Reading: Lesson 5 - Analyzing and using financial results—inventory turnover ratio

An important ratio for managers, investors, and creditors to consider when analyzing a company's

inventory is the inventory turnover ratio. This ratio tests whether a company is generating a sufficient

volume of business based on its inventory. To calculate the inventory turnover ratio:

Inventory turnover measures the efficiency of the firm in managing and selling inventory: thus, it

gauges the liquidity of the firm's inventory. A high inventory turnover is generally a sign of efficient

inventory management and profit for the firm; the faster inventory sells, the less time funds are tied up

in inventory. A relatively low turnover could be the result of a company carrying too much inventory or

stocking inventory that is obsolete, slow-moving, or inferior.

In assessing inventory turnover, analysts also consider the type of industry. When making

comparisons among firms, they check the cost-flow assumption used to value inventory and cost of

products sold.

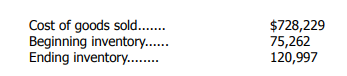

Abercrombie & Fitch reported the following financial data for 2000 (in thousands):

Their inventory turnover is:

USD 728,229/[(USD 75,262 + USD 120,997)/2] = 7.4 times

You should now understand the importance of taking an accurate physical inventory and knowing how to value this inventory. In the next chapter, you will learn the general principles of internal control and how to control cash. Cash is one of a company's most important and mobile assets.

Last modified: Tuesday, May 28, 2019, 12:12 PM