Reading: Lesson 1 - The Weight Average Cost of Capital

8.1.A - The Weight Average Cost of Capital

1. Corporate Valuation and the Cost of Capital

- Businesses require capital to develop new products, build factories and distribution centers, install information technology, expand internationally, and acquire other companies. For each of these actions, a company must estimate the total investment required and then decide whether the expected rate of return exceeds the cost of the capital. The cost of capital is also a factor in compensation plans, with bonuses dependent on whether the company’s return on invested capital exceeds the cost of that capital. This cost is also a key factor in choosing the firm’s mixture of debt and equity and in decisions to lease rather than buy assets. As these examples illustrate, the cost of capital is a critical element in many business decisions.

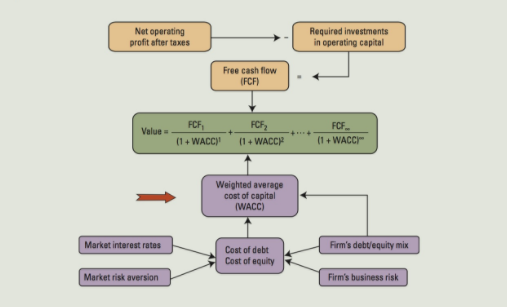

- Earlier we told you that managers should strive to make their firms more valuable and that the value of a firm is determined by the size, timing, and risk of its free cash flows (FCF). Indeed, a firm’s intrinsic value is estimated as the present value of its FCFs, discounted at the weighted average cost of capital (WACC). In previous chapters, we examined the major sources of financing (stocks, bonds, and preferred stock) and the costs of those instruments. In this chapter, we put those pieces together and estimate the WACC that is used to determine intrinsic value.

2. The Weighted Average Cost of Capital

- The value of a company’s operations is the present value of the expected free cash flows (FCF) discounted at the weighted average cost of capital (WACC):

We defined free cash flows (FCF), explained how to find present values, and used the valuation equation in earlier sections. Now we define the weighted average cost of capital (WACC):

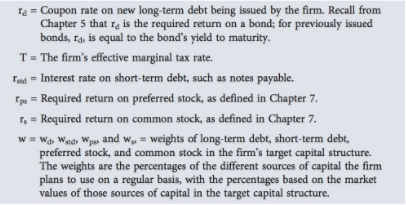

Some of these variables should be familiar to you from previous sections, but some are new. All are defined as follows:

We explain how to estimate the WACC of a specific company, MicroDrive, Inc., but let’s begin with a few general concepts. First, companies are financed by several sources of investor-supplied capital, which are called capital components. We have included short-term debt and preferred stock because some companies use them as sources of funding, but most companies only use two major sources of investor-supplied capital, long-term debt, and common stock.

Second, investors providing the capital components require rates of return (rd, rstd, rps, and rs) commensurate with the risks of the components in order to induce them to make the investments. Previous chapters defined those required returns from an investor’s view, but those returns are costs from a company’s viewpoint. This is why we call the WACC a cost of capital.

Third, recall that FCF is the cash flow available for distribution to all investors. Therefore, the free cash flows must provide an overall rate of return sufficient to compensate investors for their exposure to risk. Intuitively, it makes sense that this overall return should be a weighted average of the capital components’ required returns. This intuition is confirmed by applying algebra to the definitions of required returns, free cash flow, and the value of operations: The discount rate used in the Equation above is equal to the WACC as defined also in the Equation above. In other words, the correct rate for estimating the present value of a company’s (or project’s) cash flows is the weighted average cost of capital.

3. Choosing Weights for the Weighted Average Cost of Capital

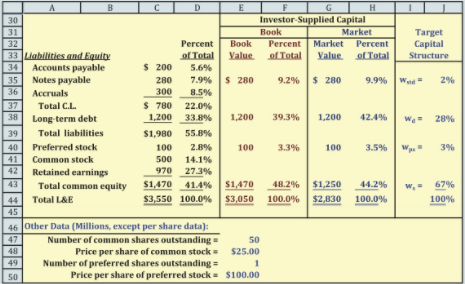

- The Figure below selected data for MicroDrive, Inc., including: (1) liabilities and equity (L&E) from the balance sheets; (2) percentages of total L&E comprised by each liability or equity account; (3) book values (as reported on the balance sheets) and percentages of financing from investor-supplied capital; (4) current market values and percentages of financing from investor-supplied capital; and (5) target capital structure weights.

- Notice that we exclude accounts payable and accruals from capital structure weights. Capital is provided by investors—interest-bearing debt, preferred stock, and common equity. Accounts payable and accruals arise from operating decisions, not from financing decisions. Recall that the impact of payables and accruals is incorporated into a firm’s free cash flows and a project’s cash flows rather than into the cost of capital. Therefore, we consider only investor-supplied capital when discussing capital structure weights.

- The Figure below reports percentages of financing based on book values, market values, and target weights. Book values are a record of the cumulative amounts of capital supplied by investors over the life of the company. For equity, stockholders have supplied capital directly when MicroDrive issued stock, but they have also supplied capital indirectly when MicroDrive retained earnings instead of paying bigger dividends. The WACC is used to find the present value of future cash flows, so it would be inconsistent to use weights based on the past history of the company.

- Stock prices are volatile, so current market values of total common equity often change dramatically from day to day. Companies certainly don’t try to maintain the weights in their capital structures daily by issuing stock, repurchasing stock, issuing debt, or repaying debt in response to changes in their stock price. Therefore, the capital structure weights based on the current market values might not be a good estimate of the capital structure that the company will have on average during the future.

- The target capital structure is defined as the average capital structure weights (based on market values) that a company will have during the future. MicroDrive has chosen a target capital structure composed of 2% short-term debt, 28% long-term debt, 3% preferred stock, and 67% common equity. MicroDrive presently has more debt in its actual capital structure (using either book values or market values), but it intends to move towards its target capital structure in the near future.

Last modified: Tuesday, August 14, 2018, 8:50 AM