficult to apply. The usefulness of accounting information in a given

instance depends not only on information characteristics but also on the capabilities of the decision

makers and their professional advisers. Accountants cannot specify who the decision makers are, their

characteristics, the decisions to be made, or the methods chosen to make the decisions. Therefore, they

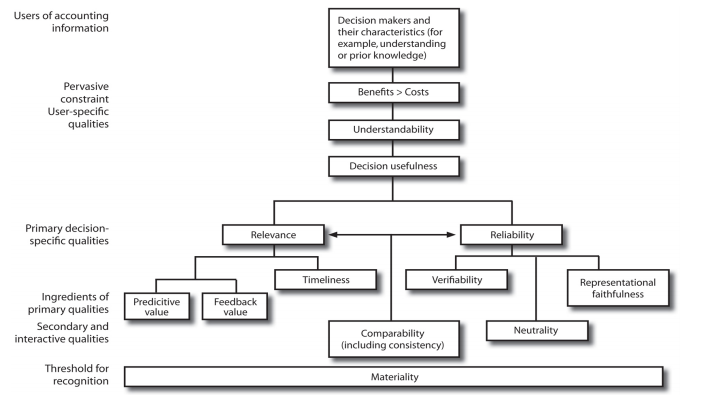

direct their attention to the characteristics of accounting information. Note the FASB's graphic

summarization of the qualities accountants consider in Exhibit 31.

To have relevance, information must be pertinent to or affect a decision. The information must

make a difference to someone who does not already have it. Relevant information makes a difference in

a decision either by affecting users' predictions of outcomes of past, present, or future events or by

confirming or correcting expectations. Note that information need not be a prediction to be useful in

developing, confirming, or altering expectations. Expectations are commonly based on the present or

past. For example, any attempt to predict future earnings of a company would quite likely start with a

review of present and past earnings. Although information that merely confirms prior expectations

may be less useful, it is still relevant because it reduces uncertainty.

Critics have alleged that certain types of accounting information lack relevance. For example, some

argue that a cost of USD 1 million paid for a tract of land 40 years ago and reported in the current

balance sheet at that amount is irrelevant (except for possible tax implications) to users for decision

making today. Such criticism has encouraged research into the types of information relevant to users.

Some suggest using a different valuation basis, such as current cost, in reporting such assets.

Predictive value and feedback value Since actions taken now can affect only future events,

information is obviously relevant when it possesses predictive value, or improves users' abilities to

predict outcomes of events. Information that reveals the relative success of users in predicting

outcomes possesses feedback value. Feedback reports on past activities and can make a difference in decision making by (1) reducing uncertainty in a situation, (2) refuting or confirming prior

expectations, and (3) providing a basis for further predictions. For example, a report on the first

quarter's earnings of a company reduces the uncertainty surrounding the amount of such earnings,

confirms or refutes the predicted amount of such earnings, and provides a possible basis on which to

predict earnings for the full year. Remember that although accounting information may possess

predictive value, it does not consist of predictions. Making predictions is a function performed by the

decision maker.

Timeliness Timeliness requires accountants to provide accounting information at a time when it

may be considered in reaching a decision. Utility of information decreases with age. To know what the

net income for 2010 was in early 2011 is much more useful than receiving this information a year later.

If information is to be of any value in decision making, it must be available before the decision is made.

If not, the information is of little value. In determining what constitutes timely information,

accountants consider the other qualitative characteristics and the cost of gathering information. For

example, a timely estimate for uncollectible accounts may be more valuable than a later, verified actual

amount. Timeliness alone cannot make information relevant, but potentially relevant information can

be rendered irrelevant by a lack of timeliness.

In addition to being relevant, information must be reliable to be useful. Information has reliability

when it faithfully depicts for users what it purports to represent. Thus, accounting information is

reliable if users can depend on it to reflect the underlying economic activities of the organization. The

reliability of information depends on its representational faithfulness, verifiability, and neutrality. The

information must also be complete and free of bias.

Representational faithfulness To gain insight into this quality, consider a map. When it shows

roads and bridges where roads and bridges actually exist, a map possesses representational

faithfulness. A correspondence exists between what is on the map and what is present physically.

Similarly, representational faithfulness exists when accounting statements on economic activity

correspond to the actual underlying activity. Where there is no correspondence, the cause may be (1)

bias or (2) lack of completeness.

- Effects of bias. Accounting measurements contain bias if they are consistently too high or too

low. Accountants create bias in accounting measurements by choosing the wrong measurement

method or introducing bias either deliberately or through lack of skill.

- Completeness. To be free from bias, information must be sufficiently complete to ensure that

it validly represents underlying events and conditions. Completeness means disclosing all

significant information in a way that aids understanding and does not mislead. Firms can reduce

the relevance of information by omitting information that would make a difference to users.

Currently, full disclosure requires presentation of a balance sheet, an income statement, a

statement of cash flows, and necessary notes to the financial statements and supporting schedules.

Also required in annual reports of corporations are statements of changes in stockholders' equity

which contain information included in a statement of retained earnings. Such statements must be

complete, with items properly classified and segregated (such as reporting sales revenue

separately from other revenues). Required disclosures may be made in (1) the body of the financial

statements, (2) the notes to such statements, (3) special communications, and/or (4) the

president's letter or other management reports in the annual report.

Another aspect of completeness is fully disclosing all changes in accounting principles and their

effects.11 Disclosure should include unusual activities (loans to officers), changes in expectations (losses

on inventory), depreciation expense for the period, long-term obligations entered into that are not

recorded by the accountant (a 20-year lease on a building), new arrangements with certain groups

(pension and profit-sharing plans for employees), and significant events that occur after the date of the statements (loss of a major customer). Firms must also disclose accounting policies (major principles

and their manner of application) followed in preparing the financial statements.

12 Because of its

emphasis on disclosure, we often call this aspect of reliability the full disclosure principle.

Verifiability Financial information has verifiability when independent measurers can substantially duplicate it by using the same measurement methods. Verifiability eliminates measurer bias. The requirement that financial information be based on objective evidence arises from the demonstrated needs of users for reliable, unbiased financial information. Unbiased information is especially necessary when parties with opposing interests (credit seekers and credit grantors) rely on the same information. If the information is verifiable, this enhances the reliability of information. Financial information is never completely free of subjective opinion and judgment; it always possesses varying degrees of verifiability. Canceled checks and invoices support some measurements. Accountants can never verify other measurements, such as periodic depreciation charges, because of their very nature. Thus, financial information in many instances is verifiable only in that it represents a consensus of what other accountants would report if they followed the same procedures.

Neutrality Neutrality means that the accounting information should be free of measurement

method bias. The primary concern should be relevance and reliability of the information that results

from application of the principle, not the effect that the principle may have on a particular interest.

Non-neutral accounting information favors one set of interested parties over others. For example, a

particular form of measurement might favor stockholders over creditors, or vice versa. "To be neutral,

accounting information must report economic activity as faithfully as possible, without coloring the

image it communicates for the purpose of influencing behavior in some particular direction." 13

Accounting standards are not like tax regulations that deliberately foster or restrain certain types of

activity. Verifiability seeks to eliminate measurer bias; neutrality seeks to eliminate measurement

method bias.

When comparability exists, reported differences and similarities in financial information are real

and not the result of differing accounting treatments. Comparable information reveals relative

strengths and weaknesses in a single company through time and between two or more companies at

the same time.

Consistency requires that a company use the same accounting principles and reporting practices through time. Consistency leads to comparability of financial information for a single company through time. Comparability between companies is more difficult because they may account for the same activities in different ways. For example, Company B may use one method of depreciation, while Company C accounts for an identical asset in similar circumstances using another method. A high degree of inter-company comparability in accounting information does not exist unless accountants are required to account for the same activities in the same manner across companies and through time. As we show in Exhibit 31, accountants must consider one pervasive constraint and one threshold for recognition in providing useful information. First, the benefits secured from the information must be greater than the costs of providing that information. Second, only material items need be disclosed and accounted for strictly in accordance with generally accepted accounting principles (GAAP).

Остання зміна: вівторок 28 травня 2019 12:11 PM