Reading: Internal Rate of Return & Payback Period Analysis

Internal

Rate of Return (IRR)

•Internal

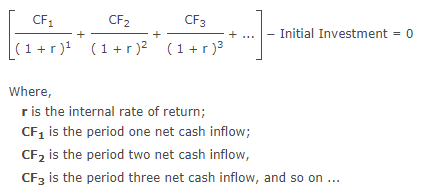

rate of return (IRR) is the discount rate at which the net present value of an

investment becomes zero. In other words, IRR is the discount rate which equates

the present value of the future cash flows of an investment with the initial

investment. It is one of the several measures used for investment appraisal.

•

•Decision

Rule

- A project should only be accepted if its IRR is NOT less than the target internal rate of return. When comparing two or more mutually exclusive projects, the project having highest value of IRR should be accepted.

- A project should only be accepted if its IRR is NOT less than the target internal rate of return. When comparing two or more mutually exclusive projects, the project having highest value of IRR should be accepted.

IRR

Calculation

•The

calculation of IRR is a bit complex than other capital budgeting techniques. We

know that at IRR, Net Present Value (NPV) is zero, thus:

-NPV = 0; or

- PV of future cash flows − Initial Investment = 0; or

-NPV = 0; or

- PV of future cash flows − Initial Investment = 0; or

IRR

Problem

•But

the problem is, we cannot isolate the variable r (=internal rate of return) on

one side of the above equation. However, there are alternative procedures which

can be followed to find IRR. The simplest of them is described below:

•

1.Guess the value of r and calculate the

NPV of the project at that value.

2.If NPV is close to zero then IRR is equal

to r.

3.If NPV is greater than 0 then increase r

and jump to step 5.

4.If NPV is smaller than 0 then decrease r

and jump to step 5.

5.Recalculate NPV using the new value of r

and go back to step 2.

IRR

Example

Find the IRR of an investment having initial cash outflow of $213,000. The cash inflows during the first, second, third and fourth years are expected to be $65,200, $96,000, $73,100 and $55,400 respectively.

Solution

Assume that r is 10%.

NPV at 10% discount rate = $18,372

Since NPV is greater than zero we have to increase discount rate, thus

NPV at 13% discount rate = $4,521

But it is still greater than zero we have to further increase the discount rate, thus

NPV at 14% discount rate = $204

NPV at 15% discount rate = ($3,975)

Since NPV is fairly close to zero at 14% value of r, therefore

IRR ≈ 14%

Payback

Period

•Payback

period is the time in which the initial cash outflow of an investment is

expected to be recovered from the cash inflows generated by the investment. It

is one of the simplest investment appraisal techniques.

•Decision

Rule

- Accept the project only if its payback period is LESS than the target payback period.

- Accept the project only if its payback period is LESS than the target payback period.

Payback

Period Formula

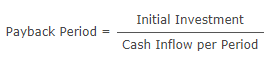

The

formula to calculate payback period of a project depends on whether the cash

flow per period from the project is even or uneven. In case they are even, the

formula to calculate payback period is:

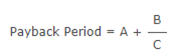

When

cash inflows are uneven, we need to calculate the cumulative net cash flow for

each period and then use the following formula for payback period:

Payback

Period Example

Example 1: Even Cash Flows

Company C is planning to undertake a project requiring initial investment of $105 million. The project is expected to generate $25 million per year for 7 years. Calculate the payback period of the project.

Solution

Payback

Period = Initial Investment ÷ Annual Cash Flow = $105M ÷ $25M = 4.2 years

Payback

Period Example

Example 2: Uneven Cash Flows

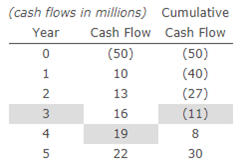

Company C is planning to undertake another project requiring initial investment of $50 million and is expected to generate $10 million in Year 1, $13 million in Year 2, $16 million in year 3, $19 million in Year 4 and $22 million in Year 5. Calculate the payback value of the project.

Payback Period

= 3 +

(|-$11M| ÷ $19M)

= 3 +

($11M ÷ $19M)

≈ 3 +

0.58

≈

3.58 years

Last modified: Tuesday, August 14, 2018, 8:51 AM