Reading: Lesson 6 - Compounding/Fractional Time Periods & Amortized Loans

4.6.A - Compounding/Fractional Time Periods & Amortized Loans

1. Semiannual and Other Compounding Periods

- In most of our examples thus far, we assumed that interest is compounded once a year, or annually. This is annual compounding. Suppose, however, that you put $1,000 into a bank that pays a 6% annual interest rate but credits interest each 6 months. This is semiannual compounding. If you leave your funds in the account, how much would you have at the end of 1 year under semiannual compounding? Note that you will receive $60 of interest for the year, but you will receive $30 of it after only 6 months and the other $30 at the end of the year. You will earn interest on the first $30 during the second 6 months, so you will end the year with more than the $60 you would have had under annual compounding. You would be even better off under quarterly, monthly, weekly, or daily compounding. Note also that virtually all bonds pay interest semiannually; most stocks pay dividends quarterly; most mortgages, student loans, and auto loans involve monthly payments; and most money fund accounts pay interest daily. Therefore, it is essential that you understand how to deal with non-annual compounding.

2. Types of Interest Rates

- When we move beyond annual compounding, we must deal with the following four types of interest rates:

• Nominal annual rates, given the symbol INOM

• Annual percentage rates, termed APR rates

• Periodic rates, denoted as IPER

• Effective annual rates, given the symbol EAR or EFF% - This is the rate quoted by banks, brokers, and other financial institutions. So, if you talk with a banker, broker, mortgage lender, auto finance company, or student loan officer about rates, the nominal rate is the one he or she will normally quote you. However, to be meaningful, the quoted nominal rate must also include the number of compounding periods per year. For example, a bank might offer you a CD at 6% compounded daily, while a credit union might offer 6.1% compounded monthly. Note that the nominal rate is never shown on a time line, and it is never used as an input in a financial calculator (except when compounding occurs only once a year). If more frequent compounding occurs, you must use periodic rates.

- This is the rate charged by a lender or paid by a borrower each period. It can be a rate per year, per 6 months (semiannually), per quarter, per month, per day, or per any other time interval. For example, a bank might charge 1.5% per month on its credit card loans, or a finance company might charge 3% per quarter on installment loans. We find the periodic rate as follows:

![]()

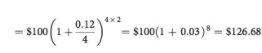

where INOM is the nominal annual rate and M is the number of compounding periods per year. Thus, a 6% nominal rate with semiannual payments results in a periodic rate of Periodic rate IPER 1⁄4 6%=2 1⁄4 3:00% If only one payment is made per year then M = 1, in which case the periodic rate would equal the nominal rate: 6%/1 = 6%. The periodic rate is the rate shown on time lines and used in calculations. To illustrate, suppose you invest $100 in an account that pays a nominal rate of 12%, compounded quarterly, or 3% per period. How much would you have after 2 years if you leave the funds on deposit? First, here is the time line for the problem:

To find the FV, we would use this modified version:

![]()

4. With a financial calculator, we find the FV using these inputs: N = 4 × 2 = 8, I = 12/4 = 3, PV = −100, and PMT = 0. The result is again FV = $126.68.

5. This is the annual (interest once a year) rate that produces the same final result as compounding at the periodic rate for M times per year. The EAR, also called EFF% (for effective percentage rate), is found as follows:

Here INOM/M is the periodic rate, N is the number of years, and M is the number of periods per year. If a bank would lend you money at a nominal rate of 12%, compounded quarterly, then the EFF% rate would be 12.5509%:

![]()

To see the importance of the EFF%, suppose that—as an alternative to the bank loan—you could borrow on a credit card that charges 1% per month. Would you be better off using the bank loan or credit card loan? To answer this question, the cost of each alternative must be expressed as an EFF%. We just saw that the bank loan’s effective cost is 12.5509%. The cost of the credit card loan, with monthly payments, is slightly higher, 12.6825%:

![]()

This result is logical: Both loans have the same 12% nominal rate, yet you would have to make the first payment after only 1 month on the credit card versus 3 months under the bank loan. The EFF% rate is rarely used in calculations. However, it must be used to compare the effective costs of different loans or rates of return on different investments when payment periods differ, as in our example of the credit card versus a bank loan.

3. Fractional Time Periods

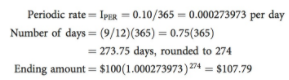

- So far we have assumed that payments occur at either the beginning or the end of periods, but not within periods. However, we occasionally encounter situations that require compounding or discounting over fractional periods. For example, suppose you deposited $100 in a bank that pays a nominal rate of 10%, compounded daily, based on a 365-day year. How much would you have after 9 months? The answer of $107.79 is found as follows:

Now suppose that instead you borrow $100 at a nominal rate of 10% per year and are charged simple interest, which means that interest is not charged on interest. If the loan is outstanding for 274 days (or 9 months), how much interest would you have to pay? The interest owed is equal to the principal multiplied by the interest rate times the number of periods. In this case, the number of periods is equal to a fraction of a year: N = 274/365 = 0.7506849.

![]()

Another approach would be to use the daily rate rather than the annual rate and thus to use the exact number of days rather than the fraction of the year:

![]()

You would owe the bank a total of $107.51 after 274 days. This is the procedure most banks use to calculate interest on loans, except that they generally require borrowers to pay the interest on a monthly basis rather than after 274 days; this more frequent compounding raises the EFF% and thus the total amount of interest paid.

4. Amortized Loans

- An extremely important application of compound interest involves loans that are paid off in installments over time. Included are automobile loans, home mortgage loans, student loans, and many business loans. A loan that is to be repaid in equal amounts on a monthly, quarterly, or annual basis is called an amortized loan.

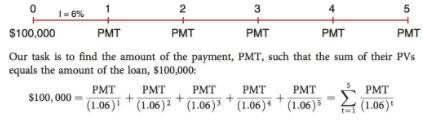

- Suppose a company borrows $100,000, with the loan to be repaid in 5 equal payments at the end of each of the next 5 years. The lender charges 6% on the balance at the beginning of each year. Here’s a picture of the situation:

With a financial calculator, we insert values as shown below to get the required payments, $23,739.64.

With Excel, you would use the PMT function: =PMT(I,N,PV,FV) = PMT(0.06,5,100000,0) = −$23,739.64. Thus, we see that the borrower must pay the lender $23,739.64 per year for the next 5 years.

5. Amortization Schedules

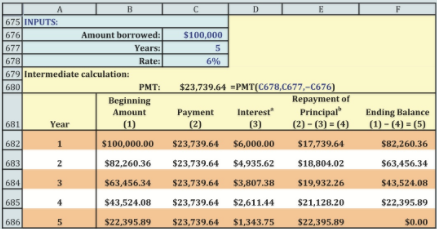

- Each payment will consist of two parts—part interest and part repayment of principal. This breakdown is shown in the amortization schedule given in the figure below. The interest component is relatively high in the first year, but it declines as the loan balance decreases. For tax purposes, the borrower would deduct the interest component while the lender would report the same amount as taxable income. Over the 5 years, the lender will earn 6% on its investment and also recover the amount of its invest

Остання зміна: вівторок 14 серпня 2018 08:41 AM