Reading: Lesson 4 - Analyzing Financial Data

8.4.A - Analyzing Financial Data

1. USING FINANCIAL INFORMATION

- Managers use financial statements as well as other financial information to understand the financial health of a business. Others are also concerned about the business’s financial health. That includes current and prospective investors; creditors, including banks and suppliers who may make loans and offer credit to the business; government officials involved in taxation and oversight of business practices; and customers. They want to know such things as whether the cash flow and working capital are sufficient to pay the company’s bills. They also analyze ratios calculated from financial statements to identify where any financial problems lie. Financial statements must be prepared in a way that provides a clear and understandable picture of the financial health of an organization. The people who are affected by the financial condition of the business need to have access to the financial information and be able to analyze the information to draw conclusions about the business’s financial health.

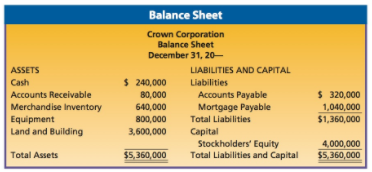

- Working capital is the difference between current assets and current liabilities. The word current refers to assets and liabilities that are expected to be exchanged for cash within one year or less, such as accounts receivable and payable. For example, companies expect most customers to pay for their credit purchases within a year. Therefore, accounts receivable are current assets. Similarly, companies expect to pay for their credit purchases within a year, so accounts payable are current liabilities. When current assets are much larger than current liabilities, businesses are better able to pay current liabilities. The amount of working capital is one indicator that a business can pay its short-term debts. Businesses with large amounts of working capital usually find it easier to borrow money, because lenders feel assured that these businesses will have the means to repay their loans. Notice that the numbers used in the analysis are the current assets and current liabilities drawn from the company’s balance sheet shown in the Figure below.

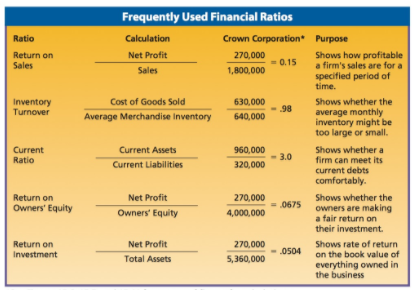

Managers use ratios to examine different areas of the business for possible financial problems. The Figure below describes some important ratios and their uses. The data for these ratios come from Crown Corporation’s financial statements: balance sheet, income statement, and working capital. Financial ratios for current financial statements can be compared with the same ratios from prior periods, with ratios from other firms, and with other types of ratios. Organizations such as Dun & Bradstreet publish a standard list of average ratios for various types of businesses. Companies can use those published ratios to compare with their own ratios to get a sense of how they are doing in relation to other companies in their industry. Lenders use ratios to decide whether a company is a good loan risk. Managers use ratios to identify possible problems needing corrective action. For example, if the company’s return on investment is below average for its industry, then managers know that they may have to increase profits to attract new investors. If the company’s current ratio keeps decreasing each period, then its liabilities are growing faster than its assets. This indicates that the company may be getting into debt trouble.

2. MAKING DECISIONS FROM NUMBERS

- Managers, whether or not they are accountants, must make decisions based on the business’s financial statements. Managers are responsible for the profitability and sustainability of the business. They need to ensure that there is enough cash available for the business to purchase inventory, cover expenses, and make payroll. Stockholders expect a business to be efficient and perform well comparatively to competitive operations. All of this requires managers to understand and use numbers.

- There are two types of comparative analysis a manager should use: one is to track performance over time and the other is to compare performance against peer organizations. A historical analysis allows a business to track its performance over time to evaluate trends and make comparisons to previous time periods. With accounting records that are created by automated record keeping and computers, this analysis can be tracked monthly, or even weekly. For many retail businesses that rely on Christmas sales, such as jewelry stores, historical sales figures as early as October could give indications of Christmas sales potential and inventory needs. Businesses of all sizes operate within an industry. For example, the Crown Corporation discussed earlier is a jewelry business. Crown should use industry comparative financial reports to evaluate its financial performance. The Jewelers of America, a jewelry industry trade group, prepares a Cost of Doing Business Report. This report provides information in terms of dollars and percentages for income and expense statements, balance sheets, and cash flow analysis. The report also provides ratios for working capital, profitability and return on investment, asset turnover and efficiency, debt service coverage, and capital structure. This information is available for high-end, mid-range, chain, and designer businesses. It is further broken down by annual sales ranges and levels of profitability for typical firms and the top 25 percent performers. This information can act as a benchmark for Crown.

- Larger businesses may have a rating from a credit rating agency such as Fitch Ratings, Moody’s Investors Service, or Standard & Poor’s. These agencies analyze the financial statements of companies and rate them from AAA (triple A) to D. The ratings have a direct impact on investors’ willingness to invest in firms as well as on a firm’s financing costs. For example, a AAA firm may be viewed by investors as a strong company with a good future profit potential. This company may be able to borrow at a lower interest rate. A C-rated firm may find that investors are unwilling to invest and banks are unwilling to make loans to the company.

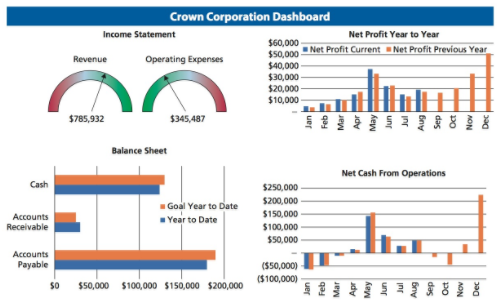

- Managers may use dashboards to track the financial performance of their business and business units. Like an automobile dashboard, a financial dashboard is a graphic designed to provide a quick view of key financial performance indicators. Financial dashboards use graphics to visually summarize a wide variety of results on a single computer screen. They can show historical data or even live data when linked to a fully integrated accounting system. Many companies produce financial dashboards that are customized to meet a manager’s information needs. Month-to-month or year-to-year data can be presented. Benchmarks can be indicated and trends can be projected. The Figure below shows a dashboard for Crown Corporation. Crown’s management has determined its goals, and they are displayed in a series of graphics and charts.

3. SOURCES OF FINANCIAL INFORMATION

- In some situations, businesses may need general advice or special help with a financial problem. Accountants, bankers, and financial consultants can provide expertise beyond what the company’s employees and managers can provide. Businesses can also consult specialists from state and federal government agencies.

- Accountants understand the complex systems used to collect, sort, and summarize financial data. They can analyze and explain the meaning and importance of the details found on financial statements. Accountants also help managers interpret financial data and make suggestions for handling various financial aspects of a business. Large firms have full-time accountants, whereas small firms usually hire accountants on a part-time basis. A firm may hire a certified public accountant, or CPA, a person who has met a state’s education, experience, and examination requirements in accounting. Corporations that sell stock to the public must hire CPAs to audit their financial records annually. An audit is an examination of a company’s financial records by an expert to verify their accuracy.

- Bankers also assist businesses with financial decisions. Bankers are well informed about the financial condition of businesses, and they also provide advice on how and where to get loans. Because bankers frequently work with businesses, they are aware of businesses’ problems and needs. In the opening story, Clark knew he would need to ask his banker for help and advice to obtain the loan he needed for his business.

- A consultant is someone who gives professional advice or offers professional services. Businesses hire consultants with specific expertise to help managers solve problems or to provide services that are not available within the business. Consultants are not employees; they are outside experts with specialized knowledge. A financial consultant is valuable to people thinking about starting a business and to managers facing financial challenges in existing businesses. Professors of accounting, finance, and management from colleges or universities often serve as consultants. Many large and small consulting firms offer their services to businesses for a fee. Consulting firms employ a variety of experts who have both education and experience in business operations and management. Some specialize in a particular area such as financial services; others offer expertise in a broad set of business issues.

- Many state and federal government agencies provide financial information and other resources for businesses. Probably the best known, the Small Business Administration (SBA) is an agency of the federal government that provides information, advice, and assistance in obtaining credit and other financial support for small businesses. Regional offices in every state offer expertise and access to a range of technical and managerial information for small business owners and people who are considering starting a new business. Other federal agencies offering resources and assistance as well as regulations related to the financial performance of businesses are the Department of Commerce and the Department of the Treasury.

Last modified: Tuesday, August 14, 2018, 8:29 AM