Reading: Lesson 5 - Federal Income Tax System

2.5.A - Corporate Income Taxes

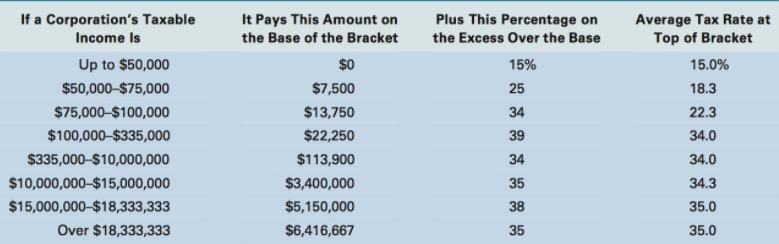

- The marginal tax rate is the rate paid on the last dollar of income, while the average tax rate is the average rate paid on all income.

- To illustrate, if a firm had $65,000 of taxable income, its tax bill would be Taxes

- Its marginal rate would be 25%, and its average tax rate would be $11,250/$65,000 = 17.3%. Note that corporate income above $18,333,333 has an average and marginal tax rate of 35%.

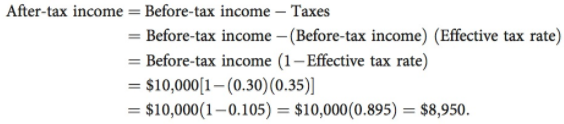

4. Interest income received by a corporation is taxed as ordinary income at regular corporate tax rates. However, 70% of the dividends received by one corporation from another are excluded from taxable income, while the remaining 30% are taxed at the ordinary tax rate.11 Thus, a corporation earning more than $18,333,333 and paying a 35% marginal tax rate would pay only (0.30)(0.35) = 0.105 = 10.5% of its dividend income as taxes, so its effective tax rate on dividends received would be 10.5%. If this firm had $10,000 in pre-tax dividend income, then its after-tax dividend income would be $8,950:

5. f the corporation pays its own after-tax income out to stockholders as dividends, then the income is ultimately subject to triple taxation: (1) the original corporation is first taxed, (2) the second corporation is then taxed on the dividends it received, and (3) the individuals who receive the final dividends are taxed again. This is the reason for the 70% exclusion on intercorporate dividends.

6. If a corporation has surplus funds that can be invested in marketable securities, the tax treatment favors investment in stocks, which pay dividends, rather than in bonds, which pay interest. For example, suppose Home Depot had $100,000 to invest, and suppose it could buy either bonds that paid interest of $8,000 per year or preferred stock that paid dividends of $7,000. Home Depot is in the 35% tax bracket; therefore, its tax on the interest, if it bought bonds, would be 0.35($8,000) = $2,800, and its after-tax income would be $5,200. If it bought preferred (or common) stock, its tax would be 0.35[(0.30) ($7,000)] = $735, and its after-tax income would be $6,265. Other factors might lead Home Depot to invest in bonds, but the tax treatment certainly favors stock investments when the investor is a corporation.

7. A firm’s operations can be financed with either debt or equity capital. If the firm uses debt, then it must pay interest on this debt, but if the firm uses equity, then it is expected to pay dividends to the equity investors (stockholders). The interest paid by a corporation is deducted from its operating income to obtain its taxable income, but dividends paid are not deductible. Therefore, a firm needs $1 of pre-tax income to pay $1 of interest, but if it is in the 40% federal-plus-state tax bracket, it must earn $1.67 of pre-tax income to pay $1 of dividends:

8. If a corporation owns 80% or more of another corporation’s stock, then it can aggregate income and file one consolidated tax return; thus, the losses of one company can be used to offset the profits of another. (Similarly, one division’s losses can be used to offset another division’s profits.) No business ever wants to incur losses (you can go broke losing $1 to save 35¢ in taxes), but tax offsets do help make it more feasible for large, multi-divisional corporations to undertake risky new ventures or ventures that will suffer losses during a developmental period.

9. Many U.S. corporations have overseas subsidiaries, and those subsidiaries must pay taxes in the countries where they operate. Often, foreign tax rates are lower than U.S. rates. As long as foreign earnings are reinvested overseas, no U.S. tax is due on those earnings. However, when foreign earnings are repatriated to the U.S. parent, they are taxed at the applicable U.S. rate, less a credit for taxes paid to the foreign country. As a result, U.S. corporations such as IBM, Coca-Cola, and Microsoft have been able to defer billions of dollars of taxes. This procedure has stimulated overseas investments by U.S. multinational firms—they can continue the deferral indefinitely, but only if they reinvest the earnings in their overseas operations.

10. Many U.S. corporations have overseas subsidiaries, and those subsidiaries must pay taxes in the countries where they operate. Often, foreign tax rates are lower than U.S. rates. As long as foreign earnings are reinvested overseas, no U.S. tax is due on those earnings. However, when foreign earnings are repatriated to the U.S. parent, they are taxed at the applicable U.S. rate, less a credit for taxes paid to the foreign country. As a result, U.S. corporations such as IBM, Coca-Cola, and Microsoft have been able to defer billions of dollars of taxes. This procedure has stimulated overseas investments by U.S. multinational firms—they can continue the deferral indefinitely, but only if they reinvest the earnings in their overseas operations.

2. Taxation of Small Businesses: S Corporations

- The Tax Code provides that small businesses that meet certain restrictions may be set up as corporations and thus receive the benefits of the corporate form of organization— especially limited liability—yet still be taxed as proprietorships or partnerships rather than as corporations. These corporations are called S corporations. (“Regular” corporations are called C corporations.) If a corporation elects S corporation status for tax purposes, then all of the business’s income is reported as personal income by its stockholders, on a pro rata basis, and thus is taxed at the rates that apply to individuals. This is an important benefit to the owners of small corporations in which all or most of the income earned each year will be distributed as dividends, because then the income is taxed only once, at the individual level.

3. Personal Taxes

- Ordinary income consists primarily of wages or profits from a proprietorship or partnership, plus investment income. For the 2012 tax year, individuals with less than $8,700 of taxable income are subject to a federal income tax rate of 10%. For those with higher income, tax rates increase and go up to 35%, depending on the level of income. This is called a progressive tax, because the higher one’s income, the larger the percentage paid in taxes.

- As noted before, individuals are taxed on investment income as well as earned income, but with a few exceptions and modifications. For example, interest received from most state and local government bonds, called municipals or munis, is not subject to federal taxation. However, interest earned on most other bonds or lending is taxed as ordinary income. This means that a lower-yielding muni can provide the same after-tax return as a higher-yielding corporate bond. For a taxpayer in the 35% marginal tax bracket, a muni yielding 5.5% provides the same after-tax return as a corporate bond with a pre-tax yield of 8.46%: 8.46%(1 − 0.35) = 5.5%.

- Assets such as stocks, bonds, and real estate are defined as capital assets. If you own a capital asset and its price goes up, then your wealth increases, but you are not liable for any taxes on your increased wealth until you sell the asset. If you sell the asset for more than you originally paid, the profit is called a capital gain; if you sell it for less, then you suffer a capital loss. The length of time you owned the asset determines the tax treatment. If held for less than 1 year, then your gain or loss is simply added to your other ordinary income. If held for more than a year, then gains are called long-term capital gains and are taxed at a lower rate.

- Under the 2003 tax law changes, dividends are now taxed as though they are capital gains. As stated earlier, corporations may deduct interest payments but not dividends when computing their corporate tax liability, which means that dividends are taxed twice, once at the corporate level and again at the personal level. This differential treatment motivates corporations to use debt relatively heavily and to pay small (or even no) dividends. The 2003 tax law did not eliminate the differential treatment of dividends and interest payments from the corporate perspective, but it did make the tax treatment of dividends more similar to that of capital gains from investors’ perspectives. To see this, consider a company that doesn’t pay a dividend but instead reinvests the cash it could have paid. The company’s stock price should increase, leading to a capital gain, which would be taxed at the same rate as the dividend. Of course, the stock price appreciation isn’t actually taxed until the stock is sold, whereas the dividend is taxed in the year it is paid, so dividends will still be more costly than capital gains for many investors.

- Note that the income of S corporations and noncorporate businesses is reported as income by the firms’ owners. Because there are far more S corporations, partnerships, and proprietorships than C corporations (which are subject to the corporate tax), individual tax considerations play an important role in business finance.

Остання зміна: вівторок 14 серпня 2018 08:38 AM