Reading: Lesson 4 - Depreciation of plant assets

Companies record depreciation on all plant assets except land. Since the amount of

depreciation may be relatively large, depreciation expense is often a significant factor

in determining net income. For this reason, most financial statement users are

interested in the amount of, and the methods used to compute, a company's

depreciation expense.

Depreciation is the amount of plant asset cost allocated to each accounting period

benefiting from the plant asset's use. Depreciation is a process of allocation, not

valuation. Eventually, all assets except land wear out or become so inadequate or

outmoded that they are sold or discarded; therefore, firms must record depreciation on

every plant asset except land. They record depreciation even when the market value of

a plant asset temporarily rises above its original cost because eventually the asset is no

longer useful to its current owner.

Major causes of depreciation are (1) physical deterioration, (2) inadequacy for

future needs, and (3) obsolescence. Physical deterioration results from the use of

the asset—wear and tear—and the action of the elements. For example, an automobile

may have to be replaced after a time because its body rusted out. The inadequacy of a

plant asset is its inability to produce enough products or provide enough services to meet current demands. For example, an airline cannot provide air service for 125

passengers using a plane that seats 90. The obsolescence of an asset is its decline in

usefulness brought about by inventions and technological progress. For example, the

development of the xerographic process of reproducing printed matter rendered

almost all previous methods of duplication obsolete.

The use of a plant asset in business operations transforms a plant asset cost into an

operating expense. Depreciation, then, is an operating expense resulting from the use

of a depreciable plant asset. Because depreciation expense does not require a current

cash outlay, it is often called a noncash expense. The purchaser gave up cash in the

period when the asset was acquired, not during the periods when depreciation expense

is recorded.

To compute depreciation expense, accountants consider four major factors:

- Cost of the asset.

- Estimated salvage value of the asset. Salvage value (or scrap value) is the

amount of money the company expects to recover, less disposal costs, on the date a

plant asset is scrapped, sold, or traded in.

- Estimated useful life of the asset. Useful life refers to the time the company

owning the asset intends to use it; useful life is not necessarily the same as either

economic life or physical life. The economic life of a car may be 7 years and its

physical life may be 10 years, but if a company has a policy of trading cars every 3

years, the useful life for depreciation purposes is 3 years. Various firms express

useful life in years, months, working hours, or units of production. Obsolescence

also affects useful life. For example, a machine capable of producing units for 20

years, may be expected to be obsolete in 6 years. Thus, its estimated useful life is 6

years—not 20. Another example, on TV you may have seen a demolition crew

setting off explosives in a huge building (e.g. The Dunes Hotel and Casino in Las

Vegas, Nevada, USA) and wondering why the owners decided to destroy what

looked like a perfectly good building. The building was destroyed because it had

reached the end of its economic life. The land on which the building stood could be

put to better use, possibly by constructing a new building.

- • Depreciation method used in depreciating the asset. We describe the four

common depreciation methods in the next section.

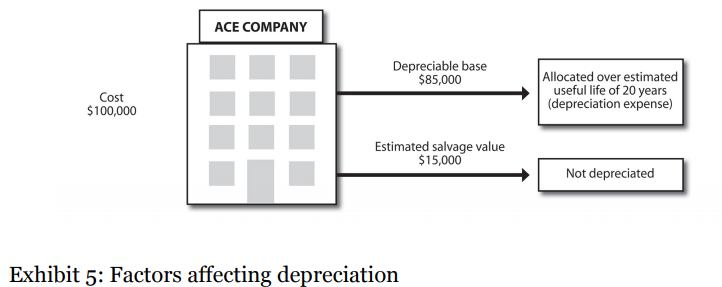

In Exhibit 5, note the relationship among these factors. Assume Ace Company

purchased an office building for USD 100,000. The building has an estimated salvage

value of USD 15,000 and a useful life of 20 years. The depreciable cost of the building

is USD 85,000 (cost less estimated salvage value). Ace would allocate this depreciable

base over the useful life of the building using the proper depreciation method under

the circumstances.

Today, companies can use many different methods to calculate depreciation on

assets.3

This section discusses and illustrates the most common methods—straightline,

units-of-production, and accelerated depreciation method (double-decliningbalance).

As is true for inventory methods, normally a company is free to adopt the most

appropriate depreciation method for its business operations. According to accounting

theory, companies should use a depreciation method that reflects most closely their

underlying economic circumstances. Thus, companies should adopt the depreciation

method that allocates plant asset cost to accounting periods according to the benefits

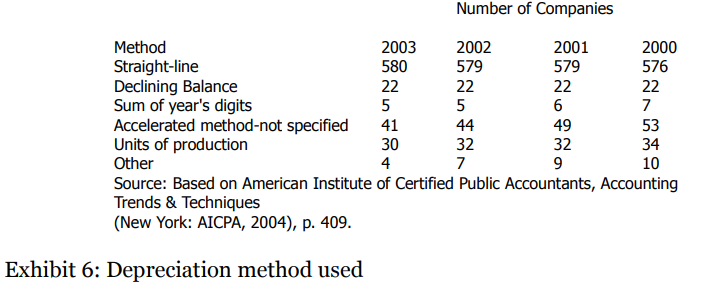

received from the use of the asset. Exhibit 6 shows the frequency of use of these

methods for 600 companies. You can see that most companies use the straight-line

method for financial reporting purposes. Note that some companies use one method

for certain assets and another method for other assets. In practice, measuring the

benefits from the use of a plant asset is impractical and often not possible. As a result, a

depreciation method must meet only one standard: the depreciation method must allocate plant asset cost to accounting periods in a systematic and rational manner. The

following four methods meet this requirement.

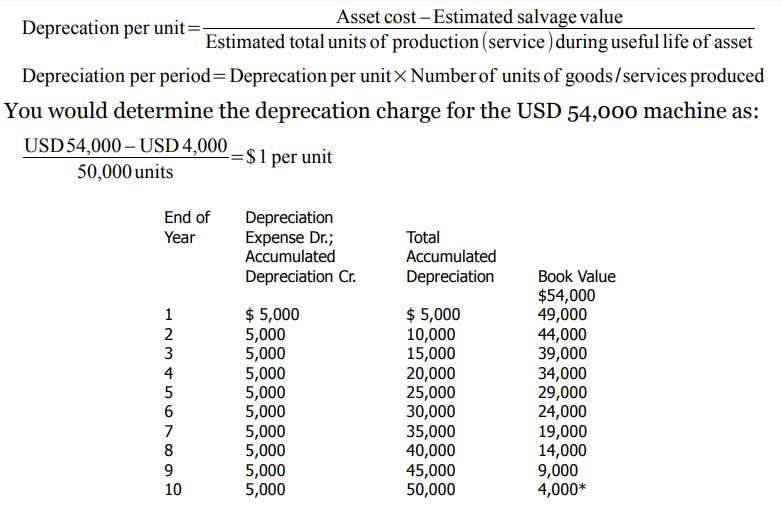

In the illustrations of the four depreciation methods that follow, we assume the

following: On 2010 January 1, a company purchased a machine for USD 54,000 with an

estimated useful life of 10 years, or 50,000 units of output, and an estimated salvage

value of USD 4,000.

Straight-line method Straight-line depreciation has been the most widely

used depreciation method in the United States for many years because, as you saw in

Chapter 3, it is easily applied. To apply the straight-line method, a firm charges an

equal amount of plant asset cost to each accounting period. The formula for calculating

depreciation under the straight-line method is:

In Exhibit 7, we present a schedule of annual depreciation entries, cumulative

balances in the accumulated depreciation account, and the book (or carrying) values of

the USD 54,000 machine.

Using the straight-line method for assets is appropriate where (1) time rather than

obsolescence is the major factor limiting the asset's life and (2) the asset produces

relatively constant amounts of periodic services. Assets that possess these features

include items such as pipelines, fencing, and storage tanks. Units-of-production (output) method The units-of-production

depreciation method assigns an equal amount of depreciation to each unit of product

manufactured or service rendered by an asset. Since this method of depreciation is

based on physical output, firms apply it in situations where usage rather than

obsolescence leads to the demise of the asset. Under this method, you would compute

the depreciation charge per unit of output. Then, multiply this figure by the number of

units of goods or services produced during the accounting period to find the period's

depreciation expense. The formula is:

Exhibit 7: Straight-line depreciation schedule

If the machine produced 1,000 units in 2010 and 2,500 units in 2011, depreciation

expense for those years would be USD 1,000 and USD 2,500, respectively.

Accelerated depreciation methods record higher amounts of depreciation

during the early years of an asset's life and lower amounts in the asset's later years. A

business might choose an accelerated depreciation method for the following reasons:

- The value of the benefits received from the asset decline with age (for example, office buildings).

- The asset is a high-technology asset subject to rapid obsolescence (for example, computers).

- Repairs increase substantially in the asset's later years; under this method, the depreciation and repairs together remain fairly constant over the asset's life (for example, automobiles).

The most common accelerated method of depreciation is the double-decliningbalance

(DDB) method.

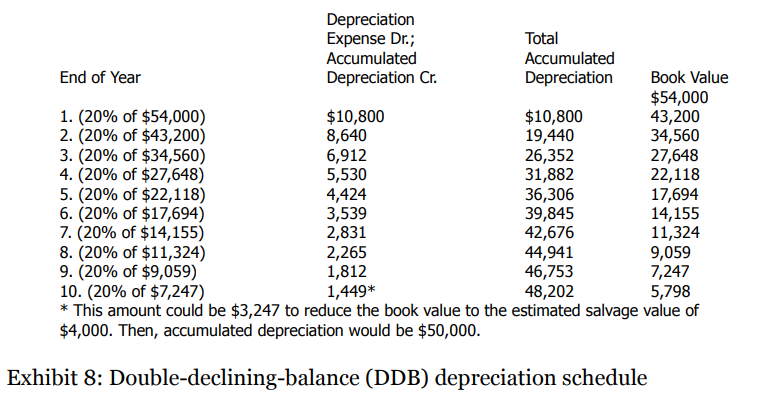

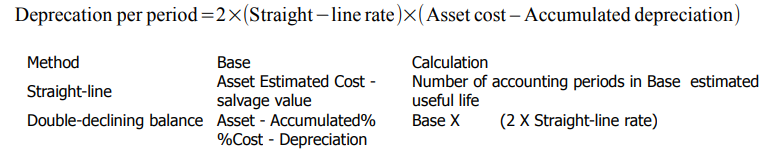

Double-declining-balance method To apply the double-declining-balance

(DDB) method of computing periodic depreciation charges you begin by calculating

the straight-line depreciation rate. To do this, divide 100 percent by the number of

years of useful life of the asset. Then, multiply this rate by 2. Next, apply the resulting

double-declining rate to the declining book value of the asset. Ignore salvage value in making the calculations. At the point where book value is equal to the salvage value, no

more depreciation is taken. The formula for DDB depreciation is:

Exhibit 9: Summary of depreciation methods

Look at the calculations for the USD 54,000 machine using the DDB method in

Exhibit 8. The straight-line rate is 10 percent (100 percent/10 years), which, when

doubled, yields a DDB rate of 20 percent. (Expressed as fractions, the straight-line rate

is 1/10, and the DDB rate is 2/10.) Since at the beginning of year 1 no accumulated

depreciation has been recorded, cost is the basis of the calculation. In each of the

following years, book value is the basis of the calculation at the beginning of the year.

In the 10th year, you could increase depreciation to USD 3,247 if the asset is to be

retired and its salvage value is still USD 4,000. This higher depreciation amount for

the last year (USD 3,247) would reduce the book value of USD 7,247 down to the

salvage value of USD 4,000. If an asset is continued in service, depreciation should

only be recorded until the asset's book value equals its estimated salvage value.

For a summary of the three depreciation methods, see Exhibit 9.

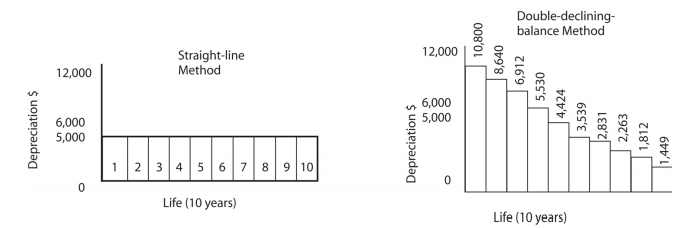

In Exhibit 10, we compare two of the depreciation methods just discussed—straight

line and double-declining balance—using the same example of a machine purchased on

2010 January 1, for USD 54,000. The machine has an estimated useful life of 10 years

and an estimated salvage value of USD 4,000.

So far we have assumed that the assets were put into service at the beginning of an

accounting period and ignored the fact that often assets are put into service during an

accounting period. When assets are acquired during an accounting period, the first

recording of depreciation is for a partial year. Normally, firms calculate the

depreciation for the partial year to the nearest full month the asset was in service. For

example, they treat an asset purchased on or before the 15th day of the month as if it

were purchased on the 1st day of the month. And they treat an asset purchased after

the 15th of the month as if it were acquired on the 1st day of the following month.

To compare the calculation of partial-year depreciation, we use a machine

purchased for USD 7,600 on 2010 September 1, with an estimated salvage value of USD

400, an estimated useful life of five years, and an estimated total units of production of

25,000 units.

Exhibit 10: Comparison of straight-line and double-declining-balance depreciation methods

Straight-line method Partial-year depreciation calculations for the straight-line

depreciation method are relatively easy. Begin by finding the 12-month charge by the

normal computation explained earlier. Then, multiply this annual amount by the fraction of the year for which the asset was in use. For example, for the USD 7,600

machine purchased 2010 September 1 (estimated salvage value, USD 400; and

estimated useful life, five years), the annual straight-line depreciation is [(USD 7,600 -

USD 400)/5 years] = USD 1,440. The machine would operate for four months prior to

the end of the accounting year, December 31, or one-third of a year. The 2010

depreciation is (USD 1,440 X 1/3) = USD 480.

Units-of-production method The units-of-production method requires no

unusual computations to record depreciation for a partial year. To compute the partialyear

depreciation, multiply the depreciation charge per unit by the units produced. The

charge for a partial year would be less than for a full year because fewer units of goods

or services are produced.

Double-declining-balance method Under the double-declining-balance

method, it is relatively easy to determine depreciation for a partial year and then for

subsequent full years. For the partial year, simply multiply the fixed rate times the cost

of the asset times the fraction of the partial year. For example, DDB depreciation on

the USD 7,600 asset for 2010 is (USD 7,600 X 0.4 X 1/3) = USD 1,013. For subsequent

years, compute the depreciation using the regular procedure of multiplying the book

value at the beginning of the period by the fixed rate. The 2011 depreciation would be

[(USD 7,600 - USD 1,013) X 0.4] = USD 2,635.

After depreciating an asset down to its estimated salvage value, a firm records no

more depreciation on the asset even if continuing to use it. At times, a firm finds the

estimated useful life of an asset or its estimated salvage value is incorrect before the

asset is depreciated down to its estimated salvage value; then, it computes revised

depreciation charges for the remaining useful life. These revised charges do not correct

past depreciation taken; they merely compensate for past incorrect charges through

changed expense amounts in current and future periods. To compute the new

depreciation charge per period, divide the book value less the newly estimated salvage

value by the estimated periods of useful life remaining.

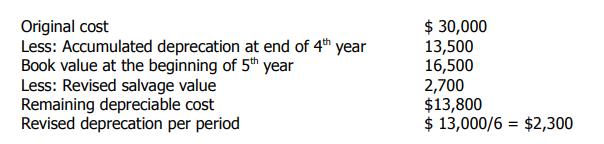

For example, assume that a machine cost USD 30,000, has an estimated salvage

value of USD 3,000, and originally had an estimated useful life of eight years. At the

end of the fourth year of the machine's life, the balance in its accumulated depreciation

account (assuming use of the straight-line method) was (USD 30,000 - USD 3,000) X

4/8 = USD 13,500. At the beginning of the fifth year, a manager estimates that the

asset will last six more years. The newly estimated salvage value is USD 2,700. To

determine the revised depreciation per period:

Had this company used the units-of-production method, its revision of the life

estimate would have been in units. Thus, to determine depreciation expense, compute

a new per-unit depreciation charge by dividing book value less revised salvage value by

the estimated remaining units of production. Multiply this per unit charge by the

periodic production to determine depreciation expense.

Using the double-declining-balance method, the book value at the beginning of year

5 would be USD 9,492.19 (cost of USD 30,000 less accumulated depreciation of USD

20,507.81). Depreciation expense for year 5 would be twice the new straight-line rate times book value. The straight-line rate is 100 percent/6 = 16.67 percent. So twice the

straight-line rate is 33.33 percent, or 1/3. Thus, 1/3 X USD 9,492.19 = USD 3,164.06.

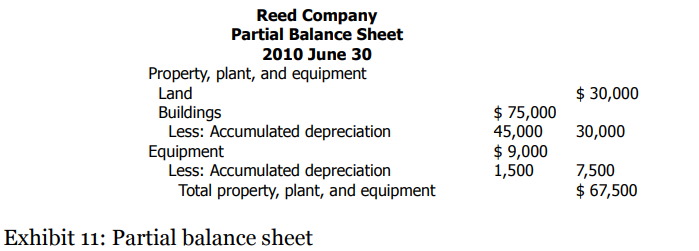

APB Opinion No. 12 requires that companies separately disclose the methods of

depreciation they use and the amount of depreciation expense for the period in the

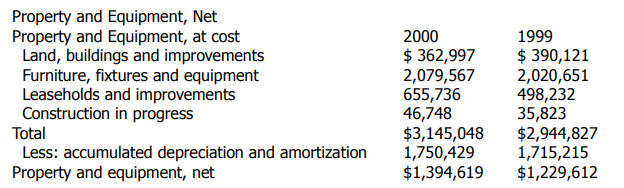

body of the income statement or in the notes to the financial statements. Major classes

of plant assets and their related accumulated depreciation amounts are reported as

shown in Exhibit 11.

Showing cost less accumulated depreciation in the balance sheet gives statement

users a better understanding of the percentages of a company's plant assets that have

been used up than reporting only the book value (remaining undepreciated cost) of the

assets. For example, reporting buildings at USD 75,000 less USD 45,000 of

accumulated depreciation, resulting in a net amount of USD 30,000, is quite different

from merely reporting buildings at USD 30,000. In the first case, the statement user

can see that the assets are about 60 percent used up. In the latter case, the statement

user has no way of knowing whether the assets are new or old.

A misconception Some mistaken financial statement users believe that

accumulated depreciation represents cash available for replacing old plant assets with

new assets. However, the accumulated depreciation account balance does not

represent cash; accumulated depreciation simply shows how much of an asset's cost

has been charged to expense. Companies use the plant asset and its contra account,

accumulated depreciation, so that data on the total original acquisition cost and

accumulated depreciation are readily available to meet reporting requirements.

Costs or market values in the balance sheet In the balance sheet, firms report

plant assets at original cost less accumulated depreciation. One of the justifications for

reporting the remaining undepreciated costs of the asset rather than market values is

the going-concern concept. As you recall from Chapter 5, the going-concern concept

assumes that the company will remain in business indefinitely, which implies the

company will use its plant assets rather than sell them. Generally, analysts do not

consider market values relevant for plant assets in primary financial statements,

although they may be reported in supplemental statements.

Last modified: Tuesday, May 28, 2019, 12:14 PM