Reading: Lesson 4 - Short-term financing through notes payable

A company sometimes needs short-term financing. This situation may occur when

(1) the company's cash receipts are delayed because of lenient credit terms granted

customers, or (2) the company needs cash to finance the buildup of seasonal

inventories, such as before Christmas. To secure short-term financing, companies issue

interest-bearing or non interest-bearing notes.

Interest-bearing notes To receive short-term financing, a company may issue an

interest-bearing note to a bank. An interest-bearing note specifies the interest rate

charged on the principal borrowed. The company receives from the bank the principal

borrowed; when the note matures, the company pays the bank the principal plus the

interest.

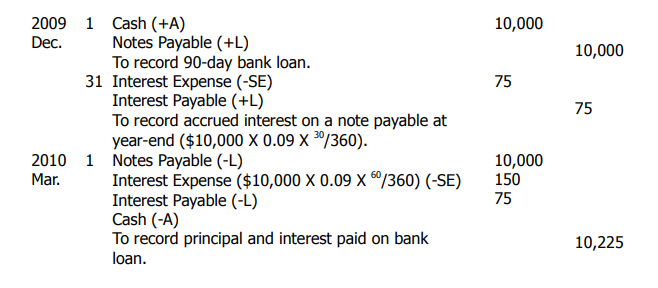

Accounting for an interest-bearing note is simple. For example, assume the

company's accounting year ends on December 31. Needham Company issued a USD

10,000, 90-day, 9 percent note on 2009 December 1. The following entries would

record the loan, the accrual of interest on 2009 December 31 and its payment on 2010

March 1:

Non interest-bearing notes (discounting notes payable) A company may

also issue a non interest-bearing note to receive short-term financing from a bank. A

non interest-bearing note does not have a stated interest rate applied to the face value

of the note. Instead, the note is drawn for a maturity amount less a bank discount; the

borrower receives the proceeds. A bank discount is the difference between the

maturity value of the note and the cash proceeds given to the borrower. The cash

proceeds are equal to the maturity amount of a note less the bank discount. This

entire process is called discounting a note payable. The purpose of this process is

to introduce interest into what appears to be a non interest-bearing note. The meaning

of discounting here is to deduct interest in advance

Needham credits Notes Payable for the face value of the note. Discount on notes

payable is a contra account used to reduce Notes Payable from face value to the net

amount of the debt. The balance in the Discount on Notes Payable account appears on

the balance sheet as a deduction from the balance in the Notes Payable account.

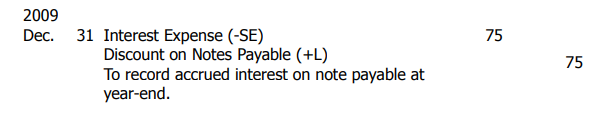

Over time, the discount becomes interest expense. If Needham paid the note before

the end of the fiscal year, it would charge the entire USD 225 discount to Interest

Expense and credit Discount on Notes Payable. However, if Needham's fiscal year

ended on December 31, an adjusting entry would be required as follows:

This entry records the interest expense incurred by Needham for the 30 days the

note has been outstanding. The expense can be calculated as USD 10,000 X 0.09 X

30/360, or 30/90 X USD 225. Notice that for entries involving discounted notes

payable, no separate Interest Payable account is needed. The Notes Payable account

already contains the total liability that will be paid at maturity, USD 10,000. From the

date the proceeds are given to the borrower to the maturity date, the liability grows by

reducing the balance in the Discount on Notes Payable contra account. Thus, the

current liability section of the 2009 December 31, balance sheet would show:

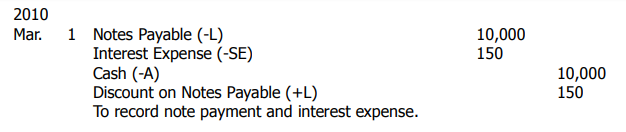

When the note is paid at maturity, the entry is:

The T-accounts for Discount on Notes Payable and for Interest Expense appear as

follows:

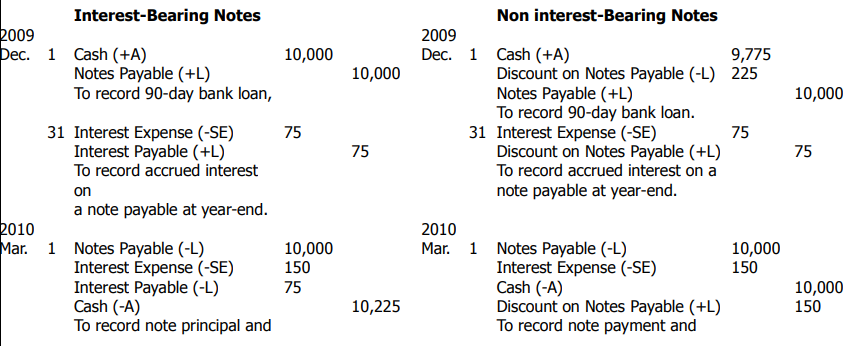

In Exhibit 3, we compare the journal entries for interest-bearing notes and noninterest-bearing

notes used by Needham Company.

Exhibit 3: Comparison between interest-bearing notes and noninterest-bearing notes

Last modified: Tuesday, May 28, 2019, 12:13 PM