Reading: Lesson 3 - The Residual Distribution Model

11.3.A - The Residual Distribution Model

1. The Residual Distribution Model

- When deciding how much cash to distribute to stockholders, two points should be kept in mind: (1) The overriding objective is to maximize shareholder value, and (2) the firm’s cash flows really belong to its shareholders, so a company should not retain income unless managers can reinvest that income to produce returns higher than shareholders could themselves earn by investing the cash in investments of equal risk. On the other hand, recall that internal equity (reinvested earnings) is cheaper than external equity (new common stock issues) because it avoids flotation costs and adverse signals. This encourages firms to retain earnings so as to avoid having to issue new stock.

- When establishing a distribution policy, one size does not fit all. Some firms produce a lot of cash but have limited investment opportunities—this is true for firms in profitable but mature industries in which few opportunities for growth exist. Such firms typically distribute a large percentage of their cash to shareholders, thereby attracting investment clienteles that prefer high dividends. Other firms generate little or no excess cash because they have many good investment opportunities. Such firms generally don’t distribute much cash but do enjoy rising earnings and stock prices, thereby attracting investors who prefer capital gains.

- Dividend payouts and dividend yields for large corporations vary considerably. Generally, firms in stable, cash-producing industries such as utilities, financial services, and tobacco pay relatively high dividends, whereas companies in rapidly growing industries such as computer software tend to pay lower dividends.

- For a given firm, the optimal distribution ratio is a function of four factors: (1) investors’ preferences for dividends versus capital gains, (2) the firm’s investment opportunities, (3) its target capital structure, and (4) the availability and cost of external capital. The last three elements are combined in what we call the residual distribution model. Under this model a firm follows these four steps when establishing its target distribution ratio: (1) it determines the optimal capital budget; (2) it determines the amount of equity needed to finance that budget, given its target capital structure (we explain the choice of target capital structures in Chapter 15); (3) it uses reinvested earnings to meet equity requirements to the extent possible; and (4) it pays dividends or repurchases stock only if more earnings are available than are needed to support the optimal capital budget. The word residual implies “leftover,” and the residual policy implies that distributions are paid out of “leftover” earnings.

- If a firm rigidly follows the residual distribution policy, then distributions paid in any given year can be expressed as follows:

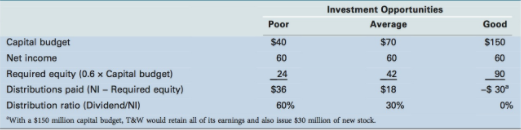

As an illustration, consider the case of Texas and Western (T&W) Transport Company, which has $60 million in net income and a target capital structure of 60% equity and 40% debt.

If T&W forecasts poor investment opportunities, then its estimated capital budget will be only $40 million. To maintain the target capital structure, 40% ($16 million) of this capital must be raised as debt and 60% ($24 million) must be equity. If it followed a strict residual policy, T&W would retain $24 million of its $60 million earnings to help finance new investments and then distribute the remaining $36 million to shareholders:

Under this scenario, the company’s distribution ratio would be $36 million ÷ $60 million = 0.6 = 60%.

In contrast, if the company’s investment opportunities are average, its optimal capital budget would rise to $70 million. Here it would require $42 million of retained earnings, so distributions would be $60 − $42 = $18 million, for a ratio of $18/$60 = 30%. Finally, if investment opportunities are good then the capital budget would be $150 million, which would require 0.6($150) = $90 million of equity. In this case, T&W would retain all of its net income ($60 million) and thus make no distributions. Moreover, because the required equity exceeds the retained earnings, the company would have to issue some new common stock to maintain the target capital structure.

Because investment opportunities and earnings will surely vary from year to year, a strict adherence to the residual distribution policy would result in unstable distributions. One year the firm might make no distributions because it needs the money to finance good investment opportunities, but the next year it might make a large distribution because investment opportunities are poor and so it does not need to retain much. Similarly, fluctuating earnings could also lead to variable distributions, even if investment opportunities were stable. Until now, we have not addressed whether distributions should be in the form of dividends, stock repurchases, or some combination.

2. The Residual Distribution Model in Practice

- If distributions were solely in the form of dividends, then rigidly following the residual policy would lead to fluctuating, unstable dividends. Because investors dislike volatile regular dividends, rs would be high and the stock price low. Therefore, firms should proceed as follows:

1. Estimate earnings and investment opportunities, on average, for the next 5 or so years.

2. Use this forecasted information and the target capital structure to find the average residual model distributions and dollars of dividends during the planning period.

3. Set a target payout ratio based on the average projected data. - Thus, firms should use the residual policy to help set their long-run target distribution ratios, but not as a guide to the distribution in any one year.

- Companies often use financial forecasting models in conjunction with the residual distribution model discussed here to help understand the determinants of an optimal dividend policy. Most large corporations forecast their financial statements over the next 5 to 10 years. Information on projected capital expenditures and working capital requirements is entered into the model, along with sales forecasts, profit margins, depreciation, and the other elements required to forecast cash flows. The target capital structure is also specified, and the model shows the amount of debt and equity that will be required to meet the capital budgeting requirements while maintaining the target capital structure. Then, dividend payments are introduced. Naturally, the higher the payout ratio, the greater the required external equity. Most companies use the model to find a dividend pattern over the forecast period (generally 5 years) that will provide sufficient equity to support the capital budget without forcing them to sell new common stock or move the capital structure ratios outside their optimal range.

- Some companies set a very low “regular” dividend and then supplement it with an “extra” dividend when times are good, such as Microsoft now does. This low-regular- dividend-plus-extras policy ensures that the regular dividend can be maintained “come hell or high water” and that stockholders can count on receiving that dividend under all conditions. Then, when times are good and profits and cash flows are high, the company can either pay a specially designated extra dividend or repurchase shares of stock. Investors recognize that the extras might not be maintained in the future, so they do not interpret them as a signal that the companies’ earnings are going up permanently, nor do they take the elimination of the extra as a negative signal.

Last modified: Tuesday, August 14, 2018, 8:54 AM