Reading: Lesson 5 - Default Risk, Liquidity, & Maturity Risk Premium's

5.5.A - Default Risk, Liquidity, & Maturity Risk Premium's

1. Default Risk Premium

- If the issuer defaults on a payment, investors receive less than the promised return on the bond. The quoted interest rate includes a default risk premium (DRP)—the greater the default risk, the higher the bond’s yield to maturity.16 The default risk on Treasury securities is virtually zero, but default risk can be substantial for corporate and municipal bonds. In this section, we consider some issues related to default risk.

- Default risk is affected by both the financial strength of the issuer and the terms of the bond contract, especially whether collateral has been pledged to secure the bond.

- An indenture is a legal document that spells out the rights of both bondholders and the issuing corporation. A trustee is an official (usually a bank) who represents the bond- holders and makes sure the terms of the indenture are carried out. The indenture may be several hundred pages in length, and it will include restrictive covenants that cover such points as the conditions under which the issuer can pay off the bonds prior to maturity, the levels at which certain ratios must be maintained if the company is to issue additional debt, and restrictions against the payment of dividends unless earnings meet certain specifications. The Securities and Exchange Commission (1) approves indentures and (2) makes sure that all indenture provisions are met before allowing a company to sell new securities to the public. A firm will have different indentures for each of the major types of bonds it issues, but a single indenture covers all bonds of the same type. For example, one indenture will cover a firm’s first mortgage bonds, another its debentures, and a third its convertible bonds.

- A corporation pledges certain assets as security for a mortgage bond. The company might also choose to issue second-mortgage bonds secured by the same assets that were secured by a previously issued mortgage bond. In the event of liquidation, the holders of these second mortgage bonds would have a claim against the property, but only after the first mortgage bondholders had been paid off in full. Thus, second mortgages are sometimes called junior mortgages because they are junior in priority to the claims of senior mortgages, or first-mortgage bonds. All mortgage bonds are subject to an indenture that usually limits the amount of new bonds that can be issued.

- A debenture is an unsecured bond, and as such it provides no lien against specific property as security for the obligation. Debenture holders are, therefore, general creditors whose claims are protected by property not otherwise pledged. The term subordinate means “below” or “inferior to”; thus, in the event of bankruptcy, subordinated debt has claims on assets only after senior debt has been paid off. Subordinated debentures may be subordinated either to designated notes payable (usually bank loans) or to all other debt. In the event of liquidation or reorganization, holders of subordinated debentures cannot be paid until all senior debt, as named in the debentures’ indentures, has been paid.

- Some companies may be in a position to benefit from the sale of either development bonds or pollution control bonds. State and local governments may set up both industrial development agencies and pollution control agencies. These agencies are allowed, under certain circumstances, to sell tax-exempt bonds and then make the proceeds available to corporations for specific uses deemed (by Congress) to be in the public interest. For example, a Detroit pollution control agency might sell bonds to provide Ford with funds for purchasing pollution control equipment. Because the income from the bonds would be tax exempt, the bonds would have relatively low interest rates. Note, however, that these bonds are guaranteed by the corporation that will use the funds, not by a governmental unit, so their rating reflects the credit strength of the corporation using the funds.

- Municipalities can have their bonds insured, which means that an insurance company guarantees to pay the coupon and principal payments should the issuer default. This reduces risk to investors, who will thus accept a lower coupon rate for an insured bond than for a comparable but uninsured one. Even though the municipality must pay a fee to have its bonds insured, its savings due to the lower coupon rate often make insurance cost-effective. Keep in mind that the insurers are private companies, and the value added by the insurance depends on the creditworthiness of the insurer. The larger insurers are strong companies, and their own ratings are AAA.

2. Bond Ratings

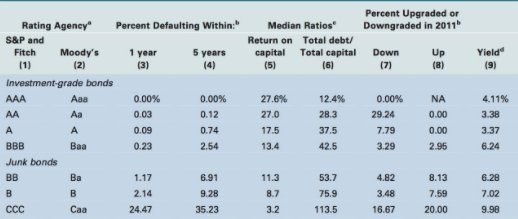

- Since the early 1900s, bonds have been assigned quality ratings that reflect their probability of going into default. The three major rating agencies are Moody’s Investors Service (Moody’s), Standard & Poor’s Corporation (S&P), and Fitch Ratings. As shown in Columns (3) and (4) of the Table below, triple-A and double-A bonds are extremely safe, rarely defaulting even within 5 years of being assigned a rating. Single-A and triple-B bonds are also strong enough to be called investment-grade bonds, and they are the lowest-rated bonds that many banks and other institutional investors are permitted by law to hold. Double-B and lower bonds are speculative bonds and are often called junk bonds. These bonds have a significant probability of defaulting.

3. Bond Rating Criteria, Upgrades, and Downgrades

- Financial Ratios. Many ratios potentially are important, but the return on invested capital, debt ratio, and interest coverage ratio are particularly valuable for predicting financial distress. For example, Columns (1), (5), and (6) in the Table above show a strong relationship between ratings and the return on capital and the debt ratio.

- Bond Contract Terms. Important provisions for determining the bond’s rating include whether the bond is secured by a mortgage on specific assets, whether the bond is subordinated to other debt, any sinking fund provisions, guarantees by some other party with a high credit ranking, and restrictive covenants such as requirements that the firm keep its debt ratio below a given level or that it keep its times interest earned ratio above a given level.

- Qualitative Factors. Included here would be such factors as sensitivity of the firm’s earnings to the strength of the economy, how it is affected by inflation, whether it is having or is likely to have labor problems, the extent of its international operations (including the stability of the countries in which it operates), potential environmental problems, potential antitrust problems, and so on. Today, a critical factor is exposure to sub-prime loans, including the difficulty of determining the extent of this exposure owing to the complexity of the assets backed by such loans.

- Rating agencies review outstanding bonds on a periodic basis and re-rate if necessary. Columns (7) and (8) in the Table above show the percentages of companies in each rating category that were downgraded or upgraded in 2011 by Fitch Ratings. The year 2011 was a difficult one, as more bonds were downgraded than upgraded.

- Over the long run, ratings agencies have done a reasonably good job of measuring the average credit risk of bonds and of changing ratings whenever there is a significant change in credit quality. However, it is important to understand that ratings do not adjust immediately to changes in credit quality, and in some cases there can be a considerable lag between a change in credit quality and a change in rating. For example, Enron’s bonds still carried an investment-grade rating on a Friday in December 2001, but the company declared bankruptcy two days later, on Sunday. Many other abrupt downgrades occurred in 2007 and 2008, leading to calls by Congress and the SEC for changes in rating agencies and the way they rate bonds. Clearly, improvements can be made, but there will always be occasions when completely unexpected information about a company is released, leading to a sudden change in its rating.

4. Bond Ratings and the Default Risk Premium

- Why are bond ratings so important? First, most bonds are purchased by institutional investors rather than individuals, and many institutions are restricted to investment-grade securities. Thus, if a firm’s bonds fall below BBB, it will have a difficult time selling new bonds because many potential purchasers will not be allowed to buy them. Second, many bond covenants stipulate that the coupon rate on the bond automatically increases if the rating falls below a specified level. Third, because a bond’s rating is an indicator of its default risk, the rating has a direct, measurable influence on the bond’s yield. Column (9) of the Table above shows that an AA bond has a yield of 3.38% and that yields increase as the rating falls. In fact, an investor would earn 9.98% on a CCC bond if it didn’t default.

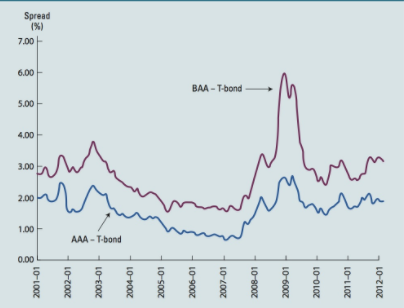

- A bond spread is the difference between a bond’s yield and the yield on some other security of the same maturity. Unless specified differently, the term “spread” generally means the difference between a bond’s yield and the yield on a Treasury bond of similar maturity.

- The figure above shows the spreads between an index of AAA bonds and a 10-year Treasury bond; it also shows spreads for an index of BBB bonds relative to the T-bond. Figure below illustrates three important points. First, the BAA spread always is greater than the AAA spread. This is because a BAA bond is riskier than an AAA bond, so BAA investors require extra compensation for their extra risk. The same is true for other ratings: Lower-rated bonds have higher yields.

- Second, the spreads are not constant over time. For example, look at the AAA spread. It was exceptionally low during the boom years of 2005–2007 but rose dramatically as the economy declined in 2008 and 2009.

- Third, the difference between the BAA spread and the AAA spread isn’t constant over time. The two spreads were quite close to one another in early 2000 but were very far apart in early 2009. In other words, BAA investors didn’t require much extra return over that of an AAA bond to induce them to take on that extra risk most years, but in 2009 they required a very large risk premium.

- Not only do spreads vary with the rating of the security, they also usually increase as maturity increases. This should make sense. If a bond matures soon, investors are able to forecast the company’s performance fairly well. But if a bond has a long time until it matures, investors have a difficult time forecasting the likelihood that the company will fall into financial distress. This extra uncertainty creates additional risk, so investors demand a higher required return.

5. The Liquidity Risk Premium

- A “liquid” asset can be converted to cash quickly and at a “fair market value.” Financial assets are generally more liquid than real assets. Because liquidity is important, investors include liquidity premiums (LPs) when market rates of securities are established. Although liquidity premiums are difficult to measure accurately, a differential of at least 2 percentage points (and perhaps up to 4 or 5 percentage points) exists between the least liquid and the most liquid financial assets of similar default risk and maturity. Corporate bonds issued by small companies are traded less frequently than those issued by large companies, so small-company bonds tend to have a higher liquidity premium.

6. The Maturity Risk Premium (MRP)

- All bonds, even Treasury bonds, are exposed to two additional sources of risk: interest rate risk and reinvestment risk. The net effect of these two sources of risk upon a bond’s yield is called the maturity risk premium, MRP. The following sections explain how interest rate risk and reinvestment risk affect a bond’s yield.

- Interest rates go up and down over time, and an increase in interest rates leads to a decline in the value of outstanding bonds. This risk of a decline in bond values due to rising interest rates is called interest rate risk. To illustrate, suppose you bought some 9% bonds at a price of $1,000, and then interest rates rose in the following year to 14%. As we saw earlier, the price of the bonds would fall to $692.89, so you would have a loss of $307.11 per bond.17 Interest rates can and do rise, and rising rates cause a loss of value for bondholders. Thus, bond investors are exposed to risk from changing interest rates. This point can be demonstrated by showing how the value of a 1-year bond with a 10% annual coupon fluctuates with changes in rd and then comparing these changes with those on a 25-year bond. The 1-year bond’s value for rd = 5% is shown below:

3. Using either a calculator or a spreadsheet, you could calculate the bond values for a 1-year and a 25-year bond at several current market interest rates; these results are plotted in the Figure below. Note how much more sensitive the price of the 25-year bond is to changes in interest rates. At a 10% interest rate, both the 25-year and the 1-year bonds are valued at $1,000. When rates rise to 15%, the 25-year bond falls to $676.79 but the 1-year bond falls only to $956.52.

4. For bonds with similar coupons, this differential sensitivity to changes in interest rates always holds true: The longer the maturity of the bond, the more its price changes in response to a given change in interest rates. Thus, even if the risk of default on two bonds is exactly the same, the one with the longer maturity is exposed to more risk from a rise in interest rates.

5. The explanation for this difference in interest rate risk is simple. Suppose you bought a 25-year bond that yielded 10%, or $100 a year. Now suppose interest rates on bonds of comparable risk rose to 15%. You would be stuck with only $100 of interest for the next 25 years. On the other hand, had you bought a 1-year bond, you would have a low return for only 1 year. At the end of the year, you would get your $1,000 back, and you could then reinvest it and receive a 15% return ($150) for the next year. Thus, interest rate risk reflects the length of time one is committed to a given investment.

6. In addition to maturity, interest rate sensitivity reflects the size of coupon payments. Intuitively, this is because more of a high-coupon bond’s value is received sooner than that of a low-coupon bond of the same maturity. This intuitive concept is measured by “duration,” which finds the average number of years that the bond’s PV of cash flows (coupons and principal payments) remains outstanding. A zero coupon bond, which has no payments until maturity, has a duration equal to its maturity. Coupon bonds have durations that are shorter than maturity, and the higher the coupon rate, the shorter the duration. Duration measures a bond’s sensitivity to interest rates in the following sense: Given a change in interest rates, the percentage change in a bond’s price is proportional to its duration:

![]()

7. Reinvestment Rate Risk

- As we saw in the preceding section, an increase in interest rates will hurt bondholders because it will lead to a decline in the value of a bond portfolio. But can a decrease in interest rates also hurt bondholders? The answer is “yes,” because if interest rates fall then a bondholder may suffer a reduction in his or her income. For example, consider a retiree who has a portfolio of bonds and lives off the income they produce. The bonds, on average, have a coupon rate of 10%. Now suppose that interest rates decline to 5%. The short-term bonds will mature, and when they do, they will have to be replaced with lower- yielding bonds. In addition, many of the remaining long-term bonds may be called, and as calls occur, the bondholder will have to replace 10% bonds with 5% bonds. Thus, our retiree will suffer a reduction of income.

- The risk of an income decline due to a drop in interest rates is called reinvestment rate risk. Reinvestment rate risk is obviously high on callable bonds. It is also high on short-maturity bonds, because the shorter the maturity of a bond, the fewer the years when the relatively high old interest rate will be earned and the sooner the funds will have to be reinvested at the new low rate. Thus, retirees whose primary holdings are short-term securities, such as bank CDs and short-term bonds, are hurt badly by a decline in rates, but holders of long-term bonds continue to enjoy their old high rates.

8. Comparing Interest Rate Risk and Reinvestment Rate Risk: The Maturity Risk Premium

- Note that interest rate risk relates to the value of the bonds in a portfolio, while reinvestment rate risk relates to the income the portfolio produces. If you hold long- term bonds then you will face a lot of interest rate risk, because the value of your bonds will decline if interest rates rise; but you will not face much reinvestment rate risk, so your income will be stable. On the other hand, if you hold short-term bonds, you will not be exposed to much interest rate risk because the value of your portfolio will be stable, but you will be exposed to considerable reinvestment rate risk because your income will fluctuate with changes in interest rates. We see, then, that no fixed-rate bond can be considered totally riskless—even most Treasury bonds are exposed to both interest rate risk and reinvestment rate risk.

- Bond prices reflect the trading activities of the marginal investors, defined as those who trade often enough and with large enough sums to determine bond prices. Although one particular investor might be more averse to reinvestment risk than to interest rate risk, the data suggest that the marginal investor is more averse to interest rate risk than to reinvestment risk. To induce the marginal investor to take on interest rate risk, long-term bonds must have a higher expected rate of return than short-term bonds. Holding all else equal, this additional return is the maturity risk premium (MRP).

9. Term Structure of Interest Rates

- The term structure of interest rates describes the relationship between long-term and short-term rates. The term structure is important both to corporate treasurers deciding whether to borrow by issuing long-term or short-term debt and to investors who are deciding whether to buy long-term or short-term bonds.

- Interest rates for bonds with different maturities can be found in a variety of publications, including The Wall Street Journal and the Federal Reserve Bulletin, as well as on a number of Web sites, including Bloomberg, Yahoo!, CNN Financial, and the Federal Reserve Board. Using interest rate data from these sources, we can determine the term structure at any given point in time. For example, the Figure below presents interest rates for different maturities on three different dates. The set of data for a given date, when plotted on a graph such as the Figure above, is called the yield curve for that date.

- As the figure shows, the yield curve changes both in position and in slope over time. In March 1980, all rates were quite high because high inflation was expected. However, the rate of inflation was expected to decline, so the inflation premium (IP) was larger for short-term bonds than for long-term bonds. This caused short-term yields to be higher than long-term yields, resulting in a downward-sloping yield curve. By February 2000, inflation had indeed declined and thus all rates were lower. The yield curve had become humped—medium-term rates were higher than either short- or long-term rates. In March 2012, all rates were below the 2000 levels. Because short-term rates had dropped below long-term rates, the yield curve was upward sloping.

- Historically, long-term rates are generally higher than short-term rates owing to the maturity risk premium, so the yield curve usually slopes upward. For this reason, people often call an upward-sloping yield curve a “normal” yield curve and a yield curve that slopes downward an inverted, or “abnormal,” curve. Thus, in Figure below the yield curve for March 1980 was inverted, whereas the yield curve in March 2012 was normal. As stated above, the February 2000 curve was humped.

- A few academics and practitioners contend that large bond traders who buy and sell securities of different maturities each day dominate the market. According to this view, a bond trader is just as willing to buy a 30-year bond to pick up a short-term profit as to buy a 3-month security. Strict proponents of this view argue that the shape of the yield curve is therefore determined only by market expectations about future interest rates, a position that is called the pure expectations theory, or sometimes just the expectations theory. If this were true, then the maturity risk premium (MRP) would be zero and long-term interest rates would simply be a weighted average of current and expected future short-term interest rates.

5.5.B - Watch the Default Risk and Bond Rating video

Video:

(Default Risk and Bond Premium, 2:29 min)

Last modified: Tuesday, August 14, 2018, 8:43 AM