Reading: Lesson 6 - Corporate Governance

10.6.A - Corporate Governance

1. Corporate Governance

- Agency conflicts can decrease the value of stock owned by outside shareholders. Corporate governance can mitigate this loss in value. Corporate governance can be defined as the set of laws, rules, and procedures that influence a company’s operations and the decisions its managers make. At the risk of oversimplification, most corporate governance provisions come in two forms, sticks and carrots. The primary stick is the threat of removal, either as a decision by the board of directors or as the result of a hostile takeover. If a firm’s managers are maximizing the value of the resources entrusted to them, they need not fear the loss of their jobs. On the other hand, if managers are not maximizing value, they should be removed by their own boards of directors, by dissident stockholders, or by other companies seeking to profit by installing a better management team. The main carrot is compensation. Managers have greater incentives to maximize intrinsic stock value if their compensation is linked to the firm’s performance rather than being strictly in the form of salary.

- Almost all corporate governance provisions affect either the threat of removal or compensation. Some provisions are internal to a firm and are under its control.3 These internal provisions and features can be divided into five areas: (1) monitoring and discipline by the board of directors, (2) charter provisions and bylaws that affect the likelihood of hostile takeovers, (3) compensation plans, (4) capital structure choices, and (5) accounting control systems. In addition to the corporate governance provisions that are under a firm’s control, there are also environmental factors outside of a firm’s control, such as the regulatory environment, block ownership patterns, competition in the product markets, the media, and litigation. Our discussion begins with the internal provisions.

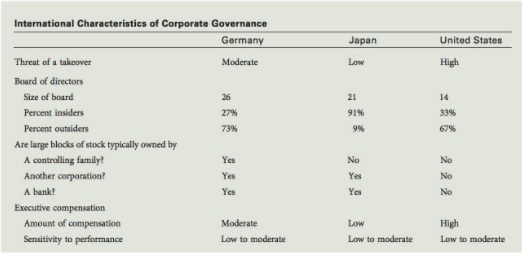

- Shareholders are a corporation’s owners, and they elect the board of directors to act as agents on their behalf. In the United States, it is the board’s duty to monitor senior managers and discipline them if they do not act in the interests of shareholders, either by removal or by a reduction in compensation.4 This is not necessarily the case outside the United States. For example, many companies in Europe are required to have employee representatives on the board. Also, many European and Asian companies have bank representatives on the board. But even in the United States, many boards fail to act in the shareholders’ best interests. How can this be?

- Consider the election process. The board of directors has a nominating committee. These directors choose the candidates for the open director positions, and the ballot for a board position usually lists only one candidate. Although outside candidates can run a “write-in” campaign, only those candidates named by the board’s nominating committee are on the ballot.5 At many companies, the CEO is also the chairman of the board and has considerable influence on this nominating committee. This means that in practice it often is the CEO who, in effect, nominates candidates for the board. High compensation and prestige go with a position on the board of a major company, so board seats are prized possessions. Board members typically want to retain their positions, and they are grateful to whoever helped get them on the board. Thus, the nominating process often results in a board that is favorably disposed to the CEO.

- At most companies, a candidate is elected simply by having a majority of votes cast. The proxy ballot usually lists all candidates, with a box for each candidate to check if the shareholder votes “For” the candidate and a box to check if the shareholder “Withholds” a vote on the candidate—you can’t actually vote “No”; you can only withhold your vote. In theory, a candidate could be elected with a single “For” vote if all other votes were withheld. In practice, though, most shareholders either vote “For” or assign to management their right to vote (proxy is defined as the authority to act for another, which is why it is called a proxy statement). In practice, then, the nominated candidates virtually always receive a majority of votes and are thus elected.

- Occasionally there is a “Just vote no” campaign in which a large investor (usually an institution such as a pension fund) urges stockholders to withhold their votes for one or more directors. Although such campaigns do not directly affect the director’s election, they do provide a visible way for investors to express their dissatisfaction. Recent evidence shows that “Just vote no” campaigns at poorly performing firms lead to better performance and a greater probability that the CEO will be dismissed.

- Voting procedures also affect the ability of outsiders to gain positions on the board. If the charter specifies cumulative voting, then each shareholder is given a number of votes equal to his or her shares multiplied by the number of board seats up for election. For example, the holder of 100 shares of stock will receive 1,000 votes if 10 seats are to be filled. Then, the shareholder can distribute those votes however he or she sees fit. One hundred votes could be cast for each of 10 candidates, or all 1,000 votes could be cast for one candidate. If noncumulative voting is used, the hypothetical stockholder cannot concentrate votes in this way—no more than 100 votes can be cast for any one candidate.

- Voting procedures also affect the ability of outsiders to gain positions on the board. If the charter specifies cumulative voting, then each shareholder is given a number of votes equal to his or her shares multiplied by the number of board seats up for election. For example, the holder of 100 shares of stock will receive 1,000 votes if 10 seats are to be filled. Then, the shareholder can distribute those votes however he or she sees fit. One hundred votes could be cast for each of 10 candidates, or all 1,000 votes could be cast for one candidate. If noncumulative voting is used, the hypothetical stockholder cannot concentrate votes in this way—no more than 100 votes can be cast for any one candidate.

- With noncumulative voting, if management controls 51% of the shares, then they can fill every seat on the board, leaving dissident stockholders without any representation on the board. With cumulative voting, however, if 10 seats are to be filled, then dissidents could elect a representative, provided they have 10% plus 1 additional share of the stock.

- Note also that bylaws specify whether the entire board is to be elected annually or if directors are to have staggered terms with, say, one-third of the seats to be filled each year and directors to serve 3-year terms. With staggered terms, fewer seats come up each year, making it harder for dissidents to gain representation on the board. Staggered boards are also called classified boards.

- Many board members are “insiders”—that is, people who hold managerial positions within the company, such as the CFO. Because insiders report to the CEO, it may be difficult for them to oppose the CEO at a board meeting. To help mitigate this problem, several exchanges, such as the NYSE and NASDAQ, now require that listed companies have a majority of outside directors.

- Some “outside” board members often have strong connections with the CEO through professional relationships, personal friendships, and consulting or other fee-generating activities. In fact, outsiders sometimes have very little expert business knowledge but have “celebrity” status from non-business activities. Some companies also have interlocking boards of directors, where Company A’s CEO sits on Company B’s board and B’s CEO sits on A’s board. In these situations, even the outside directors are not truly independent and impartial.

- Large boards (those with more than about ten members) often are less effective than smaller boards. As anyone who has been on a committee can attest, individual participation tends to fall as committee size increases. Thus, there is a greater likelihood that members of a large board will be less active than those on smaller boards.

- The compensation of board members has an impact on the board’s effectiveness. When board members have exceptionally high compensation, the CEO also tends to have exceptionally high compensation. This suggests that such boards tend to be too lenient with the CEO.7 The form of board compensation also affects board performance. Rather than compensating board members with only salary, many companies now include restricted stock grants or stock options in an effort to better align board members with stockholders.

- Studies show that corporate governance usually improves if (1) the CEO is not also the chairman of the board, (2) the board has a majority of true outsiders who bring some type of business expertise to the board and are not too busy with other activities, (3) the board is not too large, and (4) board members are compensated appropriately (not too high and not all cash, but including exposure to equity risk through options or stock). The good news for the shareholder is that the boards at many companies have made significant improvements in these directions during the past decade. Fewer CEOs are also board chairmen and, as power has shifted from CEOs to boards as a whole, there has been a tendency to replace insiders with strong, independent outsiders. Today, the typical board has about one-third insiders and two-thirds outsiders, and most outsiders are truly independent. Moreover, board members are compensated primarily with stock or options rather than a straight salary. These changes clearly have decreased the patience of boards with poorly performing CEOs. Within the past several years the CEOs of Wachovia, Sprint Nextel, Gap, Hewlett-Packard, Home Depot, Citigroup, Pfizer, Ford, and Dynegy, to name just a few, have been removed by their boards. This would not have occurred 30 years ago.

2. Charter Provisions and Bylaws That Affect the Likelihood of Hostile Takeovers

- Hostile takeovers usually occur when managers have not been willing or able to maximize the profit potential of the resources under their control. In such a situation, another company can acquire the poorly performing firm, replace its managers, increase free cash flow, and improve MVA. The following paragraphs describe some provisions that can be included in a corporate charter to make it harder for poorly performing managers to remain in control.

- A shareholder-friendly charter should ban targeted share repurchases, also known as greenmail. For example, suppose a company’s stock is selling for $20 per share. Now a hostile bidder, or raider, who plans to replace management if the takeover is successful, buys 5% of the company’s stock at the $20 price. The raider then makes an offer to purchase the remainder of the stock for $30 per share. The company might offer to buy back the raider’s stock at a price of, say, $35 per share. This is called a targeted share repurchase because the stock will be purchased only from the raider and not from any other shareholders. A raider who paid only $20 per share for the stock would be making a quick profit of $15 per share, which could easily total several hundred million dollars. As a part of the deal, the raider would sign a document promising not to attempt to take over the company for a specified number of years; hence the buyback also is called greenmail. Greenmail hurts shareholders in two ways. First, they are left with $20 stock when they could have received $30 per share. Second, the company purchased stock from the bidder at $35 per share, which represents a direct loss by the remaining shareholders of $15 for each repurchased share.

- Managers who buy back stock in targeted repurchases typically argue that their firms are worth more than the raiders offered and that, in time, the “true value” will be revealed in the form of a much higher stock price. This situation might be true if a company were in the process of restructuring itself, or if new products with high potential were in the pipeline. But if the old management had been in power for a long time and had a history of making empty promises, then one should question whether the true purpose of the buyback was to protect stockholders or management.

- Another characteristic of a stockholder-friendly charter is that it does not contain a shareholder rights provision, better described as a poison pill. These provisions give the shareholders of target firms the right to buy a specified number of shares in the company at a very low price if an outside group or firm acquires a specified percentage of the firm’s stock. Therefore, if a potential acquirer tries to take over a company, its other shareholders will be entitled to purchase additional shares of stock at a bargain price, thus seriously diluting the holdings of the raider. For this reason, these clauses are called poison pills, because if they are in the charter, the acquirer will end up swallowing a poison pill if the acquisition is successful. Obviously, the existence of a poison pill makes a takeover more difficult, and this helps to entrench management.

- A third management entrenchment tool is a restricted voting rights provision, which automatically cancels the voting rights of any shareholder who owns more than a specified amount of the company’s stock. The board can grant voting rights to such a shareholder, but this is unlikely if that shareholder plans to take over the company.

3. Using Compensation to Align Managerial and Shareholder Interests

- The typical CEO today receives a fixed salary, a cash bonus based on the firm’s performance, and stock-based compensation, either in the form of stock grants or option grants. Cash bonuses often are based upon short-term operating factors, such as this year’s growth in earnings per share, or medium-term operating performance, such as earnings growth over the past 3 years.

- Stock-based compensation is often in the form of options. Section 8 explains option valuation in detail, but here we discuss how a standard stock option compensation plan works. Suppose IBM decides to grant an option to an employee, allowing her to purchase a specified number of IBM shares at a fixed price, called the strike price (or exercise price), regardless of the actual price of the stock. The strike price is usually set equal to the current stock price at the time the option is granted. Thus, if IBM’s current price were $100, then the option would have an exercise price of $100. Options usually cannot be exercised until after some specified period (the vesting period), which is usually 1 to 5 years. Some grants have cliff vesting, which means that all the granted options vest at the same date, such as 3 years after the grant. Other grants have annual vesting, which means that a certain percentage vests each year. For example, one-third of the options in the grant might vest each year. The options have an expiration date, usually 10 years after issue. For our IBM example, assume that the options have cliff vesting in 3 years and have an expiration date in 10 years. Thus, the employee can exercise the option 3 years after issue or wait as long as 10 years. Of course, the employee would not exercise unless IBM’s stock is above the $100 exercise price, and if the price never rose above $100, the option would expire unexercised. However, if the stock price were above $100 on the expiration date, the option would surely be exercised.

- Suppose the stock price had grown to $134 after 5 years, at which point the employee decided to exercise the option. She would buy stock from IBM for $100, so IBM would get only $100 for stock worth $134. The employee would (probably) sell the stock the same day she exercised the option and hence would receive in cash the $34 difference between the $134 stock price and the $100 exercise price. There are two important points to note in this example. First, most employees sell stock soon after exercising the option. Thus, the incentive effects of an option grant typically end when the option is exercised. Second, option pricing theory shows that it is not optimal to exercise a conventional call option on stock that does not pay dividends before the option expires: An investor is always better off selling the option in the marketplace rather than exercising it. But because employee stock options are not tradable, grantees often exercise the options well before they expire. For example, people often time the exercise of options to the purchase of a new home or some other large expenditure. But early exercise occurs not just for liquidity reasons, such as needing cash to purchase a house, but also because of behavioral reasons. For example, exercises occur more frequently after stock run-ups, which suggests that grantees view the stock as overpriced. In theory, stock options should align a manager’s interests with those of shareholders, influencing the manager to behave in a way that maximizes the company’s value. But in practice there are two reasons why this does not always occur.

- First, suppose a CEO granted options on 1 million shares. If we use the same stock prices as in our previous example, then the grantee would receive $34 for each option, or a total of $34 million. Keep in mind that this is in addition to an annual salary and cash bonuses. The logic behind employee options is that they motivate people to work harder and smarter, thus making the company more valuable and benefiting shareholders. But take a closer look at this example. If the risk-free rate is 5.5%, the market risk premium is 6%, and IBM’s beta is 1.19, then the expected return, based on the CAPM, is 5.5% + 1.19(6%) = 12.64%. IBM’s dividend yield is only 0.8%, so the expected annual price appreciation must be about 11.84% (12.64% − 0.8% = 11.84%). Now note that if IBM’s stock price grew from $100 to $134 over 5 years, this would translate to an annual growth rate of only 6%, not the 11.84% shareholders expected. Thus, the executive would receive $34 million for helping run a company that performed below shareholders’ expectations. As this example illustrates, standard stock options do not necessarily link executives’ wealth with that of shareholders.

- Second, and even worse, the events of the early 2000s showed that some executives were willing to illegally falsify financial statements in order to drive up stock prices just prior to exercising their stock options.10 In some notable cases, the subsequent stock price drop and loss of investor confidence have forced firms into bankruptcy. Such behavior is certainly not in shareholders’ best interests.

- As a result, companies today are experimenting with different types of compensation plans that involve different vesting periods and different measures of performance. For example, from a legal standpoint it is more difficult to manipulate EVA (Economic Value Added) than earnings per share. Therefore, many companies incorporate EVA-type measures in their compensation systems. Also, many companies have quit granting options and instead are granting restricted stock that cannot be sold until it has vested.

- Just as “all ships rise in a rising tide,” so too do most stocks rise in a bull market such as that of 2003–2007. In a strong market, even the stocks of companies whose performance ranks in the bottom 10% of their peer group can rise and thus trigger handsome executive bonuses. This situation is leading to compensation plans that are based on relative as opposed to absolute stock price performance. For example, some compensation plans have indexed options whose exercise prices depend on the performance of the market or a subset of competitors.

- Finally, the empirical results from academic studies show that the correlation between executive compensation and corporate performance is mixed. Some studies suggest that the type of compensation plan used affects company performance, while others find little effect, if any. But we can say with certainty that managerial compensation plans will continue to receive lots of attention from researchers, the popular press, and boards of directors.

4. Capital Structure and Internal Control Systems

- Capital structure decisions can affect managerial behavior. As the debt level increases, so does the probability of bankruptcy. This increased threat of bankruptcy affects managerial behavior in two ways. First, as discussed earlier in this chapter, managers may waste money on unnecessary expenditures and perquisites. This behavior is more likely when times are good and firms are flush with cash; it is less likely in the face of high debt levels and possible bankruptcy. Thus, high levels of debt tend to reduce managerial waste. Second, however, high levels of debt may also reduce a manager’s willingness to undertake positive-NPV but risky projects. Most managers have their personal reputation and wealth tied to a single company. If that company has a lot of debt, then a particularly risky project, even if it has a positive NPV, may be just too risky for the manager to tolerate because a bad outcome could lead to bankruptcy and loss of the manager’s job. Stockholders, on the other hand, are diversified and would want the manager to invest in positive-NPV projects even if they are risky. When managers forgo risky but value-adding projects, the resulting underinvestment problem reduces firm value. So increasing debt might increase firm value by reducing wasteful expenditures, but it also might reduce value by inducing underinvestment by managers. Empirical tests have not been able to establish exactly which effect dominates.

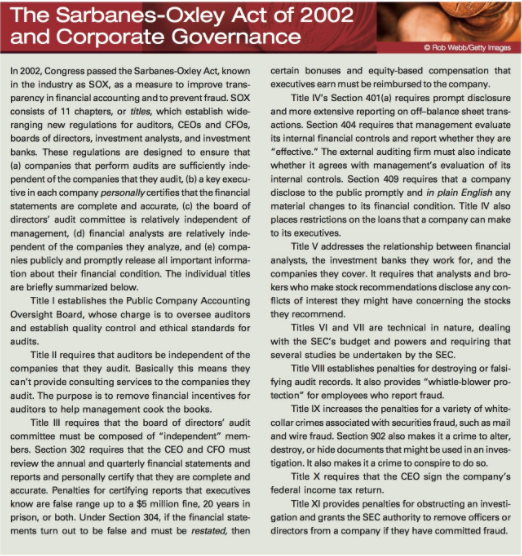

- Internal control systems have become an increasingly important issue since the passage of the Sarbanes-Oxley Act of 2002. Section 404 of the act requires companies to establish effective internal control systems. The Securities and Exchange Commission, which is charged with the implementation of Sarbanes-Oxley, defines an effective internal control system as one that provides “reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.” In other words, investors should be able to trust a company’s reported financial statements.

5. Environmental Factors outside a Firm’s Control

- As noted earlier, corporate governance is also affected by environmental factors that are outside of a firm’s control, including the regulatory/legal environment, block ownership patterns, competition in the product markets, the media, and litigation.

- The regulatory/legal environment includes the agencies that regulate financial markets, such as the SEC. Even though the fines and penalties levied on firms for financial misrepresentation by the SEC are relatively small, the damage to a firm’s reputation can have significant costs, leading to extremely large reductions in the firm’s value.12 Thus, the regulatory system has an enormous impact on corporate governance and firm value.

- The regulatory/legal environment also includes the laws and legal system under which a company operates. These vary greatly from country to country. Studies show that firms located in countries with strong legal protection for investors have stronger corporate governance and that this is reflected in better access to financial markets, a lower cost of equity, increases in market liquidity, and less non-systematic volatility in stock returns.

- Prior to the 1960s, most U.S. stock was owned by a large number of individual investors, each of whom owned a diversified portfolio of stocks. Because each individual owned a small amount of any given company’s stock, there was little that he or she could do to influence its operations. Also, with such a small investment, it was not cost effective for the investor to monitor companies closely. Indeed, dissatisfied stockholders would typically just “vote with their feet” by selling the stock. This situation began to change as institutional investors such as pension funds and mutual funds gained control of larger and larger shares of investment capital—and as they then acquired larger and larger percentages of all outstanding stock. Given their large block holdings, it now makes sense for institutional investors to monitor management, and they have the clout to influence the board. In some cases, they have actually elected their own representatives to the board. For example, when TIAA-CREF, a huge private pension fund, became frustrated with the performance and leadership of Furr’s/Bishop, a cafeteria chain, the fund led a fight that ousted the entire board and then elected a new board consisting only of outsiders.

- In general, activist investors with large blocks in companies have been good for all shareholders. They have searched for firms with poor profitability and then replaced management with new teams that are well versed in value-based management techniques, thereby improving profitability. Not surprisingly, stock prices usually rise on the news that a well-known activist investor has taken a major position in an underperforming company.

- Note that activist investors can improve performance even if they don’t go so far as to take over a firm. More often, they either elect their own representatives to the board or simply point out the firm’s problems to other board members. In such cases, boards often change their attitudes and become less tolerant when they realize that the management team is not following the dictates of value-based management. Moreover, the firm’s top managers recognize what will happen if they don’t whip the company into shape, and they go about doing just that.

- The degree of competition in a firm’s product market has an impact on its corporate governance. For example, companies in industries with lots of competition don’t have the luxury of tolerating poorly performing CEOs. As might be expected, CEO turnover is higher in competitive industries than in those with less competition. When most firms in an industry are similar, you might expect it to be easier to find a qualified replacement from another firm for a poorly performing CEO. This is exactly what the evidence shows: As industry homogeneity increases, so does the incidence of CEO turnover.

- Corporate governance, especially compensation, is a hot topic in the media. The media can have a positive impact by discovering or reporting corporate problems, such as the Enron scandal. Another example is the extensive coverage that was given to option backdating, in which the exercise prices of executive stock options were set after the options officially were granted. Because the exercise prices were set at the lowest stock price during the quarter in which the options were granted, the options were in-the- money and more valuable when their “official” lives began. Several CEOs have already lost their jobs over this practice, and more firings are likely.

- However, the media can also hurt corporate governance by focusing too much attention on a CEO. Such “superstar” CEOs often command excessive compensation packages and spend too much time on activities outside the company, resulting in too much pay for too little performance.

- In addition to penalties and fines from regulatory bodies such as the SEC, civil litigation also occurs when companies are suspected of fraud. Research indicates that such suits lead to improvements in corporate governance.

Last modified: Tuesday, August 14, 2018, 8:53 AM