Reading: Lesson 3 - Semiannual Coupons & Bond Yields

5.3.A - Semiannual Coupons & Bond Yields

1. Bonds with Semiannual Coupons

- Although some bonds pay interest annually, the vast majority actually pay interest semi-annually. To evaluate semiannual payment bonds, we must modify the valuation model as follows.

1. Divide the annual coupon interest payment by 2 to determine the dollars of interest paid every 6 months.

2. Multiply the years to maturity, N, by 2 to determine the number of semiannual periods.

3. Divide the nominal (quoted) interest rate, rd, by 2 to determine the periodic (semiannual) interest rate.

By making these changes, we obtain the following equation for finding the value of a bond that pays interest semiannually:

![]()

2. To illustrate, assume now that a firm’s bonds pay $45 interest every 6 months rather than $90 at the end of each year. Each semiannual interest payment is only half as large, but there are twice as many of them. The nominal, or quoted, coupon rate is “9%, semiannual payments. When the going (nominal) rate of interest is 4% with semiannual compounding, the value of this 15-year bond is found as follows:

EnterN=30,rd =I/YR=2,PMT=45,FV=1000,and then press the PV key to obtain the bond’s value, $1,559.91. The value with semiannual interest payments is slightly larger than $1,552.92, the value when interest is paid annually. This higher value occurs because interest payments are received somewhat sooner under semiannual compounding.

2. Bond Yields

- Unlike the coupon interest rate, which is fixed, the bond’s yield varies from day to day depending on current market conditions. Moreover, the yield can be calculated in three different ways, and three “answers” can be obtained.

- Suppose 1 year after it was issued, you could buy a firm’s 14-year, 9% annual coupon, $1,000 par value bond at a price of $1,528.16. What rate of interest would you earn on your investment if you bought the bond and held it to maturity? This rate is called the bond’s yield to maturity (YTM), and it is the interest rate generally discussed by investors when they talk about rates of return. The yield to maturity is usually the same as the market rate of interest, rd. To find the YTM for a bond with annual interest payments, you must solve the above equation rd:

![]()

You could substitute values for rd until you found a value that “works” and forces the sum of the PVs on the right side of the equal sign to equal $1,528.16, but this would be tedious and time-consuming.9 As you might guess, it is much easier with a financial calculator. Here is the setup:

Simply enter N = 14, PV = −1,528.16, PMT = 90, and FV = 1000, and then press the I/YR key for the answer of 4%.

3. You could also find the YTM with a spreadsheet. In Excel, you would use the RATE function for this bond, inputting N = 14, PMT = 90, PV = −1528.16, FV = 1000, 0 for Type, and leave Guess blank: =RATE(14,90,−1528.16,1000,0). The result is 4%. The RATE function works only if the current date is immediately after either the issue date or a coupon payment date. To find bond yields on other dates, use Excel’s YIELD function.

4. The yield to maturity can be viewed as the bond’s promised rate of return, which is the return that investors will receive if all the promised payments are made. However, the yield to maturity equals the expected rate of return only if (1) the probability of default is zero and (2) the bond cannot be called. If there is some default risk or if the bond may be called, then there is some probability that the promised payments to maturity will not be received, in which case the calculated yield to maturity will differ from the expected return.

5. The YTM for a bond that sells at par consists entirely of an interest yield, but if the bond sells at a price other than its par value, then the YTM will consist of the interest yield plus a positive or negative capital gains yield. Note also that a bond’s yield to maturity changes whenever interest rates in the economy change, and this is almost daily. If you purchase a bond and hold it until it matures, you will receive the YTM that existed on the purchase date, but the bond’s calculated YTM will change frequently between the purchase date and the maturity date.

3. Yield to Call

- If you purchased a bond that was callable and the company called it, you would not have the option of holding the bond until it matured. Therefore, the yield to maturity would not be earned. For example, if a firm's 9% coupon bonds were callable and if interest rates fell from 9% to 4%, then the company could call in the 9% bonds, replace them with 4% bonds, and save $90 − $40 = $50 interest per bond per year. This would be good for the company but not for the bondholders.

- If current interest rates are well below an outstanding bond’s coupon rate, then a callable bond is likely to be called, and investors will estimate its expected rate of return as the yield to call (YTC) rather than as the yield to maturity. To calculate the YTC, solve this equation for rd:

Here N is the number of years until the company can call the bond, rd is the YTC, and “Call price” is the price the company must pay in order to call the bond (it is often set equal to the par value plus 1 year’s interest).

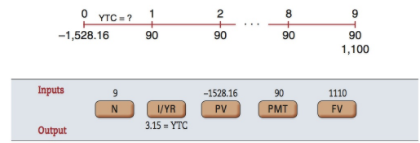

3. To illustrate, suppose a firm’s bonds had a provision that permitted the company, if it desired, to call the bonds 10 years after the issue date at a price of $1,100. Suppose further that 1 year after issuance the going interest rate had declined, causing the price of the bonds to rise to $1,528.16. Here is the time line and the setup for finding the bond’s YTC with a financial calculator:

The YTC is 3.15%—this is the return you would earn if you bought the bond at a price of $1,528.16 and it was called 9 years from today. (The bond could not be called until 10 years after issuance, and 1 year has gone by, so there are 9 years left until the first call date.)

4. Do you think the firm will call the bonds when they become callable? The firm’s actions depend on the going interest rate when the bonds become callable. If the going rate remains at rd = 4%, then the firm could save 9% − 4% = 5%, or $50 per bond per year, by calling them and replacing the 9% bonds with a new 4% issue. There would be costs to the company to refund the issue, but the interest savings would probably be worth the cost, so the firm would probably refund the bonds. Therefore, you would probably earn YTC = 3.15% rather than YTM = 4% if you bought the bonds under the indicated condition

4. Current Yield

- If you examine brokerage house reports on bonds, you will often see reference to a bond’s current yield. The current yield is the annual interest payment divided by the bond’s current price. For example, if a firm’s bonds with a 9% coupon were currently selling at $985, then the bond’s current yield would be $90/$985 = 0.0914 = 9.14%.

- Unlike the yield to maturity, the current yield does not represent the rate of return that investors should expect on the bond. The current yield provides information regarding the amount of cash income that a bond will generate in a given year, but it does not provide an accurate measure of the bond’s total expected return, the yield to maturity. In fact, here is the relation between current yield, capital gains yield (which can be negative for a capital loss), and the yield to maturity:

![]()

5. The Cost of Debt and Intrinsic Value

- The “Intrinsic Value Box” at the beginning of this chapter highlights the cost of debt, which affects the weighted average cost of capital (WACC), which in turn affects the company’s intrinsic value. The pre-tax cost of debt from the company’s perspective is the required return from the debtholder’s perspective. Therefore, the pre-tax cost of debt is the yield to maturity (or the yield to call if a call is likely). But why do different bonds have different yields to maturity? The following sections answer this question.

Last modified: Tuesday, August 14, 2018, 8:42 AM