Reading: Lesson 3 - Business Taxes

6.3.A - Business Taxes

1. GENERAL NATURE OF TAXES

- Although government uses many different ways to regulate business, no way is more important than taxes. The types and amounts of taxes influence business decisions that, in turn, can influence the total amount of business activity in a region and in the nation. Both businesses and individuals pay many kinds of taxes to local, state, and federal governments. Taxes collected by the federal government account for about 53 percent of all taxes collected, while various state and local taxes account for the remaining 47 percent. Government levies taxes for different reasons. When government decides to levy a particular type of tax, it must consider fairness to taxpayers.

- Governments levy taxes mainly to raise revenue (money) to fund new and ongoing programs. Governments also use taxes to regulate business activity. Governments set revenue goals that must be reached in order to provide the various services desired by the public. Examples of these services range from law enforcement and road building to providing for the military defense of the country. It is costly for governments to provide the many services the public wants. To pay for these services, governments must collect taxes. Governments also use taxes to control business activity. They can speed up economic growth by lowering taxes and slow it by raising taxes. The federal government also taxes certain foreign goods that enter this country in order to encourage consumers to purchase American-made rather than foreign-made products. State and local governments also control business activity through taxation. For example, they often set high taxes on alcoholic beverages and tobacco, in part to discourage customers from purchasing these products.

- It is difficult for government to find ways to levy taxes fairly and still raise sufficient amounts of money to meet government expenses. The question of fairness has caused many debates. One problem is determining who will, in fact, pay the tax. For example, a firm may have to pay taxes on the goods it manufactures. But, because the tax is part of the cost of producing the product, this cost may be passed on to the customer. Another problem of fairness is whether those with the most assets or most income should pay at a higher rate than those who own or earn the least. Government tries to solve the fairness problem by adopting a proportional, progressive, or regressive tax policy.

- A proportional tax—sometimes called a flat tax—is one in which the tax rate remains the same regardless of the amount on which the tax is imposed. For example, in a given area the tax rate on real estate per $1,000 of property value is always the same, regardless of the amount of real estate the taxpayer owns. The total dollar amount of the tax paid by someone with a $400,000 home will differ from that paid by the person with a $175,000 home in the same area, but the rate of the tax is the same for both owners. A flat state tax of 6 percent on income is also proportional. Those with higher incomes pay more dollars than those with lower incomes, but the tax rate of 6 percent stays the same.

- A progressive tax is a tax based on the ability to pay. The policy of progressive taxation is a part of many state and federal income tax systems. As income increases, the tax rate increases. As a result, a lower-income person is taxed at a lower rate than a higher-income person is. In fact, the Tax Foundation found that in a recent year, 5 percent of the taxpayers who pay the most taxes contributed over 58 percent of all the federal individual income taxes collected. Some local and state governments have combined the policies of proportional and progressive taxes. For example, a state may apply a flat tax of 5 percent to incomes up to $20,000 and 6 percent to all incomes over $20,000.

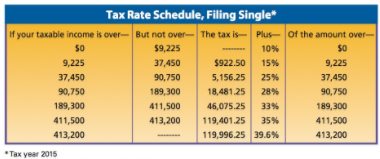

- The current federal tax law is a combination of progressive and proportional taxation policy. The Figure below illustrates the 2015 tax rate schedule used to calculate income tax for single taxpayers. Regardless of total income, everyone pays the same rate on taxable income up to $9,225 of income— 10 percent. The tax then progresses through the next five brackets. For example, if your taxable income were exactly $9,225, your tax would be $922.50. If your cousin had taxable income of $10,000, her tax would be $1,038.75. Just like you, your cousin pays $922.50 on the first $9,225 of taxable income, plus an additional 116.25. The additional amount is 15 percent on the amount over 9,225 (0.15 × $775). Most people consider the tax fair because people with higher incomes pay at a higher rate than those with lower incomes.

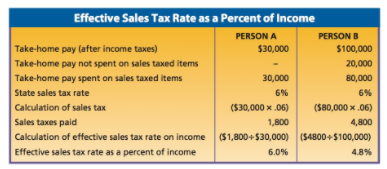

The third type of tax policy is a regressive tax. With this type of tax, the actual tax rate decreases as the taxable amount increases. Although general sales taxes are often thought to be proportional, they are actually regressive, because people with lower incomes pay a larger proportion of their incomes in taxes than those with higher incomes. Suppose, for example, that Person A and Person B live in a state with a 6 percent general sales tax. As shown in the Figure below, Person A, with an annual take-home pay of $30,000, pays a 6 percent tax rate. Person B, who has an annual take-home pay of $100,000 and may have put $20,000 in savings (which incurs no sales tax), pays only a 4.8 percent tax rate. Because the sales tax applies to purchases rather than to income, the general sales tax is regressive. For a less regressive sales tax, some states exclude taxes on such purchases as food and clothing. These exclusions are usually items on which low-income families spend a high percentage of their income.

2. TYPES OF TAXES

- Taxation has become so complicated that the average businessperson spends a great deal of time filling out tax forms, computing taxes, and filing reports. In many businesses, various taxes reduce income by a large percentage. The three most common taxes affecting businesses and individuals are income taxes, sales taxes, and property taxes.

- The federal government and most state governments use the income tax to raise revenues. An income tax is a tax on the profits of businesses and the earnings of individuals. For individuals, the tax is based on salaries and other income earned after certain deductions. For businesses, an income tax usually applies to net profits (receipts less expenses).

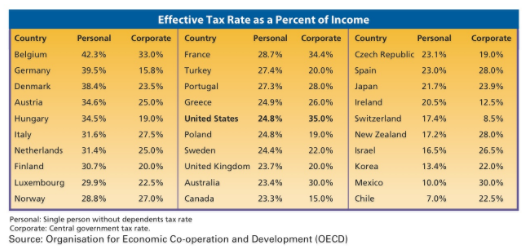

- The income tax is the largest source of revenue for the federal government. Individuals pay about 83 percent of the total federal income taxes collected, and businesses pay nearly all of the remaining 17 percent. Businesses share the cost of collecting individual income taxes. Every business is required to withhold income taxes from employees’ earnings and turn them over to the government. Thus, business performs an important tax service for government. As shown in the Figure below, tax rates paid by individuals in the United States fall somewhere in the middle when compared to tax rates paid by individuals in other developed nations. U.S. corporate tax rates are the highest among developed nations. However, with tax credits and exemptions and offshore tax havens, the actual tax burden of U.S. companies has been estimated to be 12.6 percent.

Federal Insurance Contributions Act (FICA) taxes include Social Security and Medicare. Employees and employers share the burden of these taxes, and employers withhold the employee portion from wages. For 2015, both employees and employers paid Social Security tax of 6.2 percent and Medicare tax of 1.45 percent. For 2015, only the first $118,500 in income was subject to the Social Security tax. There is no wage base limit for the Medicare tax. Self-employed workers pay FICA tax at a higher rate than employed workers because they pay both the employer and employee portions. The self-employment tax rate for 2015 was 15.3 percent (12.4 percent for Social Security and 2.9 percent for Medicare.)

A sales tax is a tax levied on the retail price of goods and services at the time they are sold. A general sales tax usually applies to all goods or services sold by retailers. However, when a sales tax applies only to selected goods or services, such as cigarettes and gasoline, it is called an excise tax. Sales taxes are the main source of revenue for most states and some cities and counties. State governments do not all administer sales taxes in the same way. In most cases the retail business collects the tax from customers and turns this tax over to the state government. A business must be familiar with the sales tax law of the state in which it operates so that it can collect and report the tax properly. From time to time, federal officials have considered charging a national sales tax. State officials, however, strongly oppose a national sales tax because the state tax is their primary source of revenue. The question as to how and whether to tax Internet sales is also under debate between the states and the federal government. Both see this source of taxes as highly attractive. Traditional retailers who pay sales taxes believe it is unfair for Internet sales not to be taxed.

A property tax is a tax on material goods owned. Whereas the sales tax is the primary source of revenue for most state governments, the property tax is the main source of revenue for most local governments. There may be a real property tax and a personal property tax. A real property tax is a tax on real estate, which is land and buildings. A personal property tax is a tax on possessions that are movable, such as furniture, machinery, and equipment. Essentially, personal property is anything that is not real estate. In some states, there is a special property tax on raw materials used to make goods and on finished goods available for sale. A tax on property—whether it is real property or personal property—is stated in terms of dollars per hundred of assessed valuation. Assessed valuation is the value of property determined by tax officials. Thus, a tax rate of $2.80 per $100 on property with an assessed valuation of $180,000 is $5,040 ($180,000/100 = $1,800; $1,800 × $2.80 = $5,040).

Managers consider taxes in many of their major decisions. Taxes may influence the accounting method a business selects to calculate profits and the method used to pay managers. Often, taxes are used as a basis for deciding where to locate a new business or whether to move a business from one location to another. For example, assume that a producer of garden tools is trying to decide in which of two cities to build a new factory. City A is located in a state that has a low state income tax and low property taxes. City B is located in a state with no state income tax but high property taxes. After weighing all the factors, the producer decides to locate in City A. City A, which has both an income tax and a property tax, is selected mainly because the total tax cost each year is less than in City B.

Last modified: Tuesday, August 14, 2018, 8:19 AM