Reading: Lesson 3 - Net Cash Flow & Free Cash Flow

2.3.A - Net Cash Flow & Free Cash Flow

1. Net Cash Flow

- In addition to the cash flow from operations as defined in the statement of cash flows, many analysts use also calculate net cash flow, which is defined as:

![]()

where net income is the net income available for distribution to common shareholders. Depreciation and amortization usually are the largest noncash items, and in many cases the other noncash items roughly net out to zero. For this reason, many analysts assume that net cash flow equals net income plus depreciation and amortization:

![]()

2. You can think of net cash flow as the profit a company would have if it did not have to replace fixed assets as they wear out. This is similar to the net cash flow from operating activities shown on the statement of cash flows, except that the net cash flow from operating activities also includes the impact of working capital. Net income, net cash flow, and net cash flow from operating activities each provide insight into a company’s financial health, but none is as useful as the measures we discuss in the next section.

- When you studied income statements in accounting, the emphasis was probably on the firm’s net income. However, the intrinsic value of a company’s operations is determined by the stream of cash flows that the operations will generate now and in the future. To be more specific, the value of operations depends on all the future expected free cash flows (FCF), defined as after-tax operating profit minus the amount of new investment in working capital and fixed assets necessary to sustain the business. Therefore, the way for managers to make their companies more valuable is to increase free cash flow now and in the future. Notice that FCF is the cash flow available for distribution to all the company’s investors after the company has made all investments necessary to sustain ongoing operations.

Calculating Free Cash Flow

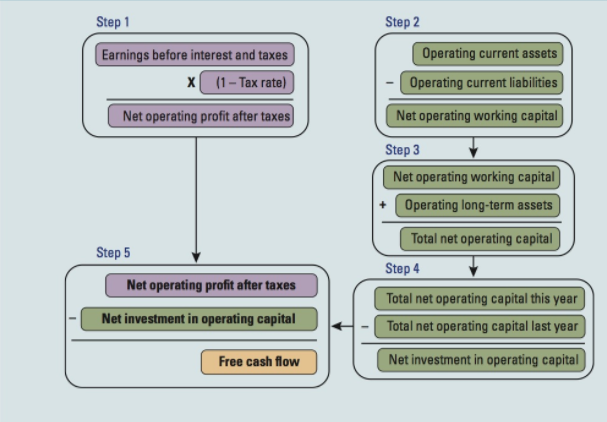

3. Net Operating Profit after Taxes (NOPAT)

- If two companies have different amounts of debt, thus different amounts of interest charges, they could have identical operating performances but different net incomes— the one with more debt would have a lower net income. Net income is important, but it does not always reflect the true performance of a company’s operations or the effectiveness of its managers. A better measure for comparing managers’ performance is net operating profit after taxes, or NOPAT, which is the amount of profit a company would generate if it had no debt and held no financial assets. NOPAT is defined as follows:

![]()

![]()

4. Net Operating Working Capital

- Most companies need some current assets to support their operating activities. For example, all companies must carry some cash to “grease the wheels” of their operations. Companies continuously receive checks from customers and write checks to suppliers, employees, and so on. Because inflows and outflows do not coincide perfectly, a company must keep some cash in its bank account. In other words, it must have some cash to conduct operations. The same is true for most other current assets, such as inventory and accounts receivable, which are required for normal operations. The short-term assets normally used in a company’s operating activities are called operating current assets.

- Not all current assets are operating current assets. For example, holdings of short-term marketable securities generally result from investment decisions made by the treasurer and not as a natural consequence of operating activities. Therefore, short-term investments are nonoperating assets and normally are excluded when calculating operating current assets. A useful rule of thumb is that if an asset pays interest, it should not be classified as an operating asset.

- Some current liabilities—especially accounts payable and accruals—arise in the normal course of operations. Such short-term liabilities are called operating current liabilities. Not all current liabilities are operating current liabilities. For example, consider the current liability shown as notes payable to banks. The company could have raised an equivalent amount as long-term debt or could have issued stock, so the choice to borrow from the bank was a financing decision and not a consequence of operations. Again, the rule of thumb is that if a liability charges interest, it is not an operating liability.

- If you are ever uncertain about whether an item is an operating asset or operating liability, ask yourself whether the item is a natural consequence of operations or if it is a discretionary choice, such as a particular method of financing or an investment in a particular financial asset. If it is discretionary, then the item is not an operating asset or liability.

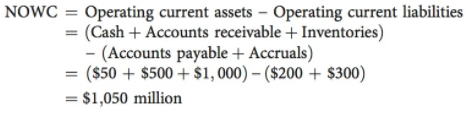

- Notice that each dollar of operating current liabilities is a dollar that the company does not have to raise from investors in order to conduct its short-term operating activities. Therefore, we define net operating working capital (NOWC) as operating current assets minus operating current liabilities. In other words, net operating working capital is the working capital acquired with investor-supplied funds. Here is the definition in equation form:

5. Total Net Operating Capital

- In addition to working capital, most companies also use long-term assets to support their operations. These include land, buildings, factories, equipment, and the like. Total net operating capital is the sum of NOWC and operating long-term assets:

![]()

2. Notice that we have defined total net operating capital as the sum of net operating working capital and operating long-term assets. In other words, our definition is in terms of operating assets and liabilities. However, we can also calculate total net operating capital by looking at the sources of funds. Total investor-supplied capital is defined as the total of funds provided by investors, such as notes payable, long-term bonds, preferred stock, and common equity. For most companies, total investor-supplied capital is:

6. Calculating Free Cash Flow

- Free Cash Flow is defined as:

![]()

or

7. The Uses of Free Cash Flow

- Recall that free cash flow (FCF) is the amount of cash that is available for distribution to all investors, including shareholders and debtholders. There are five good uses for FCF:

1. Pay interest to debtholders, keeping in mind that the net cost to the company is the after-tax interest expense.

2. Repay debt holders; that is, pay off some of the debt.

3. Pay dividends to shareholders.

4. Repurchase stock from shareholders.

5. Buy short-term investments or other nonoperating assets.

8. FCF and Corporate Value

- Free cash flow is the amount of cash available for distribution to investors; so the fundamental value of a company to its investors depends on the present value of its expected future FCFs, discounted at the company’s weighted average cost of capital (WACC). Subsequent chapters will develop the tools needed to forecast FCFs and evaluate their risk. FCF is the cash flow available for distribution to investors. Therefore, the fundamental value of a firm depends primarily on its expected future FCF.

Last modified: Tuesday, August 14, 2018, 8:38 AM