Reading: Lesson 2 - Business & Financial Risks

12.2.A - Business Risk and Financial Risk

1. Business Risk and Operating Leverage

- Business risk is the risk a firm’s common stockholders would face if the firm had no debt. In other words, it is the risk inherent in the firm’s operations, which arises from uncertainty about future operating profits and capital requirements. Business risk depends on a number of factors, beginning with variability in product demand and production costs. If a high percentage of a firm’s costs are fixed and hence do not decline when demand falls, then the firm has high operating leverage, which increases its business risk.

- A high degree of operating leverage implies that a relatively small change in sales results in a relatively large change in EBIT, net operating profits after taxes (NOPAT), return on invested capital (ROIC), return on assets (ROA), and return on equity (ROE). Other things held constant, the higher a firm’s fixed costs, the greater its operating leverage. Higher fixed costs are generally associated with (1) highly automated, capital intensive firms; (2) businesses that employ highly skilled workers who must be retained and paid even when sales are low; and (3) firms with high product development costs that must be maintained to complete ongoing R&D projects.

- To illustrate the relative impact of fixed versus variable costs, consider Strasburg Electronics Company, a manufacturer of components used in cell phones. Strasburg is considering several different operating technologies and several different financing alternatives. We will analyze its financing choices in the next section, but for now we will focus on its operating plans.

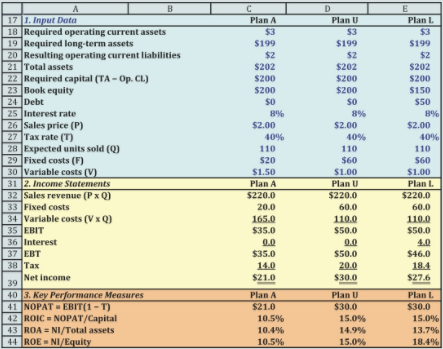

- Strasburg is comparing two plans, each requiring a capital investment of $200 million; assume for now that Strasburg will finance its choice entirely with equity. Each plan is expected to produce 110 million units (Q) per year at a sales price (P) of $2 per unit. As shown in the Figure below Plan A’s technology requires a smaller annual fixed cost (F) than Plan U’s, but Plan A has higher variable costs (V). (We denote the second plan with U because it has no financial leverage, and we denote the third plan with L because it does have financial leverage; Plan L is discussed in the next section.) The Figure below also shows the projected income statements and selected performance measures for the first year. Notice that Plan U’s performance measures are superior to Plan A’s if the expected sales occur.

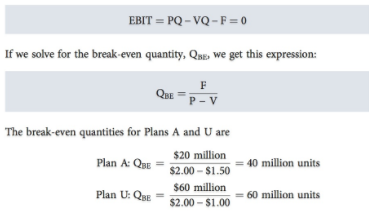

- Notice that the projections in the Figure below are based on the 110 million units expected to be sold. But what if demand is lower than expected? It often is useful to know how far sales can fall before operating profits become negative. The operating break-even point occurs when earnings before interest and taxes (EBIT) equal zero:

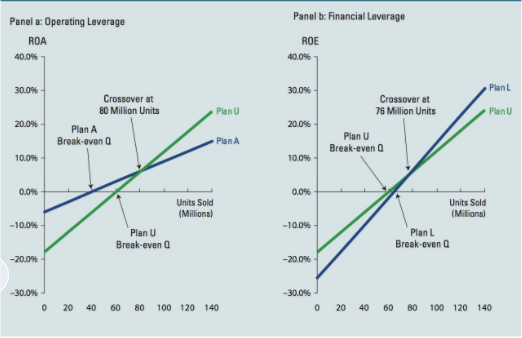

Plan A will be profitable if unit sales are above 40 million, whereas Plan U requires sales of 60 million units before it is profitable. This difference occurs because Plan U has higher fixed costs, so more units must be sold to cover these fixed costs. Panel a of the Figure below illustrates the operating profitability of these two plans for different levels of unit sales. Because these companies have no debt, the return on assets measures operating profitability; we report ROA instead of EBIT to facilitate comparisons.

Suppose sales are at 80 million units. In this case, the ROA is identical for each plan. As unit sales begin to climb above 80 million, both plans increase in profitability, but ROA increases more for Plan U than for Plan A. If sales fall below 80 million, then both plans become less profitable, but ROA decreases more for Plan U than for Plan A. This illustrates that the combination of higher fixed costs and lower variable costs of Plan U magnifies its gain or loss relative to Plan A. In other words, because Plan U has higher operating leverage, it also has greater business risk.

2. Financial Risk and Financial Leverage

- Financial risk is the additional risk placed on the common stockholders as a result of the decision to finance with debt. Conceptually, stockholders face a certain amount of risk that is inherent in a firm’s operations—this is its business risk, which is defined as the uncertainty in projections of future EBIT, NOPAT, and ROIC. If a firm uses debt (financial leverage), then the business risk is concentrated on the common stockholders. To illustrate, suppose ten people decide to form a corporation to manufacture flash memory drives. There is a certain amount of business risk in the operation. If the firm is capitalized only with common equity and if each person buys 10% of the stock, then each investor shares equally in the business risk. However, suppose the firm is capitalized with 50% debt and 50% equity, with five of the investors putting up their money by purchasing debt and the other five putting up their money by purchasing equity. In this case, the five debtholders are paid before the five stockholders, so virtually all of the business risk is borne by the stockholders. Thus, the use of debt, or financial leverage, concentrates business risk on stockholders.

- To illustrate the impact of financial risk, we can extend the Strasburg Electronics example. Strasburg initially decided to use the technology of Plan U, which is unlevered (financed with all equity), but now it’s considering financing the technology with $150 million of equity and $50 million of debt at an 8% interest rate, as shown for Plan L in the Figure above (recall that L denotes leverage). Compare Plans U and L. Notice that the ROIC of 15% is the same for the two plans because the financing choice doesn’t affect operations. Plan L has lower net income ($27.6 million versus $30 million) because it must pay interest, but it has a higher ROE (18.4%) because the net income is shared over a smaller equity base.

- When the quantity sold is 76 million, both plans have an ROIC of 4.8%. The after-tax cost of debt also is 8%(1 – 0.40) = 4.8%, which is no coincidence. As ROIC increases above 4.8%, the ROE increases for each plan, but more for Plan L than for Plan U. However, if ROIC falls below 4.8%, then the ROE falls further for Plan L than for Plan U. Thus, financial leverage magnifies the ROE for good or ill, depending on the ROIC, and so increases the risk of a levered firm relative to an unlevered firm.

- We see, then, that using leverage has both good and bad effects: If expected ROIC is greater than the after-tax cost of debt, then higher leverage increases expected ROE but also increases risk.

Last modified: Tuesday, August 14, 2018, 8:55 AM