Reading: Lesson 2 - Budgets and Budgeting

8.2.A - Budgets and Budgeting

1. BUSINESS BUDGETS

- Budgeting is critical to financial success. Studies of differences between successful and unsuccessful new businesses consistently find that those that carefully develop and follow budgets increase their chances of survival and success. The financial practices of successful businesses are (1) maintaining a complete and up-to-date set of financial records, (2) having detailed financial records reviewed regularly by objective professionals, (3) keeping accurate records of business inventory and (4) using financial budgets as planning and management tools.

- A new company’s business plan should include financial budgets for the first year of operations and more general financial projections for two or more additional years. Unfortunately, many small businesses do not update the initial budget even if one was developed as part of the business plan. A large number of business owners and managers report they don’t have confidence in their ability to plan and use financial budgets. A budget is a written financial plan for business operations developed for a specific period of time. Budgets are often developed for six months or a year but can cover a longer or shorter time period depending on the type of budget and the nature of the business. Budgets project and offer detail on the business’s estimated revenue and expenses over the time period. Based on these estimates, businesses can set financial goals. They then use the budget to develop operating plans for that time period. By comparing actual results with financial goals and budget details throughout the year, managers can control operations and keep expenses in line with income. A realistic budget can prevent overspending and be used to plan for needed income, including the possibility of borrowed funds.

- Actual budgeting procedures depend on the type of business. For a new small business, the process is mostly one of budgeting start-up costs, sales, expenses, purchases, and cash. Large businesses have a number of specialized budgets that predict the financial performance of operating areas of the company such as research and development, information technology, human resources, production, marketing, distribution and logistics, and many others. In large businesses, the final overall budget for a business is made up of several specific budgets, such as the sales, merchandising, advertising, cash, capital, and operating budgets. Most specialized budgets are based on sales and income projections. However, in some types of businesses, either the production capacity or the financial capacity of the business or the unit for which the budget is being prepared must be determined first. Sales and all other estimates are then based on the amount that can be produced or the available financial resources for the time period.

- The start-up budget projects income and expenses from the beginning of a new business until it is expected to become profitable. It identifies the start-up costs, initial operating expenses, types and sources of financing, and projected income for the time period of the budget. A start-up budget is usually prepared in large and established businesses whenever a new venture is being planned, such as the introduction of a new product, expansion into a new market, or the development of a new type of business operation. Business start- ups usually require large expenditures for equipment, inventory, salaries, and operating expenses. Income will not be realized for some time while expenses grow. Even when the new company begins to sell products and services, the income will not be adequate to cover the initial expenses.

- An operating budget is a plan showing projected sales, costs, expenses, and profits for the ongoing operations of a business. It projects operating income and expenses for the entire business or for a specific part of the business for an identified time period, such as three months, six months, or a year. The operating budget is a particularly useful planning tool because it uses the same financial categories as the company’s income statement. By subtracting its total projected costs and expenses from projected income, a business can estimate the profitability of its operations. The projections can then be compared to the actual results achieved when an income statement is prepared at the end of the time period covered by the operating budget.

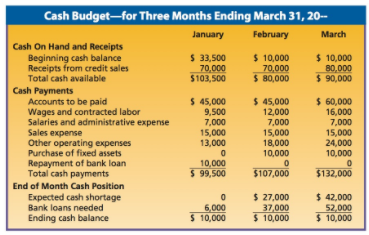

- During normal operations, companies receive cash from sales and from borrowing and use cash for purchases and loan payments. The cash budget is an estimate of the flow of cash into and out of the business over a specified time period. Companies need a cash budget to make certain that enough cash will be available at the right times to meet payments as they come due. Cash comes into the company from two primary sources: (1) cash receipts and (2) borrowing. When companies borrow money, they must eventually pay it back. Therefore, the cash budget shows borrowed money as cash flowing in and repayments as cash flowing out when each payment is due. The Figure below shows a cash budget for a small business. Cash budgets are important for all companies, no matter how large or successful they are. A company can be highly profitable yet not have enough cash on hand at the right times to pay its bills. This situation could cause the company to borrow unnecessarily. A cash budget can help a company avoid this. Cash budgets are also used to prevent the company from holding too much cash when it is not needed. That can result in missing out on profitable uses of the cash during the period when it is not needed.

- Every business must plan for the costs of buildings, equipment, and other expensive purchases needed for its operations. Over the years, it must also budget to replace wornout or obsolete fixed assets. For instance, if a company owns its own trucks and vans for distributing products, each will need to be replaced after a certain number of miles or years. A growing business plans for expansion by budgeting for the costs of new equipment, additions to buildings, and other major investments. A capital budget is a financial plan for replacing fixed assets or acquiring new ones. Capital budgeting is important because acquiring assets ties up large sums of money for long periods of time. A wrong decision can be costly. For example, a decision to buy three new trucks that have a projected life of eight years involves a large expenditure. The manager must plan well in advance if the money is to be available when the trucks are needed. Assume that the company buys the trucks based on a forecast that future sales will justify their need. However, if sales do not increase as expected, profits will be lower as a result of the added costs related to the purchase.

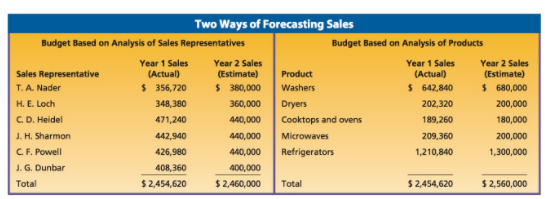

- The sales budget is a forecast of the sales revenue a company expects to receive in a month, a quarter, or a year. Estimated sales are usually projected for sales territories, types of customers (government, industrial, consumer), sales representatives, geographic areas, or product categories. Each of the sales managers responsible for the various categories (territories, customers, products) makes estimates for the sales and expenses of his or her unit. The top sales manager uses those estimates to prepare a final sales budget. Sometimes managers prepare sales estimates with the idea of developing quotas or goals for sales representatives and territories. These estimates provide a goal for the sales department as well as a source of information for preparing related budgets such as production, advertising, or cash and operating budgets.

- The Figure below shows sales estimates determined in two different ways for the same company. Because the two sets of estimated figures are not the same, someone must combine them into one satisfactory estimate for the sales department. Numerous factors influence sales estimates. The specific operating and management factors of each company play an important part. Although one company may enjoy a high sales volume, another—at the same time and under the same conditions—may suffer a decline in sales. Economic conditions are often important in planning sales. If a good harvest and favorable prices for crops are anticipated in a certain area, a company that sells farm machinery should have good sales prospects in that area. A retail store in that same area might not anticipate the same increase in sales if agricultural customers make up a small percentage of their business. A major competitor entering a market for the first time may have a significant effect on established but smaller businesses. These are examples of some of the influences that should guide a manager in making sales estimates.

2. ADMINISTERING THE BUDGET

- Because a budget is an estimate of what might happen, it usually cannot be followed exactly. Staying close to the amount budgeted is desirable. However, for various reasons often beyond the control of managers, actual income and expenses may vary from the budgeted amounts. For that reason, managers often prepare three budget estimates. The first estimate assumes that sales will be less than expected. The second estimate considers what most likely will occur. And the third estimate assumes sales will be better than expected. The second estimate is followed unless anticipated conditions change. If sales are less than expected, the business can shift immediately to the first (lower) set of budget figures. Should sales be better than expected, the business can shift to the third (higher) set of budget figures. Having more than one budget estimate allows for realistic flexibility during budget planning. It also forces managers to consider what might happen under favorable and unfavorable conditions and to be better prepared for rapid changes.

- Whether a business is large or small or uses one or more budgets, managers must use the budget to monitor ongoing operations and control expenses. That monitoring activity determines whether the business is on, under, or over budget. If expenditures exceed budgeted amounts, managers want to quickly understand why so they can make necessary changes. Some adjustments may be easy, whereas others may not even be possible. For example, labor costs might exceed budget estimates for the planned level of production because a number of new employees have been added who are not as productive as experienced employees. Additional training for those employees might help improve productivity, reducing the labor costs required to meet production goals during the rest of the budget period. However, if labor costs are higher than the budget because of an unanticipated increase in the wage rate needed to hire the new employees, little can be done to lower those costs in the short run.

- If a comparison of actual operating performance with the budget estimates reveals that the business will not make the expected profit or will have a loss, the manager must review all expenses to determine what can be done to reduce them. Some expenses may be easier to reduce in the short run than others. However, cutting some expenses may lead to longer-term profitability problems. For example, if a manager tries to reduce costs in the short run by not purchasing new inventory, those costs will need to be increased in the future to replace the inventory or sales will be lost. Cutting the number of employees to save on labor costs may put too much pressure on the remaining employees. Their productivity may go down or some may quit, leading to increased costs to replace them.

- The use of budgets and a budgeting system cannot guarantee the success of a business, but these management tools can help reduce losses or increase profits. The entire budgeting process is valuable in planning and controlling activities for managers. But whether a business is a success can be determined only after the budget time periods have passed. Comparing budgets with actual operating conditions provides a basis for making timely and knowledgeable management decisions, which, in turn, leads to more accurate budgets and more profitable operations in the future.

Last modified: Thursday, March 14, 2024, 1:19 PM