Reading: Lesson 7 - Managing the Economy

4.7.A - Managing the Economy

1. PROMOTING ECONOMIC GROWTH

- The strength of a nation depends upon its economic growth. Economic growth is measured by an annual increase in the gross domestic product, a rise in employment opportunities, and the continuous development of new and improved goods and services. However, growth cannot always be at the most desired rate. Unfortunately, when the economy grows too fast or too slow, businesses and consumers suffer. Of concern to everyone is the promotion and measurement of such growth along with the identification and control of growth problems. Economic growth occurs when a country’s output exceeds its population growth. As a result, more goods and services are available for each person. Growth has occurred and must continue if a nation is to remain economically strong.

- The following are basic ways to encourage economic growth:

1. Increase the percentage of people in the workforce.

2. Increase the productivity of the workforce by improving human capital through education and job training.

3. Increase the supply of capital goods, such as more tools and machines, in order to increase production and sales.

4. Improve technology by inventing new and better machines and better methods for producing goods and services.

5. Redesign work processes in factories and offices to improve efficiency.

6. Increase the sale of goods and services to foreign countries.

7. Decrease the purchase of goods and services from foreign countries. - For economic growth to occur, more is required than just increasing the production of goods and services. More goods and services must also be consumed. The incentive for producing goods and services in a free-enterprise economy is profit. If the goods and services produced are in demand and are profitable, business has the incentive to increase production. Economic growth is basic to a healthy economy. Through such growth more and better products become available, such as a new drug that cures disease, a battery that runs a small computer for months, and fuel-efficient cars. More and better services also become available, such as those provided by hospitals, travel agencies, and banks. But more important, economic growth is needed to provide jobs for those who wish to work.

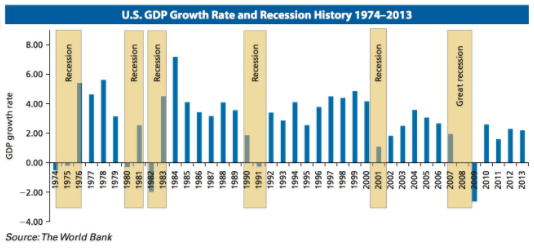

- To know whether the economy is growing at a desirable rate, statistics must be gathered. The federal government collects vast amounts of information and uses a variety of figures to keep track of the economy. The gross domestic product (GDP), as discussed in a previous chapter, is an extremely valuable statistic. The Figure below shows GDP growth rates over a 40-year time period. The consumer price index (CPI) is a measure of the average change in prices of consumer goods and services typically purchased by people living in urban areas. It indicates what is happening in general to prices in the country. To calculate the CPI, the government tracks price changes for hundreds of items, including food, gasoline, housing, and even mobile phones. With the CPI, comparisons can be made in the cost of living from month to month or year to year.

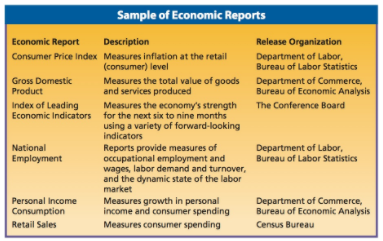

Some commonly used indicators for tracking the economy are shown in the Figure below. Government economists and business leaders examine the CPI, GDP, and other statistics each month to evaluate the condition of the economy. If the growth rate appears to be undesirable, the government can take corrective action.

2. IDENTIFYING ECONOMIC PROBLEMS

- Problems occur with the economy when the growth rate jumps ahead or drops back too quickly. One problem that occurs is a recession, which is a decline in the GDP that continues for six months or more. A recession occurs when demand for the total goods and services available is less than the supply. Sales drop, production of goods and services declines, and unemployment occurs during recessions. In most recessions, the rate of increase in prices is reduced greatly, and in some cases prices may actually decline slightly. The Figure above shows the growth and decline in GDP and recessionary periods since 1974. During this time, there were six recessions, including the Great Recession of 2007–2009.

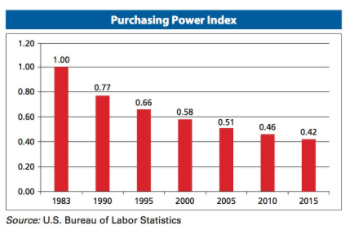

- Another problem arises when consumers want to buy goods and services that are not readily available. As revealed in the consumer price index, this increased demand causes prices for existing goods and services to rise. Inflation is the rise in prices caused by an inadequate supply of goods and services. In other words, demand across a broad variety of goods exceeds supply. Inflation results in a decline in the purchasing power of money; that is, a dollar does not buy as much as it did before inflation. Retired people and those with fixed incomes are financially harmed the most, because their incomes don’t increase fast enough to keep up with rising prices. Therefore, their buying power decreases faster during periods of inflation than does the buying power of workers who receive raises from their employers. The effect of inflation on the purchasing power of the dollar is shown in the Figure below.

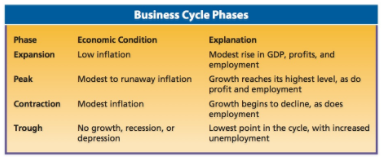

Most industrialized nations experience business cycles, patterns of irregular but repeated expansion and contraction of the GDP. Business cycles, on average, last about five years and pass through four phases, as shown in the Figure below. These four phases—expansion, peak, contraction, and trough—can vary in length and in intensity, with many lasting only a few years. Some, however, can be severe.

When statistics show that the economy may be about to enter a recessionary period (a contraction) or an inflationary period (an expansion), the government can take certain actions. Several specific devices used include controlling taxes, regulating government expenditures, and adjusting interest rates. One way to control economic growth is to raise or lower taxes. Taxes may be raised to slow growth and lowered to encourage growth. When taxes are raised, people and businesses have less money to spend, which discourages economic growth. When taxes are lowered, there is more money to spend, which encourages economic growth.

Government expenditures also influence economic growth. Federal and state governments spend billions of dollars each year to pay salaries and to buy equipment. Government can increase its spending to stimulate a slow economy or reduce spending to slow economic growth. In addition, economic growth is regulated through interest rates, the money paid to borrow money. Borrowing by businesses and consumers generates spending. Spending stimulates economic growth. When interest rates are lowered, businesses are encouraged to borrow. This stimulates business activity and, in turn, the economy. When interest rates are raised to discourage borrowing, a slowdown occurs.

Through interest rates, government spending, taxes, and other government policies, the rate of economic growth can often be controlled. Control, however, is usually kept to a minimum in a free-enterprise system. Furthermore, in a complex economic system the results of such controls are not always clearly visible in the short run. Economists do not always know exactly when control devices should be used, for how long they should be applied, or how effective they may be. Although the nature of controls can be debated, some control is needed to prevent a destructive runaway inflationary period or a depression—a long and severe drop in the GDP. Such conditions affect not only U.S. citizens but also the economic well-being of citizens in foreign countries.

Because most nations engage in international trade and because of the impact of global competition on nations, a major recession or depression in one country usually has negative carryover impacts on other countries. For example, during the Great Recession, the United States experienced a period of recession and slow growth. Other countries in Europe, such as Ireland, Greece, France, and England, also faced similar circumstances.

Last modified: Tuesday, August 14, 2018, 8:16 AM